Becoming an optometrist or dentist might make mom proud, but engineers, nurses and computer scientists are typically in a better position to tackle graduate school student loan debt after they enter the workforce — even though they tend to earn much less.

That’s according to an analysis of over 91,000 borrowers requesting rates to refinance student loans from graduate school through the Credible.com consumer finance marketplace.

“We need more transparency to help students get a handle on what they will earn after graduation, and how much debt those earnings will support.”

Stephen Dash, Founder & CEO of Credible

Credible’s analysis of federal and private student loan debt levels and salaries across 16 graduate school majors shows that the most important consideration isn’t how much debt you’ll take on to obtain an advanced degree — or how much you’ll earn after graduation — but achieving the right balance between the two.

“When choosing graduate school programs, it’s easy for students to get distracted by potential high salaries, regardless of the student loan debt incurred,” explains Stephen Dash, founder and CEO of Credible. “Our analysis shows that students who balance student loan debt against their future earnings are often in a better financial position to pay back their loans.”

What’s a graduate degree worth? Depends on the degree

Even though doctors and lawyers often take on dizzying levels of student loan debt, they’re usually able to maintain a relatively healthy balance between debt and income that enables them to stay on top of their loans.

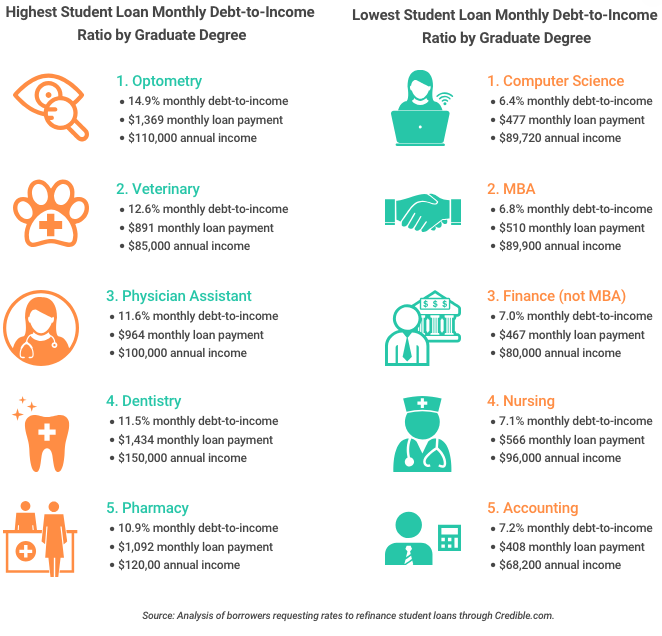

By the time they come to Credible to investigate their student loan refinancing options, optometrists, veterinarians, physician assistants, dentists and pharmacists are still allocating more than 10 percent of their monthly income to their student loan payments. Optometrists allocate the most toward their student loans, with 14.9 percent of their monthly income going toward their student debt.

While computer scientists may earn significantly less than optometrists, they also take on significantly less student loan debt. That means computer scientists can earmark just 6.4 percent of their monthly income to repaying their student debt after leaving school.

The five most debt-heavy graduate degrees

Based on the percentage of their monthly income allocated to their student loan payments, we identified the five most debt-heavy graduate degrees, as well as the degrees that are the most worry-free:

The 1:1 debt to annual earnings rule of thumb (and why you should be nicer to your eye doctor, vet and dentist)

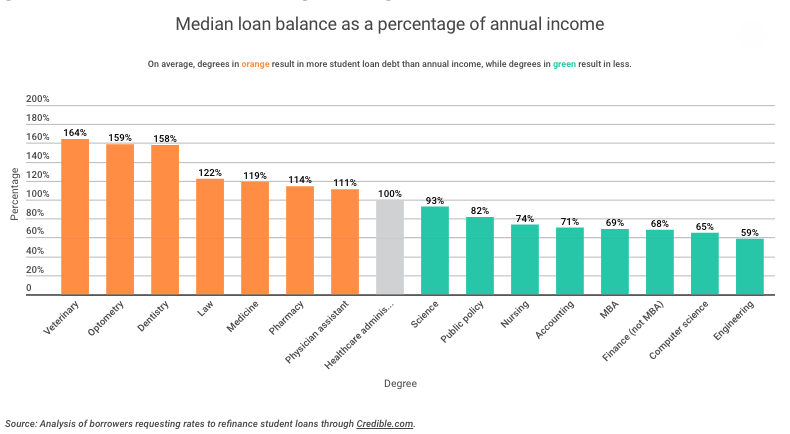

Financial aid advisors often say a good rule of thumb is not to take on more student loan debt than your expected annual earnings.

Credible’s analysis found that engineers, accountants, and nurses can generally breathe easy in this regard, as can holders of advanced degrees in finance, and public policy.

Many scientists, healthcare administrators, and physician assistants have achieved parity, or near parity, between income and student loan debt by the time they pursue refinancing.

Doctors, lawyers, and pharmacists are approaching a balance between debt to income, but dentists, optometrists, and veterinarians tend to have student loan debt that’s far out of whack with their earnings.

“While incomes tend to rise over time, students considering going into professions where they are likely to have higher debt-to-income ratios should think carefully about how they plan on paying down their student loans upon graduation,” said Dash. “Dentists, in particular, are in a particularly challenging position of having to go through rigorous and costly training — taking on significantly more debt than medical doctors for their schooling — only to earn an average of about 10 percent less than doctors after graduation.”

Students need more and better information

If students and their families had better information about college costs and outcomes — including earnings by major — that could also help them make smarter decisions about which school and which degree is right for them.

“Students considering going into professions with higher debt-to-income ratios should think long and hard about how they plan on paying down their student loans upon graduation.”

Stephen Dash

Thanks to services like College Scorecard and College Abacus, students can research the cost of earning a degree at thousands of schools. They can also get some limited information about how much graduates of those schools earn. But because Congress has barred the Department of Education from tracking the earnings of individual students into the workforce, it’s hard for students to find earnings data for both school and major.

A bipartisan bill, The College Transparency Act, would simplify the process of collecting the information needed to follow graduates into the workforce and track their earnings by school and major. The bill aims to address privacy concerns voiced by groups like the American Civil Liberties Union.

“There’s been progress in providing access to information about what college will actually cost,” Dash said. “But we need more transparency to help students get a handle on what they will earn after graduation, and how much debt those earnings will support.”

The double-edged sword of stretching payments out

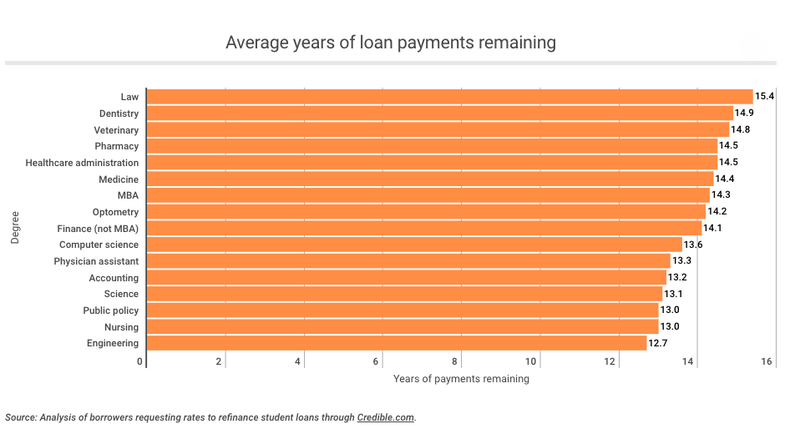

The standard repayment term for a government student loan is 10 years. But borrowers who take on more student loan debt than they can handle often enroll in income-driven repayment plans that can stretch their payments out over as long as 20 or 25 years.

While stretching payments out over a longer period of time can make monthly payments more manageable, it can also result in borrowers making thousands of dollars in additional interest payments. Credible’s analysis shows that lawyers, dentists, veterinarians and pharmacists are taking the longest to pay back their loans, while engineers, nurses and public policy majors are paying down their loans the fastest.

An advanced degree in nursing can entail taking on a sizeable amount of student loan debt — the median loan balance among nurses investigating refinancing was $71,422.

But with a median income of $96,000, Credible’s analysis found nurses were taking home bigger paychecks than scientists ($62,858), accountants ($68,200), and holders of advanced degrees in public policy ($70,000 ), health care administration ($70,000) and finance (non-MBA, $80,000).

It should be noted that nurses with advanced degrees sought out refinancing at a later stage in their career than other borrowers. The median age of nurses checking rates through the Credible marketplace was 37, compared to 32 for the group as a whole.

“Market demand for certain skill sets can definitely play a role in salaries paid in specific fields, and students will be well served by not only looking at what careers are paying well today, but what skills and expertise we’ll likely need more of in the future,” said Dash.

Methodology

Data for this analysis came from the more than 91,000 graduate degree holders who came to Credible.com between January 2015 and March 15, 2018 to request interest rates for potentially refinancing their student loan debt. This article was published on April 10, 2018.

This article originally appeared on Credible.com and was syndicated by MediaFeed.org.

Featured Image Credit: DepositPhotos.com.

AlertMe