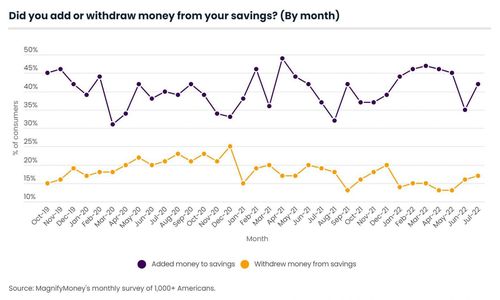

Many Americans are increasingly fearful that the economy is approaching a recession. For many, that means it’s time to start saving again. The latest MagnifyMoney Savings Index indicates that 42% of consumers saved money in July, up from this year’s 35% low in June.

But rising inflation means many are pulling from their savings, too. In total, 17% took money from their savings in July — marking a new high this year.

MagnifyMoney surveys more than 1,000 Americans each month for its Saving Index. Keep reading to learn more about how consumer saving trends are shifting, including who’s most likely to save and why they’re doing it.

Key findings

- The percentage of Americans who added money to their savings account climbed from a 35% low in June to 42% in July. However, this is still the second-lowest percentage of savers so far this year.

- Consumers are starting to pull money from savings more frequently. In July, 17% of Americans say they withdrew funds from savings — the highest rate since December 2021.

- A higher rate of Gen Zers (61%) added money to savings in July than other generations. That compares with 45% of millennials, 35% of baby boomers and 32% of Gen Xers. Additionally, a higher percentage of men (49%) saved money than women (35%).

- More Americans are saving for emergencies compared to last summer, suggesting consumers take the possibility of a recession seriously. Nearly a third (31%) say they’re saving for emergencies, up from 25% in July 2021.

- Beyond general savings and emergencies, the top categories Americans are saving for are vacations (24%), retirement (21%) and new cars (17%). Additionally, although the holidays are months away, 14% of consumers have already started saving.

Savings are rebounding, but it’s still a summer slump

Consumers may be bouncing back from this year’s savings low. In total, 42% added to their savings in July, up from 35% in June — the lowest rate in 2022. While that’s a good sign, there are still fewer summer savers than their springtime counterparts. In fact, July had the second-lowest percentage of savers this year so far, down from a high of 47% in March.

Consumers’ savings aren’t necessarily going untouched, though. In fact, 17% of Americans say they pulled funds from savings, making July the month with the highest percentage of savings withdrawals so far in 2022. Consumers withdrew at lower rates in the springtime. During April and May — the 2022 months currently tied for the lowest percentage of withdrawals — just 13% of consumers took money from their savings.

Although there’s reason for caution, it’s worth noting that a higher rate of Americans saved money this July compared to the past two years. Just 37% saved money and 19% pulled from their savings in July 2021. Meanwhile, 40% saved money and 21% withdrew from their savings in July 2020. That indicates consumers generally have an easier time saving right now, according to DepositAccounts founder Ken Tumin, but that may change as consumers continue to feel the effects of inflation.

“Many consumers have been able to build up some savings, and now they’re focused on spending some of it rather than adding to it,” Tumin says. “If we don’t see a pullback in inflation soon, many consumers may feel forced to pull all or most of their money from savings to pay for more costly goods and services.”

Who’s most likely to save, and who’s most likely to withdraw?

The youngest age groups are particularly keen to grow their savings. Gen Zers ages 18 to 25 were more likely to add money to savings in July than any other demographic. Of this age group, just over 6 in 10 (61%) put money towards savings. That compares with:

- 45% of millennials ages 26 to 41

- 35% of baby boomers ages 57 to 76

- 32% of Gen Xers ages 42 to 56

In addition to being the age group least likely to have stashed away money in July, Gen Xers are also the most likely to say they don’t have any savings (24%). On the other hand, just 13% of Gen Zers don’t have any savings, making them the most likely group to have at least some money stashed away.

Meanwhile, a higher percentage of men (49%) put money toward their savings than women (35%). Residents of the Northeast (46%) saved more money than any other region, followed closely by Westerners (45%). That compares with 40% of Southerners and 38% of Midwesterners.

Parents were saving too, but those with younger children withdrew at higher rates than parents with adult children and those without kids. While just over 4 in 10 (42%) parents with children younger than 18 saved money, 20% withdrew money. That stacks up against:

- Parents with adult children: 34% saved money, 16% withdrew money

- Adults without children: 47% saved money, 16% withdrew money

With recession fears rising, more consumers are saving for emergencies

Nearly a third (31%) of Americans say they’re saving for an emergency, up from 25% in July 2021. Fears of an impending recession are likely driving many of these consumers. In fact, a recent MagnifyMoney survey on consumers’ recession beliefs found that 70% of Americans believe a recession is coming. Of these, a majority expect a recession in the next six months. Notably, 26% said they were building their emergency savings to prepare for it.

It’s good that so many Americans are building up their emergency funds, Tumin says, but consumers should ensure they’re contributing enough money with inflation on the rise.

“A job loss becomes more likely in a recession, and an emergency fund is especially important when you lose your job,” Tumin says. “A consumer’s emergency fund should afford them a few months’ worth of expenses. With high inflation raising expenses, consumers need to add more money to ensure their emergency savings are properly funded.”

Amid the stressors of a tumultuous economy, many Americans are also eager for a getaway. In total, 24% of consumers are saving for a vacation, making it the most popular category behind general savings and emergencies. Following that, consumers are saving for retirement (21%) and a new car (17%).

Consumers are increasingly budgeting for the holidays, too. This July, 14% say they’ve already started saving for the holiday season — up from 12% in July 2021 and 10% in July 2020.

Methodology

Every month, MagnifyMoney surveys consumers to find out whether they added money to their savings — and what they’re saving for. The results comprise the monthly MagnifyMoney Savings Index, which began in October 2019.

For the July 2022 edition, MagnifyMoney commissioned Qualtrics to conduct an online survey of 1,598 U.S. consumers ages 18 to 76 from July 8 to 15, 2022. The survey was administered using a nonprobability-based sample, and quotas were used to ensure the sample base represented the overall population. All responses were reviewed by researchers for quality control.

We defined generations as the following ages in 2022:

- Generation Z: 18 to 25

- Millennials: 26 to 41

- Generation X: 42 to 56

- Baby boomers: 57 to 76

Amid the stressors of a tumultuous economy, many Americans are also eager for a getaway. In total, 24% of consumers are saving for a vacation, making it the most popular category behind general savings and emergencies. Following that, consumers are saving for retirement (21%) and a new car (17%).

Consumers are increasingly budgeting for the holidays, too. This July, 14% say they’ve already started saving for the holiday season — up from 12% in July 2021 and 10% in July 2020.

This article originally appeared on Magnifymoney.com and was syndicated by MediaFeed.org

More from MediaFeed:

Is inflation ever a good thing for consumers?

Inflation is an economic trend in which prices for goods and services rise over time. The Federal Reserve uses different price indexes, including the Consumer Price Index, to track inflation and determine how to shape monetary policy. Generally speaking, the Fed targets a 2% annual inflation rate as measured by pricing indexes.

Rising demand for goods and services can trigger inflation when there’s an imbalance in supply. This is known as demand-pull inflation. Cost-push inflation occurs when the price of commodities rises, pushing up the price of goods or services that rely on those commodities.

Inflation can have both pros and cons for consumers and investors. Understanding the potential effects of inflation can maximize the positives while minimizing the negatives.

Related: Tips for creating a financial plan

Yingko/istock

Answering the question of whether inflation is good or bad means knowing more why inflation matters so much. The Federal Reserve takes an interest in inflation because of how it relates to the broader economic and monetary policy.

Some level of inflation in an economy is normal, and an indication that the economy is continuing to grow. While inflation has remained relatively low over the past decade, it has historically seen the most change during or right after recessions.

The Fed believes that its 2% target inflation rate encourages price stability and maximum employment.

Broadly speaking, high inflation can make it difficult for households to afford basic necessities, such as food and shelter. When inflation is too low, that can lead to economic weakening. If inflation trends too low for an extended period of time, consumers may come to expect that to continue, which can create a cycle of low inflation rates.

That sounds good, as lower inflation means prices are not increasing over time for goods and services. So consumers may not struggle to afford the things they need to maintain their standard of living. But prolonged, low inflation can impact interest rate policy.

The Federal Reserve uses interest rate cuts and hikes to keep the economy on an even keel. For example, if the economy is in danger of overheating because it’s growing too rapidly or inflation is increasing too quickly, the Fed may raise rates to encourage a pullback in borrowing and spending.

Conversely, when the economy is in a downturn, the Fed may cut rates to try to promote spending and borrowing. When both inflation and interest rates are low, that may not leave much room for further rate cuts in an economic crisis, which may spur higher employment rates. If prices for goods and services continue to decline, that could lead to a period of deflation or even a recession.

So, is inflation good or bad? The answer is that it can be a little of both. How deeply inflation affects consumers or investors–and who it affects most–depends on what’s behind rising prices, how long inflation lasts, and how the Fed manages interest rates.

fotopoly/istock

The Federal Reserve believes some inflation is good and even necessary to maintain a healthy economy. The key is keeping inflation rates at acceptable levels, such as the 2% annual inflation rate target. Staying within this proverbial Goldilocks zone can result in numerous positive impacts for consumers and the economy in general.

ThitareeSarmkasat/istock

Sustainable inflation can yield these benefits:

- Higher employment rates and steady paychecks for workers

- Continued economic growth

- Potential for higher wages if employers offer cost-of-living pay raises

- Cost-of-living adjustments for those receiving Social Security retirement benefits

The danger, of course, is that inflation escalates too rapidly, requiring the Federal Reserve to raise interest rates as a result. This increases the overall cost of borrowing for consumers and businesses.

CasPhotography/istock

Inflation can benefit certain groups, depending on how it impacts Fed shapes monetary policy. Some of the people who can benefit from inflation include:

- Savers, if an interest rate hike results in higher rates on savings accounts, money market accounts or certificates of deposit

- Debtors, if they’re repaying loans with money that’s worth less than the money they borrowed

- Homeowners who have a low, fixed-rate mortgage

- People who hold investments that appreciate in value as inflation rises

DepositPhotos.com

Some of the negative effects of inflation are more obvious than others. And there may be different consequences for consumers versus investors.

DepositPhotos.com

In terms of what’s bad about inflation, here are some of the biggest cons:

- Higher inflation means goods and services cost more, potentially straining consumer paychecks

- Investors may see their return on investment erode if higher inflation diminishes purchasing power, or if they’re holding low-interest bonds

- Unemployment rates may climb if employers lay off staff to cope with rising overhead costs

- Rising inflation can weaken currency values

Inflation can be particularly bad if it leads to hyperinflation. This phenomenon occurs when prices for goods and services increase uncontrolled over an extended period of time. Generally, this would mean an inflation growth rate of 50% or more per month. While hyperinflation has never happened in the United States, Zimbabwe experienced a daily inflation rate of 98% in 2008.

DepositPhotos.com

The negative impacts of inflation can affect some more than others. In general, inflation may be bad for:

- Consumers who live on a fixed income

- People who plan to borrow money if higher interest rates accompany the inflation

- Homeowners with an adjustable rate mortgage

- Individuals who aren’t investing in the market as a hedge against inflation

Inflation and higher prices can be detrimental to retirees whose savings may not stretch as far, particularly when health care becomes more expensive. If the cost of living increases but wages stagnate, that can also be problematic for workers because they end up spending more for the same things.

DepositPhotos.com

While inflation is an investment risk to consider, smart investing can minimize its impact on your portfolio. While savings accounts may yield more interest if the Fed raises interest rates, investing in stocks, exchange-traded funds (ETFs) or mutual funds could generate even higher returns.

Real estate and Treasury-Inflation Protected Securities (TIPS). Government-issued securities designed to generate consistent returns regardless of inflationary changes, can also be good buys during periods of rising inflation. If prices are rising, that can increase rental property incomes. You could benefit from that by investing in real estate ETFs or real estate investment trusts (REITs) if you’d rather not own property directly.

In general, compounding interest and the benefits of dollar-cost averaging over time can also help offset inflation. Compounding interest allows you to earn interest on your interest, which is key to building wealth. Dollar-cost averaging means investing continuously, whether stock prices are low or high. When inflationary changes are part of a larger shift in the economic cycle, investors who dollar-cost average can still reap long term benefits, despite rising prices.

1989_s/ istockphoto

Inflation is unavoidable but you can take steps to minimize the impact to your personal financial situation. Building a well-rounded portfolio of stocks, ETFs and other investments is a smart strategy for keeping pace with rising inflation.

Learn more:

This article originally appeared on SoFi.comand was syndicated by MediaFeed.org.

SoFi Invest

The information provided is not meant to provide investment or financial advice. Investment decisions should be based on an individual’s specific financial needs, goals and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC. SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below.

1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC Registered Investment Advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or pre-qualification for any loan product offered by SoFi Lending Corp and/or its affiliates.

utah778 / istockphoto

grinvalds / iStock

Featured Image Credit: wpd911.

AlertMe