Consumers in the U.S. have an average FICO Score of 703 and VantageScore of 711, but this can vary based on age.

Credit scores are determined based on a number of factors. Your FICO Score is primarily based on specific, weighted criteria including payment history (35%), outstanding debt (30%), credit history length (15%), pursuit of new credit (10%) and the types of credit you use (10%).

Regardless of your age, those who are initially building their credit score can start from 500 to 700, with those in their 20s having an average score of 660. The age group with the highest average credit score is those in their 80s, but it’s those between 56 and 74 that have the most consumers with a perfect score of 850. However, keep in mind that credit scores vary by age and due to a number of factors.

Consumers in the U.S. have an average FICO Score of 703 and VantageScore of 711, but this can vary based on age.

Credit scores are determined based on a number of factors. Your FICO Score is primarily based on specific, weighted criteria including payment history (35%), outstanding debt (30%), credit history length (15%), pursuit of new credit (10%) and the types of credit you use (10%).

Regardless of your age, those who are initially building their credit score can start from 500 to 700, with those in their 20s having an average score of 660. The age group with the highest average credit score is those in their 80s, but it’s those between 56 and 74 that have the most consumers with a perfect score of 850. However, keep in mind that credit scores vary by age and due to a number of factors.

Credit Scores by Age Snapshot

- The average FICO Score is 703, while the average VantageScore is 711.

- Consumers who hit their 50s experience a significant increase in their credit score, reaching an average score of 703 and above.

- Credit scores can also vary based on your location — Louisiana has the lowest average credit score in the U.S., while Minnesota has the highest.

What Is the Average Credit Score by Age in the U.S.?

The average credit score in the U.S. stands at 703 as of the second quarter of 2019, but this is not the same for everyone. For instance, Louisiana has the lowest average credit score of 685 in the U.S., while Minnesota has the highest average at 739.

Your age can also indirectly play a role in your score. While age itself is not a factor used in credit scoring reports, the age of your accounts is. The older you are, the older your accounts are and the higher your credit score is, mostly due to your extensive payment history. As people reach retirement age, they generally have less debt, which can improve credit scores.

Different age groups have varying averages, with consumers in their 20s having the lowest average score at 660. Those in their 60s have a significantly higher score as they’ve built it over many years, with their average credit score standing at 733. Scores increase the most between 40 to 69, jumping an average of 20 points in each decade.

What Ages Have the Most Perfect Credit Scores (850)?

Achieving a perfect credit score of 850 is a goal for many consumers. After all, it can help them attain better loans, credit card offers and utility discounts. Roughly 58% of consumers with a perfect credit score of 850 are between the ages of 56 and 74. This score is two steps up from the average FICO score of 703, which is ranked as “good” by Experian.

Between 56 and 74, consumers are more likely to have an increased income. This can help them pay off a significant amount of debt and contribute to an increase in their score. Conversely, they may have also already paid off most of their debt and have lowered their credit utilization ratio, which has a significant impact on credit scores next to payment history.

While achieving a score of 850 is ideal, it isn’t needed to get better interest rates or offers. Getting a score of 760 or “very good” is enough to give you access to better interest rates or credit card reward options.

What’s a Good Credit Score for Your Age?

As you age and increase your payment history, increasing your credit score should be part of your goals. While you can do many things to speed up the process and have a better credit score, a good credit score keeps up with the national average. In your 20s and 30s, a good credit score is between 663 and 671, while in your 40s and 50s, a good score is around 682. To get the best interest rates, terms and offers, aim for a credit score in the 700s.

In your 20s, you’re only just starting to build your credit score, which is why it may be difficult to get the same average score of 754 that those in their 70s achieve. A number of factors can affect your score over time, such as your payment history, credit history length and revolving balance. Credit bureaus have a better idea of your creditworthiness if you have a long payment history of on-time payments.

In the meantime, focus on reducing your debt and improving your credit score by making on-time payments, reviewing your credit regularly and keeping your credit utilization as low as possible.

Average Credit Scores for People in Their 20s

The average FICO credit score for those in their 20s is 660. Between the ages of 20 and 29, consumers are starting to build their scores. These consumers may have a low-limit student credit card and are making payments towards their student loans. A low income, short payment history and higher utilization could be why their average score is on the lower side of the credit score spectrum.

Average Credit Scores for People in Their 30s

Consumers’ FICO Scores begin to grow in their 30s, increasing steadily by 14 points between the ages of 30 and 39. By this age, their incomes are growing as they establish their careers. Many in this age group have a mortgage or auto loan, which can help diversify credit beyond credit cards and student loans.

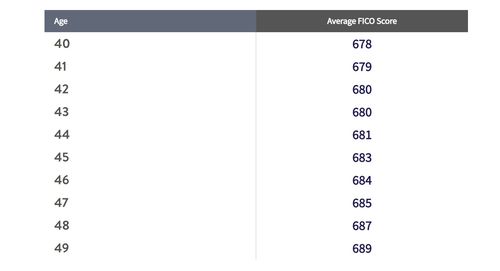

Average Credit Scores for People in Their 40s

Consumers’ average FICO Scores improve by 11 points in their 40s and reach an average of 689 by age 49. Around this age, consumers may be co-signing student loans with their children and looking at refinancing options, such as debt consolidation, to reduce debt and prepare for retirement.

Average Credit Scores for People in Their 50s

Credit scores continue to climb, and at a higher rate, throughout the consumers’ 50s. During this time, credit scores increase by 24 points from age 50 to 59. Consumers in their 50s are at their peak earning years and focusing more on retirement. They may be paying off any leftover debt to eliminate payments before retiring from their jobs.

Average Credit Scores for People in Their 60s

The average FICO Score grows by an even greater margin during the consumers’ 60s, increasing by 27 points, from 719 at age 60 to a high 746 by age 69. Around their 60s, consumers’ accounts will have aged considerably, and they have a long track record of payments. Many in this bracket have paid off their mortgage, credit cards and other debt that can affect their credit scores.

Average Credit Scores for People in Their 70s and Older

Once consumers hit their 70s, their average FICO scores will slowly plateau, getting closer to the perfect 850. Around this age, the Equal Credit Opportunity Act (ECOA) permits credit scoring models to favor certain age groups, specifically those over the age of 62. However, this age group is also likely to use credit less to avoid gaining more debt since they are now living off of Social Security, pensions and their retirement savings.

MONEYGEEK QUICK TIP: Regardless of your age, it’s important to cut back on unnecessary expenses where possible. Having monthly savings can be used to pay down debt, invest for retirement or contribute to an emergency fund to avoid overspending on credit cards.

At What Age Does Credit Score Improve the Most?

Consumer credit scores start jumping significantly between their 30s and 40s, but the biggest increase is seen between one’s 50s and 60s, a significantly large 30-point jump.

By their 40s, consumers’ accounts have aged enough to warrant a higher score increase. However, their debt levels peak and those in their 40s often have to contend with multiple credit accounts, such as their credit card, student loan and mortgage. These reduce significantly in their 60s, as debts may likely have been paid off or refinanced, and credit card debt isn’t accumulated as much due to retirement. Due to the ECOA, credit bureaus will also look at those beyond the age of 62 more favorably.

Credit Invisibility

Around 26 million consumers in the U.S. are said to be credit invisible, which means they have no recorded credit history or report at any of the three major credit bureaus (Experian, TransUnion and Equifax).

It’s a given that records will be limited for those 19 and below, with over 80% having unscored records. This drops by 40% once they reach their 20s and lowers over time, as consumers open credit accounts and take out loans. However, most consumers who are credit invisible are generally young, which may be a result of lack of income or other circumstances.

The number of credit invisible consumers increases at around age 60, caused by insufficient recent information. It’s also possible that those born before 1950 had thinner credit records throughout their careers, which reflected less credit reporting during the years when they were actively consuming credit.

Other Questions You May Have About Average Credit Scores

Credit scores can be a tricky subject. Below are a few common questions when it comes to understanding what happens to your average credit score as you age.

What’s the average credit score for an 18-19-year-old?

The average credit score in the U.S. for those between 18 and 23 is 674.

What’s the average credit score for a 21-year-old?

21-year-olds have an average credit score of 670.

What’s a normal credit score for a 25-year-old?

Consumers aged 25 have a median credit score of 659, which is lower than what they might experience in their early 20s. This may be due to opening new lines of credit or how they manage their finances.

What’s the average credit score for a 30-year-old?

At 30, the average credit score is 663. This is three points higher than the average score of a 29-year-old.

Why do younger people have lower credit scores compared to people in their 50s and 60s?

Young people often experience far lower credit scores compared to their older counterparts due to the lack of a significant credit and payment history. As those in their 50s and 60s have had their accounts for longer, credit bureaus have gathered enough activity to give them a more accurate credit score that reflects their credit-worthiness.

What percent of the U.S. population has no credit score?

62 million, or 11% of the U.S. population, are credit invisible with an additional 19.4 million having credit records that are “unscorable.” This makes up 45.5 million or almost 20% of the U.S. population.

Is a 700 credit score average?

A score of 700 is considered “good” across the different credit bureaus.

Related:

More from MediaFeed:

The average credit score & credit card debt by state

Fair Isaac Corp.’s FICO Score and VantageScore are two of the most widely used scoring models in the country. Both models range between 300 and 850 — and the higher the score, the better. The average credit score varies greatly among different populations, ages and income levels, some of which are explored below.

The average credit score in the U.S. is at an all-time high of 711. This coincides with what the Consumer Financial Protection Bureau defines as “prime.”

About 1 in 5 American adults either have no credit history (“credit invisible”) or are unscorable. As a result, these individuals will have difficulty obtaining new lines of credit.

In the eyes of lenders, credit scores fall into several buckets, which indicate how risky it may be to extend credit to an individual. Outside of playing a role in approvals for a loan or credit, these scores can also impact an individual’s lending terms. Perhaps the most important terms among those are interest rates.

The higher an individual’s credit score, the lower their quoted APR will typically be.

FICO credit scores break down in the following manner:

- 800 to 850: Exceptional

- 740 to 799: Very good

- 670 to 739: Good

- 580 to 669: Fair

- 300 to 579: Very poor

This means the average credit score of 711 is in the good range.

Though the average credit score has generally improved since 2005, slight dips were seen around the Great Recession that ended in 2009. A large number of people declaring bankruptcy or defaulting on their loans would have caused their credit scores to plummet, which in turn would have affected the overall average.

DepositPhotos.com

Millennials (ages 24 to 39) have an average credit score of 680, while baby boomers (ages 56 to 74) have an average credit score of 736.

The average FICO Score tends to improve with age.

The average credit scores coincide with the financial situations facing younger generations. It’s usually around the millennial age range that major expenses and debt begin to rack up — such as weddings and first mortgages, among others. Despite their ages, millennials hold an average of $4,322 in credit card debt.

The other age group whose average credit score skews lower is Generation Z (ages 18 to 23). A contributing factor to this is the limited access to credit this age group faces. Following the 2009 CARD Act, it became significantly harder for 18- to 21-year-olds to open new credit card accounts. As a result, many young adults don’t begin building a credit file until later in life — driving averages down.

Americans of all ages owe debt. In fact, U.S. household debt spiked to $14.35 trillion in the third quarter of 2020 — the latest available data — amid the coronavirus pandemic, according to the Federal Reserve Bank of New York.

And that debt is growing while more people remain out of work. The federal unemployment rate was 3.5% in February 2020 before spiking to 14.8% in April 2020. (It’s been dropping but was still at 6.7% in December 2020.)

Experian / Value Penguin

The higher one’s income level, the higher their average credit score tends to be.

While debt-to-income ratio doesn’t play a direct role in determining one’s credit score, it does have an indirect one. One of the factors lenders consider when modeling an individual’s credit risk is their credit utilization — the percentage of total available credit a consumer is using month to month.

To improve one’s credit score, credit utilization should generally be kept below 30%. The lower one’s income is, the more a consumer may rely on their credit for their expenditures.

Another way income may play into credit utilization, and ultimately one’s credit score, is by determining one’s credit limit. Credit issuers look at borrowers’ incomes when deciding on the amount of revolving credit that should be issued.

The lower one’s income, the lower their line of credit is likely to be.

In turn, by having significantly lower credit limits, it becomes easier for lower-income individuals to eat up a larger portion of what’s available, increasing their credit utilization.

The graphic belows shows that median credit scores are highly correlated to income.

For context:

- Low income: Up to 50% of the area median income

- Moderate income: Greater than 50% and up to 80% of the area median income

- Medium income: Greater than 80% and up to 120% of the area median income

- High income: More than 120% of the area median income

Aside from the ability to make monthly payments on time, which may be difficult, people with lower incomes have access to less credit, meaning their credit utilization would be higher with smaller debt. This, in turn, lowers credit scores, which can, in turn, lower credit availability.

Below are the average credit scores throughout the U.S. by ranking.

Federal Reserve Bank of New York / Value Penguin

- Average credit score: 675

- Average credit card debt: $4,587

SeanPavonePhoto/istockphoto

- Average credit score: 684

- Average credit card debt: $5,127

DenisTangneyJr

- Average credit score: 686

- Average credit card debt: $5,047

Sean Pavone

- Average credit score: 688

- Average credit card debt: $5,848

DenisTangneyJr

- Average credit score: 689

- Average credit card debt: $5,310

SeanPavonePhoto

- Average credit score: 689

- Average credit card debt: $5,693

SeanPavonePhoto

- Average credit score: 690

- Average credit card debt: $5,271

DepositPhotos.com

- Average credit score: 690

- Average credit card debt: $4,791

Tara Ballard

- Average credit score: 694

- Average credit card debt: $4,948

Davel5957

- Average credit score: 695

- Average credit card debt: $4,686

hkim39 // istockphoto

- Average credit score: 695

- Average credit card debt: $5,422

Byelikova_Oksana / istockphoto

- Average credit score: 697

- Average credit card debt: $5,006

NathanMerrill

- Average credit score: 698

- Average credit card debt: $4,521

Thomas Kelley

- Average credit score: 701

- Average credit card debt: $5,623

Elisa.rolle

- Average credit score: 703

- Average credit card debt: $5,121

” Darwin Brandis”

- Average credit score: 706

- Average credit card debt: $5,157

wanderluster

- Average credit score: 707

- Average credit card debt: $4,651

f11photo

- Average credit score: 707

- Average credit card debt: $4,950

eyecrave

- Average credit score: 710

- Average credit card debt: $5,462

mdgmorris

- Average credit score: 711

- Average credit card debt: $4,888

dypics

- Average credit score: 712

- Average credit card debt: $5,977

James_Lane

- Average credit score: 713

- Average credit card debt: $5,671

DepositPhotos.com

- Average credit score: 714

- Average credit card debt: $6,617

Chilkoot

- Average credit score: 714

- Average credit card debt: $4,692

haveseen

- Average credit score: 716

- Average credit card debt: $5,120

mlauffen

- Average credit score: 716

- Average credit card debt: $5,365

ibsky

- Average credit score: 717

- Average credit card debt: $5,063

Zillow

- Average credit score: 717

- Average credit card debt: $5,992

DenisTangneyJr

- Average credit score: 718

- Average credit card debt: $5,414

Eloi_Omella

- Average credit score: 719

- Average credit card debt: $5,256

danlogan

- Average credit score: 719

- Average credit card debt: $5,182

AnujSahaiPhotography

- Average credit score: 720

- Average credit card debt: $4,582

Zillow

- Average credit score: 720

- Average credit card debt: $5,080

AppalachianViews

- Average credit score: 721

- Average credit card debt: $4,676

DepositPhotos.com

- Average credit score: 721

- Average credit card debt: $5,978

aimintang

- Average credit score: 723

- Average credit card debt: $6,040

traveler1116

- Average credit score: 723

- Average credit card debt: $4,900

” 4kodiak”

- Average credit score: 725

- Average credit card debt: $5,541

Jacob Boomsma / istockphoto

- Average credit score: 726

- Average credit card debt: $4,289

JoeChristensen

- Average credit score: 726

- Average credit card debt: $4,785

YinYang

- Average credit score: 727

- Average credit card debt: $5,614

Art Wager

- Average credit score: 727

- Average credit card debt: $4,681

HaizhanZheng

- Average credit score: 728

- Average credit card debt: $4,819

HaizhanZheng

- Average credit score: 729

- Average credit card debt: $5,141

Rolf_52

- Average credit score: 729

- Average credit card debt: $5,327

DenisTangneyJr

- Average credit score: 730

- Average credit card debt: $4,865

sequential5

- Average credit score: 730

- Average credit card debt: $5,238

4nadia

- Average credit score: 731

- Average credit card debt: $4,633

Rex_Wholster

- Average credit score: 731

- Average credit card debt: $4,653

DenisTangneyJr

- Average credit score: 732

- Average credit card debt: $4,376

FierceAbin

- Average credit score: 739

- Average credit card debt: $4,767

Related:

This article originally appeared on ValuePenguin.comand was syndicated by MediaFeed.org.

JoeChristensen

Featured Image Credit: DepositPhotos.com.

AlertMe