Owning a home in a coastal area may be appealing, but the reality is less attractive if there is damage during hurricane season. If you’re buying a house in a hurricane zone, knowing how flood insurance works and how to prepare before a storm hits could save money, and more importantly, your life.

What is a hurricane zone?

Hurricane zones are areas of the United States where hurricanes are most likely to make landfall. Residential and vacation homes are located within coastal hurricane zones stretching from the Gulf of Mexico in Texas to the Atlantic Ocean near Maine. Hurricane season starts June 1 and ends Nov. 30 every year.

Hurricanes are known for wind speeds ranging from 74 to 157 mph. “Wind damage to roofs is probably the most common loss,” said Loretta Worters, vice president of media relations for the Insurance Information Institute. “There can be trees that fall onto the home’s structure.”

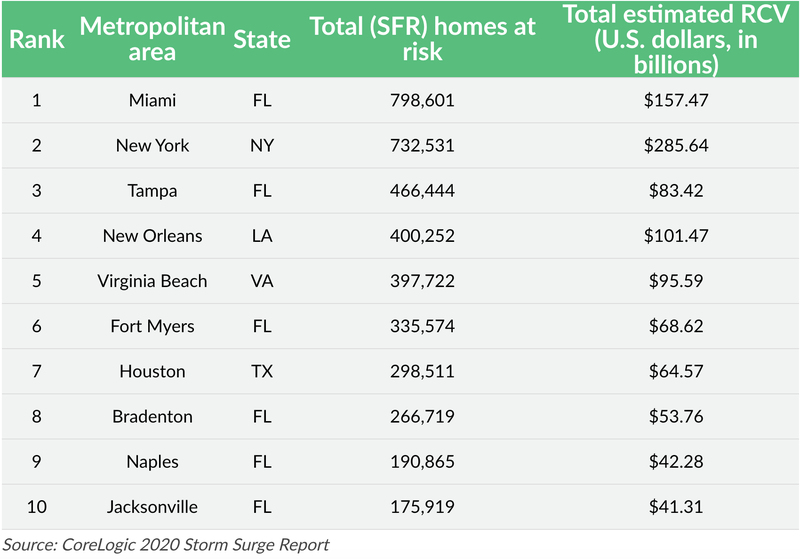

However, it’s the abnormal rise of water the storm generates that typically causes the most property damage. This is known as storm surge, and according to CoreLogic’s 2020 Storm Surge Report, more than 7.1 million single-family residences are at risk of flood damage from this year’s hurricane season.

The table below reflects the top 10 metropolitan areas threatened by potential flood damage. It also estimates the reconstruction cost value (RCV) if the homes are completely destroyed.

Can you buy a house in a hurricane zone?

The simple answer is yes, but mortgage financing options will be limited and you may pay expensive flood insurance premiums. If your home is listed for sale, the seller’s real estate agent should disclose:

- Whether the home is in an area that requires flood insurance

- Whether home is in an area prone to flood risk

- Whether nearby owners typically purchase flood insurance

- Whether flood insurance was required in the past

- Whether the home was previously in a flood plain

Always get a home inspection to confirm there aren’t traces of flood damage, such as mold and mildew. Flood information disclosure laws vary by state; you can review disclosures applicable to your area using the National Association of Realtors (NAR) state flood hazard disclosures survey.

What hurricane zone am I in?

To determine the hurricane zone map in which your property sits, input your address into the Federal Emergency Management Agency (FEMA) flood map service center. The maps may change over time based on weather patterns, natural erosion or new housing developments.

If you’re buying a home in a hurricane zone it’s likely in a Special Flood Hazard Area (SFHA) beginning with the letters A or V on a FEMA flood map. If you need a traditional mortgage to purchase your home, you’ll have to buy flood insurance before the loan closes.

How much is flood insurance if your house is in a hurricane zone?

The average yearly cost of flood insurance purchased through the National Flood Insurance Program (NFIP) is $708, according to ValuePenguin. Standard homeowners insurance policies don’t usually cover flood damage. The NFIP offers both building and contents coverage.

Your deductible for hurricane coverage may be significantly higher than a standard homeowner’s insurance policy. “A standard homeowners policy deductible typically is $500 to $1,000,” Worters said. “Hurricane deductibles apply only to damage caused by hurricanes, and typically range from 1% to 5% of the insured value of the home,” Worters said.

- How much you’ll pay for flood insurance depends on:

- What flood zone you’re in

- The type of coverage you need (building and/or contents)

- The amount of the deductible

- The amount of building and contents coverage you buy

- The location of your home

- The year the home was built

- Where the contents of the home are located (basement, bottom floor, middle floor, etc.)

Smart tip: Don’t wait until a storm is headed your way to buy flood insurance. It can take up to 30 days for a policy to go into effect.

What’s covered by a flood insurance policy?

“A typical federally backed policy from the NFIP provides $250,000 for the structure and $100,00 for the contents,” Worters said.

For homes that cost more than NFIP coverage limits, supplemental insurance is recommended. Coverage is available from what’s called “surplus lines insurance,” with much higher limits ($1 million or more), Worters added.

The table below provides examples of what’s protected by standard flood coverage for a building and its contents:

Protected by building coverage:

- Electrical, plumbing, furnaces and water heaters

- Refrigerators, cooking stoves and dishwashers

- Permanently installed carpet, cabinets and bookcases

- Foundation walls, detached garages and staircases

Protected by contents coverage:

- Curtains, washers, dryers and microwave ovens

- Valuable items, including artwork

- Window or portable air conditioners

8 tips for reducing your flood insurance premiums

There are simple ways to reduce your flood premium if you’re buying a home in a hurricane zone. An added bonus: These tips may also help reduce damage to your home. The key is to keep the major structure and components of your home above the base flood elevation (BFE). The BFE tells flood insurers whether there’s a 1% chance water could rise above a set level in a given year, potentially causing flood damage.

- Choose a higher deductible amount. You could receive up to a 40% reduction in your annual premium by choosing a policy with the maximum $10,000 deductible. Make sure you’ve stockpiled the cash reserves to cover the deductible cost if your home is severely flood-damaged.

- Buy a brick home. “You will pay more for a wood structure than you would a brick structure in coastal areas,” Worters said.

- Get an elevation certificate (EC). An EC shows the insurance company how the property is built in relation to the local flood map. If your home is built above the highest floodwater level, you may get a discount on your premium.

- Raise up your utilities. Elevating anything connected to an electrical panel like air conditioning, water heaters and other utilities above the BFE will save you the annual surcharge you’d pay otherwise.

- Fill up the basement. The NFIP normally won’t cover damage to basements for newly built homes located in hurricane zones. Filling the basement with gravel or soil, for example, could reduce flood premiums by 15% to 20%.

- Add flood openings. The NFIP offers premium reductions to borrowers with flood openings installed in basements. The premium may also be applied to openings added to other fully enclosed areas, like garages or windows, below the lowest elevated floor in the home.

- Shop around for the best insurance rates. Get homeowners insurance quotes from multiple companies. And when shopping for flood insurance, make sure you ask about the company’s claims process. The sooner your claim is settled, the sooner you can get help.

- Strengthen your home with hurricane-resistant retrofits. The Insurance Institute for Business & Home Safety provides a list of upgrades to fortify your home against a hurricane’s impact. Many insurers accept those types of retrofits and provide you with a credit to lower your insurance policy costs, said Tom Larsen, senior director of content strategy for insurance solutions at CoreLogic.

Preparing for a hurricane during the COVID-19 pandemic

You’ll need a place to stay if you’re evacuated, and shelter locations may have changed due to the COVID-19 pandemic. Additionally, hotels and restaurants may not be fully operational due to social-distancing restrictions, depending on which state you live in. Planning in advance could prevent dire circumstances for you and your family.

Stock up on groceries. The Department of Homeland Security recommends you build a disaster supply kit complete with water, food and other survival tools like batteries, flashlights and local maps. “Have your go bag and your clothes and whatever you need to sustain yourself for three to five days,” Larsen suggested.

Learn about local hurricane evacuation zones. Listen to the radio, TV or state police to find out if there are specific routes you should take if a hurricane is approaching.

Find your contractors ahead of time. The time to call hurricane shutter installers is not when a hurricane is days or hours away. If your area is prone to major storms, the sooner you have protection devices set up, the better.

Scope out options for shelter in advance. Hotels and Airbnbs may fill up quickly, especially in states where capacity is limited to prevent the spread of the coronavirus. If you’re in a COVID-19 hotspot, discuss an evacuation plan with friends and family. Contact the American Red Cross in your area to find out about shelter options.

Keep numbers and locations of hospitals handy. Hospitals struggling to keep up with the needs of COVID-19 patients may not have the staff to help people affected by a hurricane. Make sure you have more than one urgent care option in neighboring cities or even states.

Learn your insurance company’s claims process. Ask your insurance agent if they offer a virtual claims process. If they do, you may be able to take pictures of the damage with your phone to move the claims process along, said Larsen.

Have your mortgage company contact information accessible. You may be eligible for mortgage help if your home is in a designated natural disaster area. Call your mortgage servicer right away if your home is damaged.

This article originally appeared on LendingTree.com and was syndicated by MediaFeed.org.

Featured Image Credit: Karl Spencer.

AlertMe