A down payment and a strong cosigner are usually the best ways to get a car loan with bad credit. It may seem challenging to find a bad credit car loan, but there are many lenders willing to work with borrowers who have poor or damaged credit. The challenge is finding an affordable rate and avoiding any scams along the way. Following these steps could help increase your chances of getting approved for an auto loan with a rate and terms that work for you.

Steps for getting a car loan with bad credit

You could go straight to a dealership and apply for a loan, but there could be a better way to get your most affordable bad credit auto loan.

Image Credit: ipuwadol.

Step 1: Check your credit

There may be an error dragging down your credit score. Check your credit history for free at AnnualCreditReport.com to make sure that there are no mistakes.

If there are mistakes, here’s how to dispute a credit report error. You’ll need to write to the credit bureaus that show the error and the financial institution that gave the incorrect report. Keep copies of the correspondence you send. Once credit reporting agencies receive a dispute, they must investigate and report back to you within 30 days. If you are unsatisfied with the investigation, you could issue a complaint to the Consumer Financial Protection Bureau.

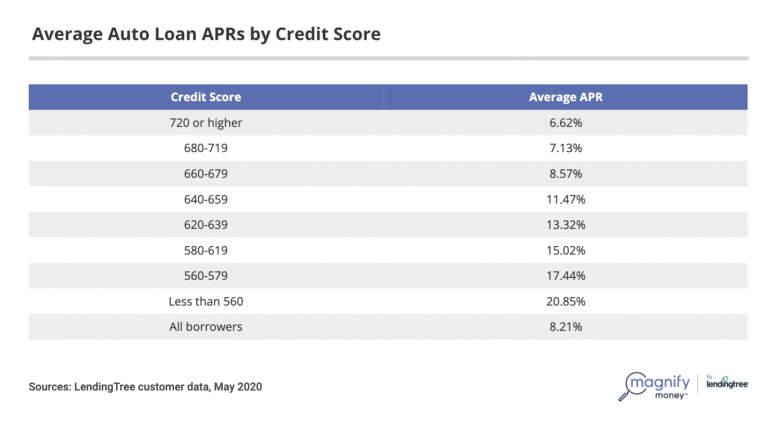

Credit history vs. credit score

Negative information on your credit report can affect your credit score. There are several ways to check your score. When you know your score, you’ll have a general idea about the APR you may receive. While there’s no set minimum credit score for buying a car, the rule of thumb is this: The higher your score, the lower your auto loan rate.

Image Credit: MagnifyMoney by LendingTree.

Step 2: Set a car budget

As the modern marvels of machinery that they are, cars are expensive. Americans with the lowest credit scores borrow an average of $15,845 for used cars and $27,867 for new cars. It’s vital to make sure your vehicle is affordable to you. You could use the 20/4/10 rule as a guideline for your car-buying budget: Put 20% down, finance for no more than four years and keep your total transportation costs under 10% of your income.

| 20/4/10 Rule Example | |

|---|---|

| Gross monthly income |

$4,000 |

| 10% of gross income |

$400 |

| Average cost of car insurance |

$78 |

| Estimated cost of fuel |

$50 |

| Estimated cost of maintenance |

$10 |

| Recommended monthly car payment |

$262 |

Your car ownership costs will vary, but you could use a car affordability calculator to see what could fit in your budget. If you want to get a professional’s opinion on your credit and budget situation before buying a vehicle, the National Foundation for Credit Counseling offers free and low-cost credit counseling.

Image Credit: DepositPhotos.com.

Step 3: Save a down payment and look for a cosigner

While it’s possible to find a bad credit car loan with zero down payment, we recommend buyers give a down payment, no matter their credit. Down payments can:

- Increase the likelihood that a lender will make you a loan offer

- Possibly lower your APR

- Prevent your car loan from being underwater

The traditionally-recommended down payment is 20% of the car’s price. How much you actually put down is up to you. If you’d like help saving, here are some of the best money-saving apps listed on our site.

A cosigner could help

If you’re having trouble getting approved for a car loan or a car loan at the rate and terms you prefer, a cosigner could help. The downsides are that a cosigner is risking their own credit and possible fees should you default on the loan.

Image Credit: wutwhanfoto / iStock.

Step 4: Research lenders and get pre-approved

Potential lenders could include your own bank, credit union or online lender. We looked at more than 100,000 subprime auto loan applications and chose the three top bad credit car loan lenders based on popularity and average APRs borrowers received.

| Best Lenders for Bad Credit Car Loans | |||

|---|---|---|---|

| Lender | Average APR for Subprime Borrowers | Amounts | Terms |

| Capital One |

12.50% |

$4,000+ | 36-84 months |

| RoadLoans |

17.84% |

$5,000 – $75,000 | Up to 72 months |

| Carvana |

19.39% |

Not available | 36-72 months |

Source: LendingTree customer data, Q2 2020

Whichever lender you choose, we recommend applying for a preapproval — ideally, more than one — before you go to a dealership. Dealers can and often do raise a customer’s interest rates. Ergo, it’s best to cut out the middleman and apply directly to a lender.

Consider a personal loan instead

If you’re having trouble getting a car loan, a personal loan might be an option. The pros of using a personal loan to buy a car include flexible loan amounts and no restrictions on vehicle age or mileage. However, personal loans tend to have higher APRs than auto loans.

Image Credit: Drazen Zigic/iStock.

Step 5: Negotiate at the dealership

By getting a loan preapproval, you can walk into the dealership focused on getting your best price possible on your new car. Dealers will try to distract you with their own loan offers and talk of monthly payment. A car-buying secret is to keep your focus on the total price of the vehicle. Once that’s set, see if the dealer can beat your preapproved loan rate. Pay attention to how long the loan term is. Even with a lower rate, you may end up paying more in interest over a longer loan.

Here’s more on how to negotiate car price and when to walk away.

Image Credit: PeopleImages.

Step 6: Sign and set up automatic payments

Finalize the paperwork with the seller and drive off with your car. You may have up to 30 days from the day you sign until your first payment and it may take almost that long for your state government to process the paperwork and get the permanent vehicle registration to you.

Some lenders will offer you the chance to sign up for automatic payments at the same time as when you sign for the car loan. Other lenders will contact you regarding payment methods.

We recommend setting up automatic payments so that it’s easier to make all payments on time. You’ll still be able to pay off your car loan faster, if you choose.

Refinance for a better rate later. Paying your car loan on time could help increase your credit score and decrease the amount you owe. You could refinance your bad credit car loan to a better rate after roughly two years, give or take.

Image Credit: Depositphotos.

Avoid bad credit car loan scams

Buy-here, pay-here dealerships advertising “No credit? Bad credit? No problem!” often come with high rates and fees. They know that many customers who walk in may not qualify at traditional dealerships and instead depend on used-car businesses that serve as their own banks.

“In general, buy-here pay-here financing is just overpriced junk,” said Rosemary Shahan, founder of Consumers for Auto Reliability and Safety (CARS) Foundation. “There are just too many games that they can play.”

Some in-housing financing may be reputable, but unscrupulous businesses have been known to use these tactics:

Image Credit: DepositPhotos.com.

Yo-yo financing

Yo-yo financing is when dealers allow you to sign a contract at one rate, and then change the terms of the contract a few weeks after you’ve taken the vehicle home. They usually claim that the “financing fell through” and you need to sign a new contract at a higher interest rate.

To protect yourself, keep copies of all loan documents you sign, and don’t drive away with a car until you’ve signed for it.

Image Credit: DepositPhotos.com.

Fees, overpriced extras

There are dealer fees that can’t be avoided, then there are fees you typically won’t find with traditional lenders, such as loan origination charges or steep late payment fees. These may come on top of overpriced extras. If you want add-ons like extended warranties, do your research ahead of time. You’ll most likely find them elsewhere for less.

Image Credit: DepositPhotos.com.

Undervalued trade-ins

Your old vehicle is an asset and you should get as close to Kelley Blue Book value as possible if you decide to trade it in. Some shady dealers will undervalue your vehicle, leaving you with less money to put toward your new car. Financing a larger amount than necessary at high rates and fees is exactly what the unscrupulous dealer is hoping for. A private sale will almost always yield the biggest bang for your buck, but that might be inconvenient for you.

Image Credit: iStock.

Mechanically unsound vehicles

Some unscrupulous used car dealers sell lemon vehicles to unsuspecting customers and worse, label them “certified pre-owned.” Legitimate CPO vehicles are generally sold through franchised dealers with the automaker’s seal of approval. Protect yourself by checking for safety recalls. If the dealer doesn’t provide a vehicle history report (VHR), there are several places you can buy a VHR for yourself.

Remember, once you’ve purchased the vehicle, it’s very difficult to return it.

Image Credit: DepositPhotos.com.

Bad credit car loan FAQs

Should I buy a new or used car?

When considering whether to buy a new or used vehicle, we often recommend used. Due to depreciation, buying a three-year old vehicle can mean you only pay about half of what the vehicle costs new, and the car still has most of its life span left. Borrowing less for a car may also increase your loan approval chances.

Should I get an 84-month car loan?

We do not recommend 84-month car loans. Yes, it’s a way to lower your monthly payment, which may be important in finding an affordable auto loan. But the risks usually outweigh the benefits: higher interest charges plus a greater likelihood that you’ll wind up underwater on your car loan. By the end of those seven years, you could be on the hook for monthly car payments and repair costs.

Can I buy a car before declaring bankruptcy?

We don’t recommend this either — purchasing a car before filing for bankruptcy can be seen as a sign of fraud. You may be able to buy a car during your bankruptcy.

Can I buy a car after declaring bankruptcy?

Yes, but it might be best to wait a year or two instead of immediately getting a car loan after a bankruptcy is discharged. This could allow you to attain a car loan with lower interest.

What happens if I don’t get approved for an auto loan?

If you don’t get approved for an auto loan, ask the bank why. Do you have insufficient income? Do you have a recent auto repossession on your credit report? Finding out why could help you fix the problem. Just because one lender didn’t provide a loan offer, doesn’t mean you can’t get a car loan.

Do I need a cosigner for a bad credit car loan?

This depends on the lender and your application. Some banks, credit unions or online lenders will not lend to you unless you have a cosigner. The cosigner agrees to pay for your loan if you stop making payments. If you have low income and bad credit, you’ll probably need a cosigner.

Editorial Note: The content of this article is based on the author’s opinions and recommendations alone. It may not have been previewed, commissioned or otherwise endorsed by any of our network partners.

This article originally appeared on MagnifyMoney.com and was syndicated by MediaFeed.org.

Image Credit: DepositPhotos.com.

AlertMe