You read that right, I have six bank accounts that I use on a monthly basis. I have had more in the past and the number of accounts fluctuates depending on what is going on in my life. Keep reading to see why I have six bank accounts and why you may even need more!

Image Credit: fizkes / iStock.

Add structure to your financial plan

It is extremely important we have a structure built for our personal finances in order to be successful with them. I went years with having two bank accounts. One checking account and one savings account. Money was directly deposited into my checking and I paid for all my bills out of there. If there was any money left at the end of the month, I might move some of it to my savings account.

Needless to say, when I managed my finances this way I was going nowhere fast. I wasn’t saving really anything and I spent what I made. As long as there wasn’t a negative balance in my checking account at the end of the month, I was happy.

It turns out, most people manage their finances this way. I was normal and didn’t know any better. Now that I’m older and (hopefully) wiser, I now use a minimum of six bank accounts – and sometimes more!

Before I go into the “why”, let me show you how my current bank account system is set up…

Image Credit: DepositPhotos.com.

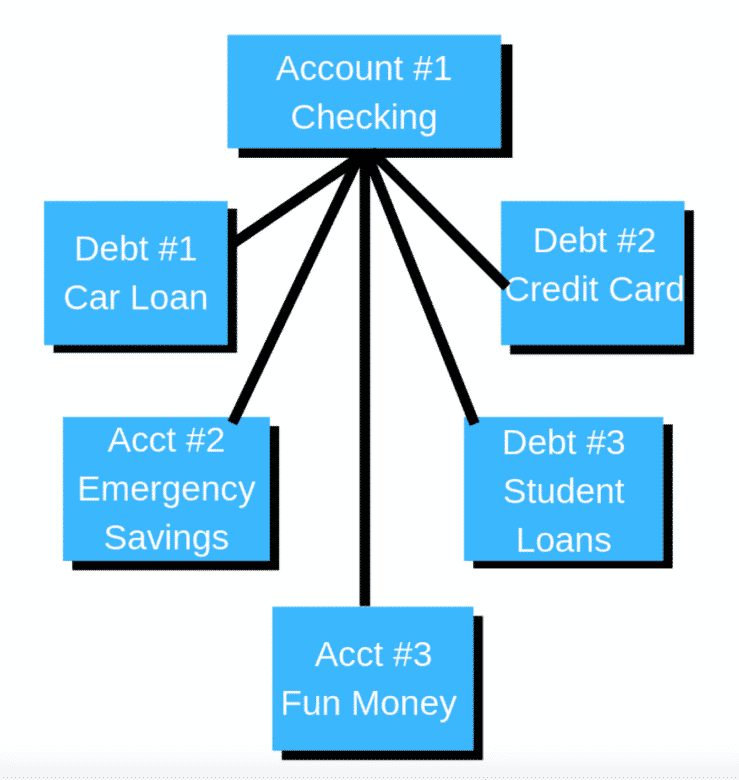

My current bank account setup

My first account is my checking account. After all my pretax money is taken out of my check for retirement, health insurance, and my health savings account, the money is directly deposited into my checking account.

Image Credit: Ryan Luke.

Move your money at the beginning of the month

At the beginning of the month, my wife moves money around into each separate savings account. By moving the money at the beginning, it forces us to stick to our budget for the remainder of the month, which isn’t hard if you incorporate a simple monthly budget template into your financial planning.

Most people manage their money in a backward manner. At the end of the month is when money is moved. Whatever is left in the checking account is then disbursed into any liabilities or savings. The problem with this method is it is too easy to overspend. Just like when I was younger, I usually spent what I made because the money was easy and accessible.

If you move your money at the beginning, it makes it much more difficult to overspend if you don’t have the money in checking to begin with. This is where strict discipline on credit card usage is a must. Credit cards make it too easy to spend when you run out of money.

This is why I recommend using cash throughout the month if you have issues with credit cards. Leave the cards at home when you go to the grocery store or shop online: How Frys Pickup (formally Click List) Saves Me Money

Image Credit: serezniy / iStock.

You need a vehicle account

After the money is deposited into checking, we move a portion into a vehicle fund. This fund is only for vehicle maintenance and for future vehicle purchases. I am anti-car payments so we save up and buy our cars with cash. Due to my wife and I driving older vehicles (one is 12 years old, the other is 13 years old), they periodically need repairs that can be a few hundred dollars. By contributing to this account each month, we have never needed to put a vehicle repair on a credit card.

Image Credit: RostislavSedlacek.

My vacation account is my favorite

The third savings account is our vacation fund. This is obviously our favorite fund and one we make sure we put money into each and every month! By having a set amount of money deposited into this savings account, we pay for our vacations with cash.

By doing it this way, we can enjoy our vacation and not feel the pain of credit card debt when we come home from vacation. We love our vacations so we make sure it is one of our top priorities to fund this savings account.

Image Credit: DepositPhotos.com.

Emergency savings & 6 months of expenses

Our fourth savings account is our emergency savings and six months of expenses fund. Luckily this savings account is fully funded so we no longer contribute to it. It sits there making little to no money in interest.

I’m all about investing money and it hurts to know that this account is worth 2%-3% less each year due to inflation. However, this is a savings account and not an investment. It is there to protect us against emergencies or unexpected major expenses. Insurance for life is a good way to think about it. Insurance costs you money – investments make you money. This savings account is my insurance.

Image Credit: designer491 / iStock.

‘Fun money’ accounts are only for fun!

The fifth and sixth savings accounts are also two of our favorites. Each month my wife and I get a certain amount of “fun money.” This is money that we can spend without feeling any guilt. If I want to use my money to go get beer and wings with my friends I can. If she wants to spend it on her hair and nails, she can with no questions asked.

We each need a certain amount of money to spend without feeling guilty. If you are in debt, you know how frustrating it can be to stick to a budget without any room for fun. It’s like a diet. If you have no cheat days, how many people are really going to stick to a diet for any amount of time? Give yourself some wiggle room to splurge a predetermined and budgeted amount on yourself. Even if it’s only $20 dollars a month!

Right now we are at the lowest number of accounts we have had in our marriage. Depending on what our goals are, we may have more accounts depending on what we are saving up for. This structure actually works very well and is not confusing once you get the hang of it. We have built up a routine of moving money on a monthly basis in order to set ourselves up for future success.

Image Credit: bernardbodo / iStock.

Increase your income to fund your accounts more quickly

I also rely heavily on my side hustle. I work a side job outside of my main employment to add more money to our goals. By doing this, we are able to fund our separate accounts faster. All of my side job money goes to the extra accounts and none of it is used for bills. If you get into the habit of overspending and using a side hustle to pay the bills, you are one injury away from defaulting on your loans. Avoid this slippery slope!

Image Credit: iStock.

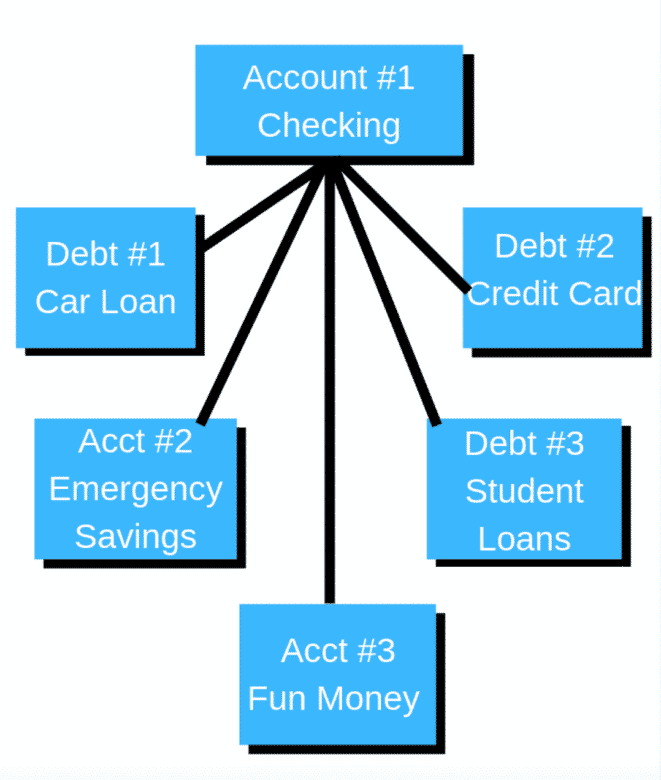

Restructure based on your situation

If you are in debt, your account structure may look a bit different. Here is an example of how your account and payment structure may look:

You may be wondering where the vacation fund went. Depending on the amount of debt you have and your future plans, you may need to go without a vacation for a year or two. Before you unsubscribe from all my emails and close my web page, hear me out.

Image Credit: Ryan Luke.

Bottom line

If you continue to spend money on vacations or other things that delay your debt payoff, you may never truly free yourself from debt. If you sacrifice a couple of years now to get out of debt, you will be able to take many more exciting and financially stress-free vacations in the future. Avoid punishing your future self by spending money you don’t have today.

If you need more help getting out of debt, please check out my related articles:

This article originally appeared on ArrestYourDebt.com and was syndicated by MediaFeed.org.

Image Credit: grki.

AlertMe