Real estate comes with some of the best tax advantages in the world. Landlord tax deductions include just about every conceivable expense associated with rental properties – plus some just-on-paper expenses.

But tax laws change fast, so investors need to stay on top of real estate tax deductions and other tax law changes. So, before you jump into the rental property deductions checklist, make sure you’re up to speed on how recent tax law changes affect landlords’ tax returns.

21 Tax Deductions for Landlords

Real estate investors can deduct the following 21 rental property expenses, to keep more of your money in your pocket where it belongs. It’s not 100% exhaustive, as there are a few obscure tax deductions that only apply to a few landlords, but think of this as a rental property deductions checklist for the average landlord.

IMPORTANT: These rental property tax deductions are “above the line” deductions, meaning they come directly off your taxable income for rental properties. That means you can deduct these expenses, and still take the standard deduction!

For help managing your investments, consider working with a fiduciary financial advisor. Find an advisor who serves your area today (Sponsored).

1. Losses from Theft or Casualty

The TCJA suspended the itemized deduction for personal casualty and theft losses for 2018 through 2025. Before 2018 deductions of this kind were permitted when they exceeded $100.

But landlords can still deduct losses from theft or damage to their rental properties, as business expenses.

2. Property Depreciation

Depreciation makes for a handy “paper expense.” Much of the cost of buying your property can be written off as a tax deduction, although it must be spread over 27.5 years (don’t ask me where that number came from). Buildings lose value as they age (at least theoretically), so the IRS lets you deduct 1/27.5th of the property’s cost each year.

Major property upgrades and “capital improvements” must be depreciated as well, rather than deducted in the year you make them. For example, a new roof is a capital improvement that must be depreciated, rather than deducted all at once.

But the patching of a roof leak? That’s a repair.

Read more about rental property depreciation before writing it off, and use our rental property depreciation calculator to make your life easier.

3. Repairs & Maintenance

Basic repairs and maintenance such as new paint and new carpets are deductible for your rental properties. That’s not the case for your primary residence, in which repairs are not deductible.

Remember, if it’s a large improvement or replacement (like the roof example), it may count as a “capital improvement,” in which case you’ll have to spread the deduction over multiple years, in the form of depreciation.

The line isn’t always crystal clear however, like the roof example above. Here’s an example of how it gets blurry: if you replace all your windows to modernize and improve your energy efficiency, it’s a capital improvement. If a baseball goes through one window, which you replace, it’s a repair. But what if you replaced a few windows last year, but not all?

Talk to an accountant, and build a defensible argument for any repairs you deduct.

4. Segmented Depreciation

Some improvements, such as landscaping and “personal property” inside the rental/investment property (e.g. refrigerators) can be depreciated faster than the building itself. It’s more paperwork, to segment the depreciation of certain improvements as separate from the building’s depreciation, but it means a lower tax bill right now, not in the far distant, unknowable future.

5. Utilities

Do you pay for gas, heating, trash removal, sewer or any other utility for your rental? Be sure to deduct these costs when you file your tax return.

Take heed however, these if your tenant reimburses you for a utility, that would be considered income. So you have to declare both the income and the expense, even though they offset each other.

6. Home Office

This is a popular deduction, but it’s also one you need to be careful about, as it can trigger audits. You have to set aside a percentage of your home for only doing work/business/real estate investing-related activities, and that percentage of your housing bill can be deducted. The IRS has put this deduction under the microscope in recent years, and 2022 may see this deduction scrutinized even more.

One recent downer: no more home office deduction for those who work for others in the comfort of their home. But as a real estate investor, you’re a business owner, so you can still claim it if you use the space “exclusively for business.”

Make sure and talk to an accountant about this, and keep the percentage realistic.

7. Real Estate-Related Travel

Another popular-but-dangerous deduction, you can deduct travel expenses if your travel was for your real estate investing business… and you can prove it. Many people get cute with this one, and when they go on vacation they’ll go see one or two “potential investment” properties and then write the entire trip off as a business expense.

Whenever you plan on deducting travel expenses, put together as much documentation as you possibly can so that you can make a strong case that it was an actual business trip. For example, meet with a real estate agent in the area, and keep all of your email correspondence with them. Keep all listing information and investment calculations for any properties you visit. Track your mileage for all driving done to and from rental properties.

C-Y-A!

8. Meals

This one’s dangerous too, but still legal.

Landlords and real estate investors can deduct 50% of meal costs while traveling to visit properties they already own. They cannot write off meals when scouting for prospective rental properties.

In your home market, defined as a 40-mile radius of where you live, you can deduct 50% of meal costs when meeting with other business contacts, such as partners, real estate agents, or contractors. Real estate investors cannot take a deduction for meals they eat alone in their home market.

As with the other rental property deductions on this list, always keep receipts and documentation, and always be prepared to defend all deductions if audited by the IRS!

9. Closing Costs

Many closing costs are tax deductible, and others can be depreciated over time as part of your acquisition cost. Use an accountant with a deep knowledge of real estate investments, and send them the settlement statement (previously called a HUD-1, now known as a CD or closing document) for each property you bought last year.

10. Property Management Fees

Paid a property manager to handle the headaches and field those dreaded 3 AM phone calls from tenants? You can write off their management fees, including monthly percentage fees, new tenant placement fees, and any other fees the manager slaps you with.

If you’re still on the fence about hiring one, here’s what you should know about whether to hire a property manager.

11. Rental Property Insurance & Rent Default Insurance

Like homeowner’s insurance for your primary residence, your landlord insurance premium for each property is also tax deductible.

You can also deduct the cost of rent default insurance policies for each property. Not familiar with rent default insurance? If the tenant stops paying the rent, the insurance company pays it until you go through the eviction process and sign a lease agreement with a new tenant. It protects you against tenants failing to pay rent, so you never go without rental cash flow.

They’re not very expensive either, usually ranging between $300-450 per year. Try Steady, we’ve vetted them as a reputable and easy insurance provider to work with.

12. Mortgage Interest

All interest you pay to your mortgage lender on rental property loans remains tax deductible. As mentioned above, it’s an “above the line” deduction that simply comes off of your taxable rental property income.

But for your primary residence, the IRS limits the deductibility of mortgage interest only up to $750,000 of home mortgage debt for tax year 2021.

13. Mortgage Insurance (PMI/MIP)

No one likes mortgage insurance (other than banks). But at least you can deduct the cost from your taxable rental property income.

Note that mortgage insurance only applies to conventional and FHA loans, not privately issued portfolio loans. If you borrowed your rental property loan through a private portfolio lender like Kiavi or LendingOne, you don’t have to worry about mortgage insurance.

While you’re at it, check to see if any of your mortgage balances have fallen below 80% of their respective property values. If so, you can apply to have PMI removed from the loan, and potentially save yourself hundreds of dollars per month.

The same goes for your home, not just your rental properties!

14. Accounting, Legal & Other Professional Fees

All professional fees associated with your rental properties are tax deductible. Bookkeeping, accounting, attorney, real estate agent and any other fees you pay out for professional services can be deducted from your taxable income. Don’t forget the cost of any bookkeeping or landlord software (ahem!) you use.

One wrinkle introduced by the TCJA however is that personal tax preparation expenses are no longer deductible since 2018. But business accounting – such as for your real estate LLC or S-corp – is still deductible as a rental business expense for landlords. Talk to your accountant about shifting as many of your tax preparation expenses as possible to the business side of the books!

15. Tenant Screening

If you paid for tenant credit reports, criminal background checks, identity verifications, eviction history reports, employment and income verification or housing history verification, those fees are deductible.

Even better, have the applicant pay directly for tenant screening report costs. Which, I might add, our landlord software allows you to do!

16. Legal Forms

Bought a state-specific lease agreement this year? Eviction notices? Property management contracts? The cost of legal forms is also deductible.

Although I have to add that we offer free tenant letters and state-specific eviction notices, so you don’t need to pay for them at all.

17. Property Taxes

Under the Tax Cuts and Jobs Act, landlords can still deduct rental property taxes as an expense.

But it’s a little more complicated for homeowners, and even though this is a list of landlord tax deductions, let’s take a moment to review the changes for homeowners, shall we?

For tax year 2021, you can no longer deduct for state and local taxes in excess of $10,000. These state taxes include things like: state and local income tax, sales taxes, personal property tax, and… homeowner property taxes.

What does this mean for high-tax states like New York, New Jersey or Connecticut? Well, it could mean that more people may relocate to lower-tax states like Florida, and may even spark lower property values in states such as New Jersey. Only time will tell.

18. Phones, Tablets, Computers, Phone Service, Internet

Bought a new phone this year? Maybe a new laptop or tablet? If you use it for work, you can probably persuade your accountant (and the IRS) that the costs should be deducted from your taxable income. Or, more likely depreciated, as most of these devices come with a lifespan that the IRS classifies in multiple years.

Likewise, for internet bills, phone service charges and the like, with the caveat that you need to be able to document that it was for business purposes. Printer toner, computer paper, pens, and the like; keep those receipts.

19. Rental Property Licensing & Registration Fees

Licensing and registration fees are sometimes a local requirement for rental properties. For instance, in the city of Philadelphia, a rental license fee is required along with an inspection of the property.

So, if you’ve had to purchase or renew a landlord or rental license for the property, that cost is deductible.

Furthermore, some localities will require a vacation rental license for short term rentals such as seasonal, AirBnB and the like. These licensing costs are deductible as well.

20. Occupancy Tax

There are states that assess an occupancy tax on collected rental amounts, comparable to paying sales tax. You see this more often in states where short-term rentals are common. Florida, Arizona and New Jersey are examples of states that charge an occupancy or tourist tax.

If you own rental property in an area that charges an occupancy-like tax, then the amount is tax deductible. Remember, however, that the tax will not only differ from state to state but also from local jurisdictions like cities and counties.

21. Business Entity Pass-Through Deduction

The TCJA made significant changes to how legal entities (e.g. LLCs) and pass-throughs are treated. Sole Proprietorship, Partnership, and Corporate Entities are now entitled to a “pass-through” deduction as long as the rental activities meet the requirements for business tax purposes.

The short version is that landlords can deduct 20% of their rental business income from their taxable business income amount. For example, if you own a rental property that netted you $10,000 last year, the pass-through deduction reduces your taxable rental business income from $10,000 to $8,000. Pretty sweet, eh?

There are restrictions, of course. The deduction phases out for single tax payers with adjusted gross incomes over $163,300, and married taxpayers earning over $326,600. Although under some conditions, higher-earning landlords can still take advantage of the pass-through deduction – definitely discuss with your accountant.

One more reason, beyond asset protection, to own rental properties under a legal entity!

We’ve said it before and we’ll say it again: talk to an accountant before taking this deduction. It gets complicated quickly, and you don’t want to end up in boiling water with the IRS.

Regular Income Tax Rates

From 2018 through 2025, rental property investors will benefit from generally lower income tax rates and other favorable changes to the tax brackets. The TCJA retains seven tax rate brackets, although six of the brackets’ rates are lower than before.

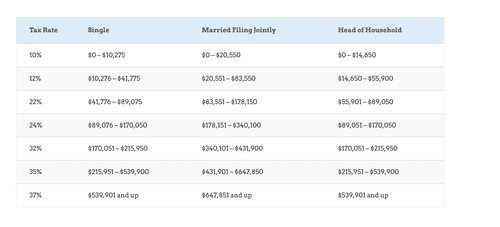

2022 Income Tax Rates

Here are the updated regular income rates for tax year 2022 (due in April 2023 or October 2023 with an extension):

Keep in mind that you pay separate tax rates for each “segment” of income. For example, a single taxpayer with an adjusted gross income of $50,000 would pay the following taxes:

$1,027.50 on their first $10,275 of income (10%)

$3,779.88 on the next $31,499 of income (12%)

$1,809.28 on the next $8,224 of income (22%)

Total Taxes: $6,616.66 Effective Tax Rate: 13.23%

2023 Income Tax Rates

For tax year 2023 (taxes due in April 2024), the regular income tax brackets shifted upward as follows:

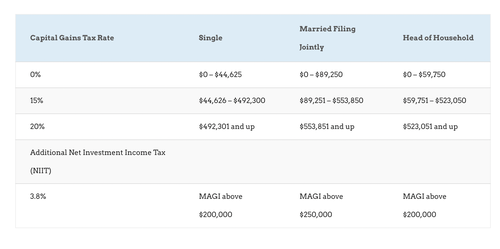

Long-Term Capital Gains Tax Brackets

The TCJA retains the existing tax rates for long-term capital gains.

Remember, short-term capital gains – earnings on investments held for less than one year, such as flipped homes – are taxed as regular income. But the IRS charges less for long-term capital gains: earnings from investments held for at least one year.

Roughly speaking, taxpayers pay 0% on long-term capital gains if their income falls in the 10% or 12% income tax brackets. If they earn enough to pay taxes at the 22% tax rate, they have to start paying taxes on long-term capital gains.

2022 Capital Gains Tax Rates

Here’s how the tax brackets look for long-term capital gains for tax year 2022 (due in April 2023):

2023 Capital Gains Tax Rates

For tax year 2023 (taxes due in April 2024), the capital gains tax brackets bump up:

The 2023 tax brackets jumped more than usual, given the high inflation rate during 2022.

TCJA Changes to the Home Mortgage Deduction

The changes in the Tax Cuts and Jobs Act of 2017 (TCJA) impacted homeowners, real estate investors and landlords alike. Here’s an outline of what you need to know as a real estate owner, and when in doubt, hire a professional who knows accounting with a real estate investing focus. Ideally one who invests in real estate themselves.

Home mortgage interest remains deductible up to $1,000,000, for loans that settled before December 15, 2017.

Home mortgage debt incurred after December 15, 2017 is only deductible up to $750,000. Mortgage interest on rental property loans is unaffected by the TCJA.

Another change worth mentioning is the tax deduction is no longer available on HELOC’s (Home Equity Line Of Credit) since tax year 2019.

Keep in mind that interest on HELOCs for rental properties remains deductible for landlords.

No Self-Employment Taxes for Landlords

In many ways, landlords get the best of both worlds: the tax benefits of owning a business, without the downside of self-employment taxes.

Real estate flippers can sometimes fall under the “dealer” category, and find themselves subject to double FICA taxes. FICA taxes fund Social Security and Medicare, and cost both employees and employers 7.65% of all income paid. Self-employed people end up having to pay both sides of FICA taxes, at 15.3% of total income. If you haven’t done so already, consider using a tax calculator to make sure everything is accurate.

But the Tax Cuts and Jobs Act of 2017 ended up leaving landlords and their rental income free from any FICA taxes.

Passive Income Loss Rule

If you have losses from “passive activities” such as owning rental properties, typically you can only deduct those losses to offset other passive income sources, such as other rental properties. For example, if you earn $10,000 from one rental property and have an $8,000 loss on another, you can offset your $10,000 income with the $8,000 loss, for a net taxable rental income of $2,000.

But if you have a net loss, that can’t be used as a deduction against your active income from your 9-5 job. You can carry it forward however, to offset future passive income earnings and rents.

Here’s how the TCJA changes matters: there’s a new $250,000 cap for single filers, $500,000 cap for married filers, for passive losses. Any passive losses that you’re allowed, in excess of those caps, must be carried forward to the next tax year.

It won’t affect most landlords, but it’s something to be aware of.

Final Word

It’s hard to get ahead if 50% of your income is going to taxes (which it probably is, if you add up everything you pay in sales tax, property tax, federal income tax, state income tax, local income tax and FICA taxes). But by being savvier with your documentation and deductions, landlords and real estate investors can pay less in taxes than other people, and truly realize the advantages of entrepreneurship.

Remember to always document every expense you plan to deduct. That means keeping receipts, invoices and bills throughout the year as expenses pop up; to help with this, keep a separate checking account for your real estate expenses if you don’t already. Never swipe that debit card or write a check from that account without first getting documentation!

We will continue updating and expanding this article content as the upcoming tax changes continue. (If you want to be notified of future webinars by email, sign up for our mailing list – you even get access to our free mini-course on buying 2-4 multifamily rentals!)

Feel free to pass this rental property deductions checklist on to other landlords, to make sure they’re taking advantage of all tax deductions available for landlords!

More from MediaFeed:

- 11 ways that millionaires think differently than the rest of us

- Foods that Americans really loathe

- Unsettling facts about retirement in America

- The most crime-ridden cities in the US

Like MediaFeed’s content? Be sure to follow us.

More investing tips

You can start investing at any age and with nearly any budget. Just be sure to keep your risk tolerance in mind, especially when the market is volatile.

Additionally, a financial advisor can help you with your investment portfolio. SmartAsset’s free tool matches you with up to three financial advisors who serve your area, and you can interview your advisor matches at no cost to decide which one is right for you. (Sponsored)

This article originally appeared on SparkRental.com and was syndicated by MediaFeed.org.

What are the different types of taxes?

Whether you’re a newbie in the workforce or a seasoned retiree looking to do some estate planning, taxes can be complicated. With terms like “tax brackets” and “deductions,” or the differences between income vs. payroll taxes and short-term vs. long-term capital gains, you’re joining hundreds of millions of Americans who have had to figure out the confusing world of the U.S. tax code.

At a high level, taxes are involuntary fees imposed on individuals or corporations by a government entity. The collected fees are used to fund a range of government activities, including but not limited to schools, maintaining roads, health programs, as well as defense measures.

DepositPhotos.com

For individuals, taxes can have a profound effect on your life, influencing decisions on marriage, employment, buying a home, investing, healthcare, charity, retiring and leaving a will. Therefore, even if you have a smart accountant, it’s important to get up to speed on the tax code.

Helloquence

Here’s an incomplete but detailed look at the different types of taxes that can be levied and the ways in which they’re typically calculated and imposed.

franckreporter

The federal government collects income tax from people and businesses, based upon the amount of money that was earned during a particular year. There can also be other income taxes levied, such as state or local ones. Specifics of how to calculate this type of tax can change as tax laws do.

In the U.S, about 200 million Americans file tax forms with the Internal Revenue Service by April 15 each year. The amount of income tax owed will depend upon the person’s tax bracket and it will typically go up as a person’s income does. That’s because, in the U.S., there is a progressive tax system for federal income tax, meaning individuals who earn more are taxed more.

There are currently seven different federal tax brackets. To find out what bracket applies, a taxpayer can look at the current IRS 2021 tax bracket chart. The amount owed will also depend on filing categories like single; head of household; married, filing jointly; and married, filing separately.

Deductions and credits can help to lower the amount of income tax owed. And if a federal or state government charges you more than you actually owed, you’ll receive a tax refund.

DepositPhotos.com

Property taxes are charged by local governments and they are one of the costs associated with owning a home.

The amount owed varies by location and is calculated as a percentage of a property’s value. The funds typically help to fund the local government, as well as public schools, libraries, public works, parks and so forth.

Property taxes are considered to be an ad valorem tax because they are based on the assessed value of the property.

In fact, property taxes are the most common type of an ad valorem tax. Another ad valorem application is the import duty tax where the amount due is based on the value of goods being imported from another country.

DepositPhotos.com

Employers withhold a percentage of money from employees’ pay and then forward those funds to the government. The amount being withheld will vary, based on a particular employee’s wages, with federal payroll taxes being used to fund Medicare and Social Security.

There are limits on the portion of income that would be taxed. For example, in 2020, a person’s income that exceeds $137,700 is not subject to Social Security tax.

Because this tax is applied uniformly, rather than based on income throughout the system, payroll taxes are considered to be a regressive tax.

DepositPhotos.com

These are actually two different types of taxes. The first — the inheritance tax — can apply in certain states when someone inherits money or property from a deceased person’s estate. The beneficiary would be responsible for paying this tax if they live in one of several different states where this tax exists AND the inheritance is large enough.

The federal government does not have an inheritance tax. Instead, there is a federal estate tax that is calculated on the deceased person’s money and property and it’s paid out from the assets of the deceased before anything is distributed to their beneficiaries.

There can be exemptions to these taxes and, in general, people who inherit from someone they aren’t related to can anticipate higher rates of tax.

DepositPhotos.com

These are the three main categories of tax structures in the U.S. (two of which have already been referenced in this post).

Here are definitions that include how they impact people with varying levels of income.

DepositPhotos.com

Because this tax is uniformly applied, regardless of income, it takes a bigger percentage from people who earn less and a smaller percentage from people who earn more.

As a high-level example, a $500 tax would be 1% of someone’s income if they earned $50,000; it would only be half of one percent if someone earned $100,000, and so on. Examples of regressive taxes include state sales taxes and user fees.

alfexe

This kind of tax works differently, with people who are earning more money having a higher rate of taxation. In other words, this tax (such as an income tax) is based on income.

This system is designed to allow people who have a lower income to have enough money for cost of living expenses.

Depositphotos

This is another way of saying “flat tax.” No matter what someone’s income might be, they would pay the same proportion. This is a form of a regressive tax and proportional taxes are more common at the state level and less common at the federal level.

DepositPhotos.com

Next up: capital gains tax that an investor may be responsible for paying when having stocks in an investment portfolio. This can happen, for example, if they sell a stock that has appreciated in value over the purchase price.

The difference in the increased value from purchase to sale is called “capital gains” and, typically, there would be a capital gains tax levied.

An exception can be when an investor sells increased-in-value stocks through a tax-deferred retirement investment inside of the account. Meanwhile, dividends are taxed as income, not as capital gains.

It’s also important for investors to know the difference between short-term and long-term capital gains taxes. In the U.S. tax code, short-term is one year or less, while long-term is anything longer. In 2020, the federal tax rate on gains made by short-term investments ranged from 10% to 37%.

For long-term investment gains, it was significantly lower at either 0%, 15% or 20%.

Jirapong Manustrong / istockphoto

Tips for tax efficient investing can include to select certain investment vehicles, such as:

- Exchange-traded funds (ETFs): These are baskets of securities that trade like a stock. They’re tax efficient because they typically track an underlying index, meaning that while they allow investors to have broad exposure, individual securities are bought and sold less frequently, creating fewer events that will likely result in capital gains taxes.

- Index mutual funds: These tend to be more tax efficient than actively managed funds for reasons similar to ETFs.

- Treasury bonds: There are no state income taxes levied on earned interest.

- Municipal bonds: Interest, in general, is exempted from federal taxes; if the investor lives within the municipality where these local government bonds are issued, they can typically be exempt from state and local taxes, as well.

fizkes/istockphoto

In the U.S., we pay a regressive form of tax, a sales tax, on many items that are purchased. In Europe, the system works differently. A VAT tax is a form of consumption tax that’s due upon a purchase, calculated on the difference between the sales price and what it cost to create that product or service. In other words, it’s based on the item’s added value.

Here’s one big difference between a sales tax and a VAT tax: the first is charged at the final part of the sales transaction. VAT, on the other hand, is calculated throughout each supply chain step and then built into the final purchase price.

This leads to another difference. Sales taxes are added onto the purchase price that’s listed; VAT contains those fees within the price and so nothing extra is added onto the price tag that a buyer would see.

DepositPhotos.com

This isn’t a comprehensive list of all tax types but hopefully it provides a broad answer to questions like “What is a tax?” and “What types of taxes are there?” And hopefully it demystifies some questions you might have had about all the different tax items on a receipt or paystub.

Learn more:

This article

originally appeared on SoFi.com

https://www.sofi.com/learn/content/types-of-taxes/

and was

syndicated by MediaFeed.org.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

SoFi Money

SoFi Money is a cash management account, which is a brokerage product, offered by SoFi Securities LLC, member FINRA / SIPC . Neither SoFi nor its affiliates is a bank. SoFi has partnered with Allpoint to provide consumers with ATM access at any of the 55,000+ ATMs within the Allpoint network. Consumers will not be charged a fee when using an in-network ATM, however, third party fees incurred when using out-of-network ATMs are not subject to reimbursement. SoFi’s ATM policies are subject to change at our discretion at any time.

External Websites: The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

SoFi Invest

The information provided is not meant to provide investment or financial advice. Investment decisions should be based on an individual’s specific financial needs, goals and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA / SIPC . SoFi Invest refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below.

1) Automated Investing—The Automated Investing platform is owned by SoFi Wealth LLC, an SEC Registered Investment Advisor (“Sofi Wealth“). Brokerage services are provided to SoFi Wealth LLC by SoFi Securities LLC, an affiliated SEC registered broker dealer and member FINRA/SIPC, (“Sofi Securities).

2) Active Investing—The Active Investing platform is owned by SoFi Securities LLC. Clearing and custody of all securities are provided by APEX Clearing Corporation.

3) Cryptocurrency is offered by SoFi Digital Assets, LLC, a FinCEN registered Money Service Business.

For additional disclosures related to the SoFi Invest platforms described above, including state licensure of Sofi Digital Assets, LLC, please visit www.sofi.com/legal. Neither the Investment Advisor Representatives of SoFi Wealth, nor the Registered Representatives of SoFi Securities are compensated for the sale of any product or service sold through any SoFi Invest platform. Information related to lending products contained herein should not be construed as an offer or pre-qualification for any loan product offered by SoFi Lending Corp and/or its affiliates.

DepositPhotos.com

Featured Image Credit: SeventyFour/ iStock.

AlertMe