Has your business reached the point where you’re ready to hire more employees or expand into new customer markets? As your business becomes more complex, it may be time to revisit whether accrual accounting will be more effective for your financial and tax reporting.

In this post, we’ll go over what you need to know about the accrual method of accounting, including its benefits, how it compares to cash accounting, and if it’s right for your business.

The differences between cash vs. accrual accounting

Though people commonly confuse accrual accounting with cash accounting, there are some stark differences to know before choosing which is right for your business.

Accrual-based accounting is a popular method for big companies, as it uses the double-entry accounting method, which is more accurate and conforms with the generally accepted accounting principles (GAAP).

In accrual accounting, you record income and expenses as you earn or incur them. This means you add income to your accounting journal when you complete a service or deliver goods and expenses when you receive an invoice for the goods and services.

Cash accounting, on the other hand, records income and expenses when you receive or deliver payment for goods and services. Most small businesses prefer the cash method because it’s simpler.

Here’s how they work: Let’s say your business provided a service to a customer in June, but they’ll only pay you in July. With accrual accounting, you’d record income for June, which is when you performed the service. But with cash accounting, you’d record income in July, when you received the payment.

Most businesses can choose between cash and accrual accounting methods. However, if an inventory is necessary to account for your income or your company’s income is over $25 million, the IRS will require you to use the accrual method.

How accrual accounting works for different adjusting entries

When using accrual accounting, you’ll have different adjusting entries to add to the balance sheet and income statement.

These entries divide into two categories:

- Accruals: Revenue and expenses you haven’t yet received or paid, but you already provided the good or service.

- Deferrals: Revenue and expenses you received or paid before providing or receiving the goods and services.

Let’s take a look at these types of adjusting entries and how you can use them in accrual accounting.

Accrued revenue

Accrued revenue is any income you expect to receive for any good or service you provided. It essentially means a customer owes you money for the transaction.

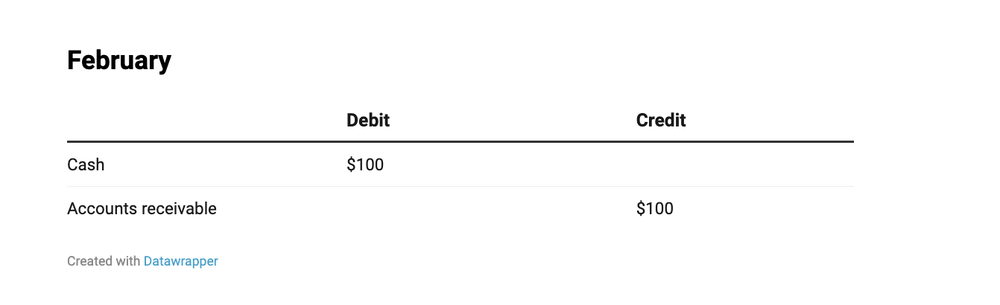

For example, if you provided a consulting service for $100 in January but you expect the customer to pay in February, you’ll have an accrued revenue of $100 in January.

In this case, you’d debit your accounts receivable and credit revenue. Here’s how you’d record this in January:

Then, in February, when you receive the payment, you’ll credit accounts receivable, which means receivables go down, and debits cash, which will go up.

Deferred revenue

Differently than accrued revenue, deferred revenues happen when a customer has paid for a good or service you haven’t yet provided. Meaning you owe the customer what they paid for.

This is common when customers pay for a subscription or have recurring payments, like a phone bill. For example, let’s say a customer paid $100 for your consulting services in January, but you’ll only be providing the service in February.

In this case, you would debit your cash account since it increased, and you’d credit your deferred revenue, which is a liability account.When you provide the consulting service in February, you’ll debit your deferred revenue, decreasing your liability. Then, you’ll credit revenue.

Accrued expenses

Accrued expenses are similar to accrued revenues in the sense that you were recording when the transaction happened, and not when there’s a payment. But in this case, your business is the one that has to pay.

This happens when you receive a good or service, but the provider expects you to pay at a later date. For example, let’s say you received merchandise for your business in March and received an invoice of $500 with payment due in April.

In accrual accounting, you’d record when you received the merchandise. In March, you’d debit $500 for expenses and credit accounts payable since you still have to pay for it. Once you pay for the merchandise in April, you’ll debit accounts payable and credit cash.

Prepaid expenses

Prepaid expenses are the opposite of accrued expenses. This means you already paid for the goods or services that you’re yet to receive. In this case, someone still owes you the goods and services you paid for.

For example, if you paid $500 for merchandise from your supplier in March, but they’ll only deliver them in April, you’ll have to debit the prepaid expense account and credit your cash account. After you receive the merchandise in April, you’ll debit your expense account and credit prepaid expense.

Advantages of accrual accounting

Recording cash transactions based on when you complete services, deliver products, and incur expenses is also beneficial to your business.

Here are the main advantages typically associated with accrual accounting.

- Provides a more accurate view of your business’s performance: Since you can measure profitability and business activity during a specific month or year.

- Makes it easier to track revenue if you sell on credit: Since you record the transactions when they happen instead of after payment.

- Can defer your tax liability: Since you can delay paying taxes on a certain income if a customer pays the year after it was delivered.

Still, it’s important to review the IRS guidelines on how to report an advance payment for services using the accrual accounting method.

Disadvantages of accrual accounting

Whereas accrual accounting’s strengths lie in accurately showing business profitability and representing long-term revenues and expenses, it has a few drawbacks as well.

Here are some pitfalls of accrual accounting:

- Does a poor job of tracking cash flows: Since your bank account may show a smaller balance than your income statement if customers haven’t paid what they owe you.

- Requires more bookkeeping and staff resources: Since you need to track cash flow separately to cover your bills which can be more complicated and expensive to implement.

Due to the added complexity and paperwork required under the accrual method of accounting, small business owners—particularly when starting a business—tend to view it as a less ideal option than the cash accounting method.

Streamline your accounting and save time

Accrual accounting provides a better picture of your overall financial position, and many companies consider it to be the standard and more accurate accounting method. But it can also be too complicated and expensive for small business owners.

One way to offset the people and time resources required under accrual accounting is to invest in accounting software that does the hard work for you.

This article originally appeared on the QuickBooks Resource Center and was syndicated by MediaFeed.org.

More from MediaFeed:

18 loans for Hispanic-owned businesses

There are nearly 5 million Hispanic-owned businesses in the U.S., making this the fastest-growing segment of U.S. small businesses, according to the U.S. Small Business Administration (SBA). Yet, despite these big numbers, Hispanic and Latinx business owners frequently face challenges accessing capital and, as a result, often can’t successfully scale their businesses.

Fortunately, a number of organizations and government agencies in the U.S. are stepping up to address this unmet need, offering loans, grants, and other financing options to Hispanic and other minority entrepreneurs. These minority business loans may have lower interest rates and be easier to qualify for than some traditional loans. Here are 18 financing options that are worth checking out.

(Learn more: Personal Loan Calculator)

PeopleImages/istockphoto

To qualify as a Hispanic-owned business, more than 50% of the company must be owned by people of Mexican, Puerto Rican, Cuban, or other Hispanic origin. Currently, nearly one in four businesses are Hispanic-owned.

andresr/istockphoto

A minority business loan is a small business loan designed to provide financing options for underserved communities. While minorities are free to apply for any business loan, minority business loans may offer more competitive rates and have less stringent qualification requirements.

Groups that are considered minorities in the U.S. include African Americans, Asian Americans, Hispanic Americans, and Native Americans. Women are also considered minorities for many types of loans, as well.

FreshSplash/istockphoto

The following lenders offer different types of small business loans to Hispanic and minority entrepreneurs and were chosen based on our analysis of search volume.

1. Accion

Accion is a nonprofit financial institution that invests in underserved communities and offers low-cost lending opportunities to Hispanic- and minority-owned businesses. The Accion Opportunity Fund provides loan amounts from $5,000 to $100,000, and is quick and easy to apply for online.

Accion offers two types of small business loans — the Southern Opportunity and Resilience (SOAR) Fund and the Small Business Progress Loan. SOAR is geared toward those in the south and southeast who experienced economic hardship from the COVID-19 pandemic and have been in business since September 2019 or earlier. The Small Business Progress Loan, on the other hand, is open to all minority-owned businesses and women entrepreneurs, and is partnered with American Express.

Accion also offers online resources, events, and networking opportunities (in Spanish and English) to help minority business owners learn and grow their companies.

(Learn more at: Home Affordability Calculator)

Delmaine Donson/istockphoto

The Community Development Financial Institutions Fund (CDFI Fund), which is part of the U.S. Treasury, gives funds to companies and organizations that help underserved people and communities. Minority business owners can reach out to local banks and nonprofit groups that have received CDFI funds to discuss and apply for low-cost business loans.

JohnnyGreig/istockphoto

The owners of Camino Financial were inspired to start their lending business in order to help people like their mother, who lost her Mexican restaurant business when they were children. To that end, they offer simple and affordable loans to small businesses who find it difficult to borrow through banks. They offer bad credit loans, secured and unsecured loans, microloans, and working capital loans up to $35,000. To qualify, your business must have been in operation for at least nine months and generate annual sales of $30,000 or $2,500 a month.

monkeybusinessimages/istockphoto

The U.S. Small Business Administration (SBA) offers several financing programs that can help minority-owned businesses get access to the funding they need. Here are two programs you may want to check out to find a Hispanic small business loan:

Microloans

The SBA microloan program is administered by an intermediary network of nonprofit community-based lenders, rather than traditional banks. Through these lenders, the SBA aims to reach lower-income communities and minority-owned businesses that are often overlooked by traditional lenders. These loans come with low interest rates, six-year terms. and loan amounts up to $50,000.

Community Advantage Loans

The SBA’s Community Advantage loan program provides up to $350,000 in capital and is specifically designed to meet the needs of business owners in underserved communities. To qualify for an SBA community advantage loan, business owners need to have good credit and a strong business plan. However, the business’s balance sheet and amount of collateral will not affect eligibility.

mapodile/istockphoto

By offering crowdfunded loans with 0% interest, nonprofit Kiva is working to lift barriers to capital often faced by entrepreneurs from underserved communities. To apply, you need to market your Hispanic business to the community of 1.9 million individual lenders. These lenders can then choose to lend your company as much as $15,000 and you’ll have up to three years to repay them.

PeopleImages/istockphoto

CDC Small Business Finance is a nonprofit whose mission is to provide access to affordable and responsible capital to underserved entrepreneurs, including minority, veteran, and hispanic business owners. CDC offers loan amounts of $20,000 to $350,000 with five- to 10-year terms. They also offer SBA 504 commercial real estate loans of $250,000 to $40 million.If you are looking for advice to rebuild your credit, develop your business strategy, or manage financial reports, you’ll appreciate having access to small business advisors through CDC.

AaronAmat/istockphoto

Grameen America strives to achieve racial and gender equity by providing microloans of up to $2,000 to female and minority business owners. As part of their program, borrowers can open free savings accounts with commercial banks and build personal credit as they pay off their microloans. Grameen also offers training and support to women who want to start businesses and rise out of poverty.

ferrantraite/istockphoto

The Latino Economic Development Center (LEDC) offers Hispanic small business loans of $500 to $250,000 that can be used to purchase equipment, expand a business, hire staff, or purchase inventory. The three types of loans offered by the LEDC are as follows:

- LEDC Growth Loan: Loan amounts up to $250,000 for established small businesses that have been in operation for a minimum of two years.

- LEDC Startup Loan: Loan amounts up to $20,000 for new businesses with less than two years of business history.

- LEDC Seed Loan: Loan amounts up to $5,000 for businesses with less than one year of experience and with plans to launch a company within three months of funding.

LEDC also offers free business advice and credit-building services, as well as a directory of latino-owned small businesses.

svetikd/istockphoto

The National Association of Latino and Community Asset Builders (NALCAB) provides funding to a network of over 200 nonprofit organizations that serve diverse Latino communities throughout the U.S. With NALCAB support, these partner organizations offer Hispanic loans, grants, professional training, and support.

FG Trade/istockphoto

Hispanic small business loans aren’t the only way for your business to get funding. There are also minority business grants that can provide capital that you don’t have to repay. These grants are offered by federal and local government agencies, corporations, and nonprofits.

10. Grants.gov

Grants.gov is the largest database of federal grant opportunities. While most grants are not specifically targeted to Hispanic small business owners, awards are available for all types of entrepreneurs, especially those focused on healthcare, U.S. defense, and environmental protection.

Drazen_/istockphoto

digitalundivided’s BREAKTHROUGH Program (powered by JPMorgan Chase’s Advancing Black Pathways) offers $5,000 grants to Black and Hispanic women in the Dallas, Texas area. digitalundivided also provides training and resources to help businesses understand their customers, find financing, and choose the right business model.

alvarez/istockphoto

The National Association of the Self-Employed (NASE) works to provide resources for all self-employed individuals, including Hispanic business owners. They offer Growth Grants of $4,000, which can be used for a variety of business expenses, including marketing, advertising, hiring employees, and expanding facilities.

Besides access to grants, becoming a NASE member allows you to connect with experts who can advise you on subjects like finance, healthcare, strategy, law, and marketing. NASE membership also gives you access to discounts on healthcare, software, tax filing, and business travel.

PeopleImages/istockphoto

Hispanic businesses located in rural areas that have fewer than 50 employees and less than $1 million in gross revenue may want to consider applying for a Rural Development Grant from the USDA. Grants vary in size and can be used for a variety of projects that aid business development in rural areas, including training, technical assistance, acquisition or development of land, building construction or renovations, equipment purchases, and pollution control.

supersizer/istockphoto

The Small Business Innovation Research (SBIR) and Small Business Technology Transfer (STTR) programs are government grants from five different federal government agencies. These competitive grants are focused around tech and science and offer up to $1 million in capital (divided into two phases) to qualified small businesses.

Tempura/istockphoto

You may be able to find funding for your Hispanic small business through Candid.org’s Foundation Directory Online, which contains information on over 240,000 grantmakers in the U.S. Access to the directory requires buying a monthly subscription, but you can cancel at any time.

monkeybusinessimages/istockphoto

Comcast RISE, which stands for Representation, Investment, Strength, and Empowerment, is a grant designed for businesses that were hit hardest by COVID-19. The grant is worth $5,000 and is given to small business owners hoping to expand and recover from the effects of the pandemic. Awards go to those looking to uplift their communities with a focus on diversity, inclusion, and community investment.

Vergani_Fotografia/istockphoto

The Entrepreneurial Spirit Fund by SIA Scotch Whiskey awards $10,000 in grants to small businesses owned by people of color in the food and beverage industry. Created by Hispanic entrepreneur Carin Luna-Ostaseskis, one of SIA’s goals is to provide funding, mentorship, and community to small businesses.

monkeybusinessimages/istockphoto

If you’re a woman entrepreneur, consider applying for the Amber Grant, named after Amber Wigdahl, who passed at the age of 19 and never got to fulfill her business dreams. Each month, at least $30,000 is given in Amber Grant money. Applying takes just a few minutes and winners are announced by the 23rd of the following month.

andreswd/istockphoto

In addition to the grants and loans, there are organizations that can provide technical assistance, training, workshops, and networking opportunities to Hispanic businesses. Below are some you may want to check out.

digitalundivided

With a focus on assisting Black female and Latinx business owners, digitalundivided offers virtual training and a fellowship program for entrepreneurs. It also offers a pre-accelerator program for tech-enabled startup founders who have already begun to build their startup, are pre-revenue, and need assistance in developing their business model, marketing, and strategy.

Minority Business Development Agency

The Minority Business Development Agency is an advocate for Hispanic and other minority-owned businesses, and offers research, conferences, and resources to help entrepreneurs. Its Enterprising Women of Color Initiative is aimed to help minority women succeed in business through various offerings.

USHCC

The United States Hispanic Chamber of Commerce actively promotes the economic growth, development, and interests of Hispanic-owned businesses. Members have access to events and business resources to support them in their growth. In addition, members get listed in the Chamber’s online Hispanic business directory.

SCORE

SCORE is a national organization that connects business owners to free mentors to help them learn and grow their companies. SCORE also offers free workshops and a robust online database of useful business content.

Poike/istockphoto

Looking for — and applying for — a Hispanic business loan can feel like an overwhelming task. Here are some ways to simplify the process.

Consider Your Options

Before applying for a small business loan, it’s a good idea to take a look at your credit profile and business financials, as this will give you an idea of what type of loan you might qualify for. If you have excellent credit, solid revenue, and have been in business at least two years, you may be able to qualify for a long-term, low interest loan from a bank or SBA lender. If not, you may want to look into financing offered by lenders and grantmakers listed above, as well as online lenders (who often have less strict qualification requirements for loans).

Determine How Much Money You Need

To figure out how much of a loan you need to start or grow your Hispanic business, consider how you would like to use the funds from a loan, then create a detailed budget for your project, adding in some padding to account for unexpected expenses.

Consider the Best Location for Your Business

If you haven’t yet launched your business, consider what might be the best environment for doing so. You may want to explore the best metros for minority businesses, since they may have established communities of hispanic business owners and resources to help you.

Gather All Your Paperwork

Whatever type of funding you decide to pursue, you will likely need to supply an extensive amount of information about your business in order to apply. This often includes:

- Business EIN

- Industry

- Entity type

- Business license and permits

- Annual business revenue and profit

- Bank account statements (personal and business)

- Personal and business tax returns

- Balance sheet

- Proof of collateral

- Accounts receivable and payable reports

- Existing debt

- Commercial lease

- Purpose of the loan/grant

- Business plan

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Lantern By

SoFiSoFi receives compensation in the event you obtain a loan, financial product, or service through the Lantern marketplace. This Lantern website is owned by SoFi Lending Corp., a lender licensed by the Department of Financial Protection and Innovation under the California Financing Law, license number 6054612; NMLS number 1121636. (nmlsconsumeraccess.org

https://www.nmlsconsumeraccess.org/

). This site is NOT owned and operated by SoFi Bank. Loans, financial products, and services may not be available in all states.

All rates, fees, and terms are presented without guarantee and are subject to change pursuant to each provider’s discretion. There is no guarantee you will be approved or qualify for the advertised rates, fees, or terms presented. The actual terms you may receive depends on the things like benefits requested, your credit score, usage, history and other factors.

*Check your rate: To check the rates and terms you may qualify for, Lantern and/or its network lenders conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, the lender(s) you choose will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

All loan terms, including interest rate, and Annual Percentage Rate (APR), and monthly payments shown on this website are from lenders and are estimates based upon the limited information you provided and are for information purposes only. Estimated APR includes all applicable fees as required under the Truth in Lending Act. The actual loan terms you receive, including APR, will depend on the lender you select, their underwriting criteria, and your personal financial factors. The loan terms and rates presented are provided by the lenders and not by SoFi Lending Corp. or Lantern. Please review each lender’s Terms and Conditions for additional details.

Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website on credit (consumer.ftc.gov)

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.¹

SoFi’s Insights tool offers users the ability to connect both SoFi accounts and external accounts using Plaid, Inc.’s service. When you use the service to connect an account, you authorize SoFi to obtain account information from any external accounts as set forth in SoFi’s Terms of Use. SoFi assumes no responsibility for the timeliness, accuracy, deletion, non-delivery or failure to store any user data, loss of user data, communications, or personalization settings. You shall confirm the accuracy of Plaid data through sources independent of SoFi. The credit score provided to you is a VantageScore® based on TransUnion® (the “Processing Agent”) data.

Personal Loan

SoFi Lending Corp. (“SoFi”) operates this Personal Loan product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders/partners receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.Personal loan offers provided to customers on Lantern do not exceed 35.99% APR. An example of total amount paid on a personal loan of $10,000 for a term of 36 months at a rate of 10% would be equivalent to $11,616.12 over the 36 month life of the loan.

Student Loan RefinanceSoFi Lending Corp. (“SoFi”) operates this Student Loan Refinance product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

NOTICE: The debt ceiling legislation passed on June 2, 2023, codifies into law that federal student loan borrowers will be reentering repayment. The US Department of Education or your student loan servicer, or lender if you have FFEL loans, will notify you directly when your payments will resume For more information, please go to https://docs.house.gov/billsthisweek/20230529/BILLS-118hrPIH-fiscalresponsibility.pdf https://studentaid.gov/announcements-events/covid-19

If you are a federal student loan borrower considering refinancing, you should take into account the new income-driven payment plan, SAVE, which replaces REPAYE, seeks to make monthly payments more affordable, and offers forgiveness of balances that were originally $12,000 or lower after 120 payments, among other improvements. Also, please note that once you refinance federal student loans you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as SAVE, or extended repayment plans.

Auto Loan RefinanceAutomobile refinancing loan information presented on this Lantern website is from Caribou, AUTOPAY, Engine by MoneyLion, and each of Engine’s partners (along with their affiliated companies). Caribou, AUTOPAY, and Engine by MoneyLion pay SoFi compensation for marketing their products and services on the Lantern site.

Auto loan refinance information presented on this Lantern site is indicative and subject to you fulfilling the lender’s requirements, including but not limited to: credit standards, loan size, vehicle condition, and odometer reading. Loan rates and terms as presented on this Lantern site are subject to change when you reach the lender and may depend on your creditworthiness, consult with the lender for more details. Additional terms and conditions may apply and all terms may vary by your state of residence.

Secured Lending DisclosureTerms, conditions, state restrictions, and minimum loan amounts apply. Before you apply for a secured loan, we encourage you to carefully consider whether this loan type is the right choice for you. If you can’t make your payments on a secured personal loan, you could end up losing the assets you provided for collateral. Not all applicants will qualify for larger loan amounts or most favorable loan terms. Loan approval and actual loan terms depend on the ability to meet underwriting requirements (including, but not limited to, a responsible credit history, sufficient income after monthly expenses, and availability of collateral) that will vary by lender.

BankingSoFi Lending Corp. (“SoFi”) operates this website in cooperation with Engine by MoneyLion presenting promotions for products and services offered by other banks, lenders, and financial institutions. If you select a promotion above, you will be connected to the website of the company offering the product. The promotions presented on this site are from companies that pay SoFi and Engine by MoneyLion compensation for marketing their products and services. This may affect whether a provider is featured on this site and could affect the order of presentation. Lantern and Engine by MoneyLion do not include all providers in the market or all of their available offerings. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

FG Trade/istockphoto

wagnerokasaki/istockphoto

Featured Image Credit: Deposit Photos.

AlertMe