Casting a Wider Net

The new term du jour is “bear market rally,” and the exercise du jour is trying to determine if any uptrends we see in markets are simply brief rallies in an otherwise downward trending period, or if they’re indications that we’re entering a new phase of positive momentum.

There are various ways to splice the price action and attempt to make a call on the above. I’m going to choose three indicators in order to gauge my confidence level with recent rallies.

The first, and perhaps most promising, is a simple comparison of the S&P 500 equal weighted Index vs. the S&P 500 market-cap weighted index (the one we use most often). Given that the five largest companies in the S&P 500 (Apple, Microsoft, Alphabet, Amazon, and Tesla) make up nearly 25% of the index, performance numbers are heavily influenced by a very small set of names.

What I want to see is a strengthening in performance from the other stocks in the index, which would give me more confidence that the market has more durability beyond the big names. So far in 2022, the equal weight index has outperformed the market cap weighted index by more than 5 percentage points, one indication that the market is quietly starting to exhibit better breadth.

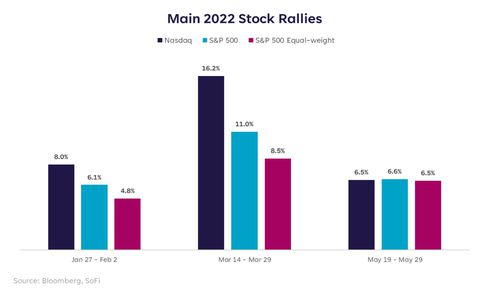

Catch and Release

Second, I wanted to look at the action that happened during each of the brief rallies we’ve seen in 2022. There have only been three periods of rallies lasting longer than three consecutive days (remember, this has been the worst start to a year in the stock market since 1970). Although each is a welcome sigh of relief, so far, they’ve felt more like a game of catch and release.

Of those periods, the first two were driven by large-cap stocks, particularly the big names in technology and communications. This is evidenced by stronger performance in the S&P 500 and the Nasdaq over those periods as compared to the S&P 500 equal weighted index.

What’s encouraging, however, is the most recent rally that took place between May 19-May 27 when all three indices performed in-line with one another. So rather than the mega caps and headline makers being the only stocks that caught a bid, the buying was spread out among more sectors and constituents. We need to see more of this to convince me though…one period does not make a trend.

Swimming in the Same Direction

Lastly, we can look at the percent of stocks advancing vs. the percent of stocks declining in order to see how many constituents are moving in the right direction. Using a 10-day average to smooth out the choppiness, so far in 2022 the max percent advancing was 67.0%. This compares to a pre-pandemic max of 70.9% in 2019. This measure has been increasing over the recent spring rallies but is still not quite to convincing levels.

In conclusion, I think we’ve done a lot of work this year in re-rating stocks to more reasonable levels given the rate environment, the inflation environment, and to prepare for the removal of monetary and fiscal stimulus. We’ve also done some work on finding our footing in order to establish a more durable uptrend after the big downdraft. But we still need a few more tallies in the breadth and strength columns to persuade me that we’re out of the woods. I’m optimistic that late June or early July will start to feel more convincing.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

More from MediaFeed:

6 ways to protect your money from inflation

Inflation has been squeezing — and infuriating — U.S. consumers for a long time now.

What began as an annoyance (an extra pinch at the gas pump and the grocery store) has turned into a painful reminder that budgeting and saving may be even more important than anyone ever thought. And without a plan to deal with inflation’s effects — day to day and over time — your dollars can lose purchasing power.

The good news is that it’s never too late to consider strategies that could protect your money from inflation, while also keeping in mind your personal financial situation, your goals, and your tolerance for risk.

Read on for intel on how to protect your money and yourself from inflation.

Related: What is wealth management?

nicoletaionescu / iStock

Wondering what inflation is exactly? In basic terms, inflation means prices are rising and your purchasing power is declining. You can’t get the goods and services you’re used to buying without paying more for them. And if your income doesn’t increase to match those higher prices — because you can’t get a pay raise that keeps up, or you’re a retiree on a fixed income — it can really impact your lifestyle.

The U.S. has been on a months-long run of record-setting inflation since the start of the coronavirus pandemic. And according to the U.S. Department of Labor Statistics, it’s the costs most people can’t avoid — like food, gas, and rent — that are driving the continued increase in the Consumer Price Index (the most commonly used measure of inflation).

It’s true that there are common causes of inflation and escalating prices aren’t uncommon, but what is happening right now is undoubtedly intense. Rates are hitting the highest numbers the U.S. has seen since the early 1980s, which means it’s the first time many consumers here have experienced inflation at this level.

But even a low inflation rate can erode purchasing power over the long haul. For example, according to the U.S. Inflation Calculator, if you purchased an item for $100 in 2000, that same item would have cost $150.30 in 2020 — before inflation soared. The dollar had an average inflation rate of 2.06% per year in the two decades between 2000 and 2020, producing a cumulative price increase of a whopping 50.30%.

That’s why preparing for inflation can be an important consideration for every consumer, whether you consider yourself a saver, a spender, an investor, or (like most people) you’re a mix of all three.

Recommended: Is Inflation a Good or Bad Thing for Consumers?

Yingko/istock

Needless to say, stuffing your money into a mattress or cookie jar probably isn’t the best strategy for protecting your hard-earned dollars.

Not only is an FDIC-insured savings account generally considered a safer place to keep your funds, but you also can earn interest on your money until you need it. Perhaps you’re saving for a down payment on a car or home, a wedding or vacation, or maybe for an unexpected expense.

Although most savings accounts pay minimal interest — usually not enough to counteract even low inflation rates — you’re at least earning something. And if you take time to occasionally review the interest rates various financial institutions are offering, you may be able to improve on what you’re currently getting.

For example, online financial institutions are more likely to offer high-yield savings accounts than traditional brick-and-mortar banks. So, if you’re comfortable with the idea of electronic banking, you may find a significantly higher annual percentage yield (APY). You also might be able to reduce or eliminate some of the fees you’re paying, which can boost your savings as well.

If the Federal Reserve continues to raise its benchmark interest rate in an effort to combat inflation, as it has indicated it will, you may see the rate on your current savings account slowly increase. But if it doesn’t, or if you don’t want to wait around for that to happen, it may make sense to start shopping for a smarter way to save right now.

Photodjo / iStock

Taking the time to reassess the potential earnings from your savings account can be an important step in offsetting inflation’s impact on your bottom line.

But there are other strategies you also may want to consider. Here are steps that can help you protect yourself from inflation.

Love portrait and love the world / iStock

It might be hard to believe when the housing market is this hot and prices are this high, but homeownership actually may help protect you from inflation.

If you’re a renter, you’re probably at the mercy of your landlord when it comes to how much your monthly payment could go up when it’s time to renew your lease. And during an inflationary period, your landlord may decide to raise your rent to reflect higher prices. If you decide to move, your new lease also could reflect the high inflation rate. Plus, you’ll have to go through the hassle of finding a new place and moving.

If you buy a house, on the other hand, you’re more likely to have a fixed monthly payment that’s locked in for the life of your mortgage. Another benefit: The value of the home you own may increase along with inflation. And if you hang onto your home until it’s paid off, you won’t have to worry about what housing prices (renting or owning) might look like in the future.

DepositPhotos.com

Especially if you’re a first-time homebuyer, you might feel more than a little overwhelmed thinking about signing off on a 30-year fixed-rate mortgage for, let’s say, $350,000.

It might help to take a deep breath and think about this: According to the U.S. Inflation Calculator, $350,000 in today’s dollars is equal to about $173,000 in 1992 dollars. Thirty years ago, somebody thought $173,000 was a crazy-high amount of money for a house. Now, it sounds like a bargain. It often takes us by surprise how prices (and salaries) do rise over the years.

If you’re borrowing money for 30 years (the most common mortgage term) at a competitive interest rate — and you aren’t paying more than the home’s appraised value — inflation could work for you. That’s because the value of money, including debt, declines as the inflation rate rises. So, the inflation-adjusted value of your mortgage payments goes down as inflation and your property value go up.

depositphotos.com

If you have the room and a knack for bargain-hunting, it may make sense to build up a supply of the kinds of goods that could be affected by inflationary prices. This is especially those items that are often linked to shortages.

Unfortunately, it isn’t really feasible for most folks to stockpile gasoline. But your backup supply might include canned goods, baby food, paper towels, toilet paper, and other necessities that you find on sale or can buy for less in bulk.

Keep in mind, though, that if you pay for those goods with a high-interest credit card and you don’t pay off the balance each month, you might not see any savings. (Which is another good reason to keep some money stashed in your checking and savings account to pay for such purchases.)

Valeriy_G/istockphoto

The price of durable goods (products that typically last at least three years) also can be affected by shortages and increased consumer demand.

If you need a new car, for example, and prices seem high for the make or model you want, it may be tempting to purchase a lower-quality replacement. Keep in mind, though, that over the long term, you could end up spending more on repairs than you would have if you bought the better brand. Or the less expensive make may not last as long as a better car would have.

You may find it’s a smarter strategy to get an auto loan and invest in the higher-priced car from the start.

martin-dm

A household budget can be a helpful tool any time, but it could be particularly useful when prices are soaring.

Even if you already have a budget, you may want to reevaluate your spending in categories that are or could be vulnerable to inflation, such as food, transportation, healthcare, and utilities. And you may have to look for categories you can spend less on (at least temporarily), such as entertainment, dining out, clothing, and vacations.

If you’ve put most of your bills on autopay, you also can check for “expense creep” on things like cable and Wi-Fi, subscription services, and utilities.

Sticking to a budget could help you avoid touching your emergency savings when times are tight—or, worse, overusing high-interest credit cards.

Once you’ve established a savings account (hopefully a high-interest one) for your emergency fund and other short-term expenses, you may want to look at investing as another strategy to combat inflation.

Though it carries more risk than keeping your money in a high-yield savings account, investing in stocks, mutual funds, or exchange-traded funds (ETFs) can help you grow your money for the future.

Once again, let’s go back 30 years to get some perspective. According to Officialdata.org’s S&P 500 data calculator, if you had invested $100 in the S&P 500 at the beginning of 1992, you’d come out with about $1,974.20 at the end of 2022 (assuming you reinvested all dividends). That’s a return on investment of 1,874.20%, or 10.42% per year. Even after adjusting for inflation, you’d be looking at a 7.87% return per year — which is better than most alternatives. Which all goes to say that investing may be a very good hedge against inflation.

nortonrsx

What is the best way to protect against inflation?

The best approach may be to prepare for the worst while hoping it doesn’t happen. This means finding ways to get the most for your money as a saver (perhaps with a savings account that pays more in interest), spender (adopting a budget and savvy buying tactics), and investor (with investments that keep growing your money over time).

Where should I put my money to combat inflation?

You may want to start by shopping for a savings account that offers a higher APY and/or lower fees. That way, you won’t be slowly losing money as your cash sits in the bank. Another option is to invest it, which is riskier but may yield you a higher return.

How can I prepare for hyperinflation?

You can use many of the same tactics to protect against runaway or hyperinflation as you would for high inflation. You might decide to stockpile goods now, while your money has value, for example. You may choose to buy a car or make another important purchase sooner rather than later. You also can evaluate what expenditures are “needs” vs. “wants” and budget appropriately. Also try not to panic — which can lead to poor decision-making.

RossHelen/ iStock

To younger consumers, today’s high inflation may seem like a new phenomenon. But inflation always has been — and always will be — a challenge.

While you probably can’t avoid inflation completely, with proactive planning, you may be able to blunt its impact on your day-to-day and long-term finances. If you haven’t already, you may want to review your savings, spending, and investing strategies to be sure you’re getting the most you can for your money.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

SoFi Checking and Savings is offered through SoFi Bank, N.A. ©2022 SoFi Bank, N.A. All rights reserved. Member FDIC. Equal Housing Lender.

SoFi members with direct deposit can earn up to 1.25% annual percentage yield (APY) interest on all account balances in their Checking and Savings accounts (including Vaults). Members without direct deposit will earn 0.70% APY on all account balances in their Checking and Savings accounts (including Vaults). Interest rates are variable and subject to change at any time. Rate of 1.25% APY is current as of 4/5/2022. Additional information can be found at http://www.sofi.com/legal/banking-rate-sheet

DepositPhotos.com

Damir Khabirov / iStock

Featured Image Credit: DepositPhotos.com.

AlertMe