If you fall behind on your auto loan payment, your lender may repossess your car. That means the lender can seize your vehicle to recoup some of the money it loaned you.

The bad news? It’s a double whammy. You no longer have a vehicle, and repossession can hurt your credit score. The good news? You may be able to get your car back, either by reinstating your car loan or through a process called redemption.

Here’s a look at the difference between these two strategies and how to know which, if either, is an option you can pursue.

How Car Repossession Works

When you take out a loan to buy a car, your lender will typically use your vehicle as collateral to secure the loan. That means that your lender has the right to take the vehicle away if you miss payments and default on the loan, also known as car repossession.The lender will usually sell the vehicle at auction in order to recover some of the money it loaned you.

Your loan contract will specify terms for repossession, defining what it means to default on your loan and laying out the consequences. In some cases, defaulting may mean missing just one payment. However, your lender will likely warn you that you’ve missed a payment and try to collect before repossessing your car. If the lender fails to collect and you’re in default, it can come and take your vehicle at any time and without warning.

Your car can also be repossessed if you fail to have proper insurance for your vehicle. Because your lender uses your vehicle to secure your loan, it has a vested interest in protecting it. If you allow your auto insurance policy to lapse, your lender may view that as a risk and use it as a reason to repossess your car.

(Learn more: Personal Loan Calculator)

What Is Reinstatement?

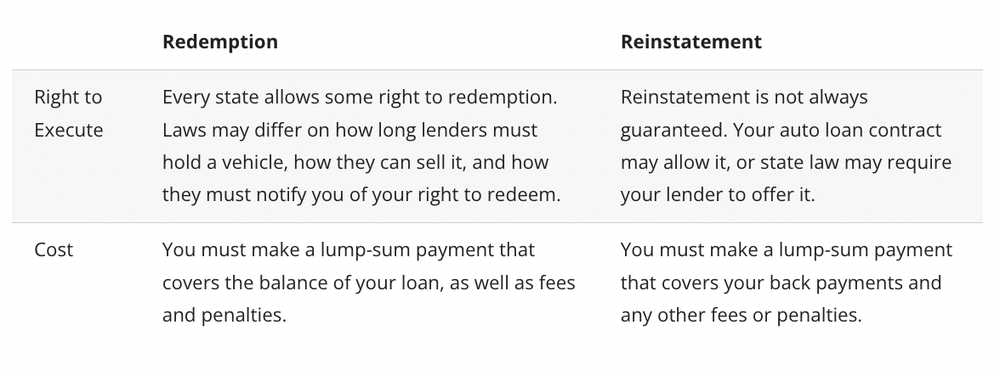

Reinstating your car loan is when you can make up any overdue payments, including covering the costs of the car repossession, and get your vehicle (and your loan) back after it’s been repossessed. Reinstatement basically takes the loan back to where it should be, and you would resume making payments on the loan as normal.

How Reinstating a Car Loan Works

If your car has been repossessed, all is not lost. You may be able to get it back by reinstating your loan.

Typically, you do this by bringing your loan up-to-date with a lump-sum payment that covers all past due payments, fees, and late charges. Your right to reinstatement might be built into your loan contract, or state law may require your lender to allow it. To find out if your state allows reinstatement, contact your state attorney general’s office or the state consumer protection agency.

If reinstatement is allowed through your loan agreement or state law, you can contact your lender to request a reinstatement quote, but do so as soon as possible. Your lender is then required to send you a notice within 15 days with the amount necessary to make your loan current. But be ready: At that point you may have as little as 10 to 15 days to reinstate your loan at that amount.

Note, too, that if the terms of the reinstatement notice aren’t feasible for you, your lender may be willing to negotiate.

When You Can’t Reinstate an Auto Loan

If your loan contract or state doesn’t specify your right to reinstate your auto loan, you may have to seek other options, such as redemption. What’s more, be aware that even if you do have the option of reinstating your auto loan, you have only a limited amount of time to do so. And if you don’t pay the necessary amount to bring your loan current under the terms of your reinstatement notice, or if your car is sold, you may forfeit your right to reinstatement.

When Redemption Is an Option

If you can’t reinstate your loan, another option may be loan redemption. When you redeem your car, you buy it back from your lender in a lump-sum payment. That likely will be more expensive than reinstating your loan, but it is more likely to be an available option.

Every state allows some form of redemption, and you typically can exercise this right until the lender sells the car. State laws differ in how long a lender must hold on to a car before selling it, how the lender can sell the vehicle, and how the lender has to notify you of your right to redeem.

Bear in mind that redeeming your car can be a costly process. You may have to cover costs, such as repossession expenses, towing charges, attorney’s fees, and late fees. As with reinstating your loan, the terms of redemption may be negotiable.

How Long Does a Repossession Stay on Your Credit Report?

An auto repossession typically has a negative effect on your credit report and will likely remain there for seven years. Like bankruptcies and collections accounts, repossessions are serious red flags for lenders if you are seeking credit in the future.

What’s more, failing to pay your auto loan on time can have its own negative impact on your credit score. Your lender can report you as delinquent on your loan for each month your payment is 30 or more days past due. This, too, can drag down your credit score, potentially for years to come.

The Takeaway

When your lender repossesses your car, it doesn’t necessarily have to leave you stranded. Reinstatement and redemption provide options for getting your car back, though the process can be costly.

It’s generally far better to avoid repossession in the first place. If you find your auto payments are becoming untenable, consider refinancing your auto loan to help make your monthly payments easier. Refinancing before you fall behind on payments typically has a minimal effect on your credit score. Note that refinancing after a repossession can be extremely difficult. Another option that may be available to you is to trade in your vehicle for a less expensive car with cheaper payments.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Lantern By

SoFiSoFi receives compensation in the event you obtain a loan, financial product, or service through the Lantern marketplace. This Lantern website is owned by SoFi Lending Corp., a lender licensed by the Department of Financial Protection and Innovation under the California Financing Law, license number 6054612; NMLS number 1121636. (nmlsconsumeraccess.). This site is NOT owned and operated by SoFi Bank. Loans, financial products, and services may not be available in all states.

All rates, fees, and terms are presented without guarantee and are subject to change pursuant to each provider’s discretion. There is no guarantee you will be approved or qualify for the advertised rates, fees, or terms presented. The actual terms you may receive depends on the things like benefits requested, your credit score, usage, history and other factors.

*Check your rate: To check the rates and terms you may qualify for, Lantern and/or its network lenders conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, the lender(s) you choose will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

All loan terms, including interest rate, and Annual Percentage Rate (APR), and monthly payments shown on this website are from lenders and are estimates based upon the limited information you provided and are for information purposes only. Estimated APR includes all applicable fees as required under the Truth in Lending Act. The actual loan terms you receive, including APR, will depend on the lender you select, their underwriting criteria, and your personal financial factors. The loan terms and rates presented are provided by the lenders and not by SoFi Lending Corp. or Lantern. Please review each lender’s Terms and Conditions for additional details.

Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website on credit (consumer.ftc.gov)

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.¹

SoFi’s Insights tool offers users the ability to connect both SoFi accounts and external accounts using Plaid, Inc.’s service. When you use the service to connect an account, you authorize SoFi to obtain account information from any external accounts as set forth in SoFi’s Terms of Use. SoFi assumes no responsibility for the timeliness, accuracy, deletion, non-delivery or failure to store any user data, loss of user data, communications, or personalization settings. You shall confirm the accuracy of Plaid data through sources independent of SoFi. The credit score provided to you is a VantageScore® based on TransUnion® (the “Processing Agent”) data.

Personal Loan

SoFi Lending Corp. (“SoFi”) operates this Personal Loan product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders/partners receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.Personal loan offers provided to customers on Lantern do not exceed 35.99% APR. An example of total amount paid on a personal loan of $10,000 for a term of 36 months at a rate of 10% would be equivalent to $11,616.12 over the 36 month life of the loan.

Student Loan RefinanceSoFi Lending Corp. (“SoFi”) operates this Student Loan Refinance product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

NOTICE: The debt ceiling legislation passed on June 2, 2023, codifies into law that federal student loan borrowers will be reentering repayment. The US Department of Education or your student loan servicer, or lender if you have FFEL loans, will notify you directly when your payments will resume For more information, please go to https://docs.house.gov/billsthisweek/20230529/BILLS-118hrPIH-fiscalresponsibility.pdf https://studentaid.gov/announcements-events/covid-19

If you are a federal student loan borrower considering refinancing, you should take into account the new income-driven payment plan, SAVE, which replaces REPAYE, seeks to make monthly payments more affordable, and offers forgiveness of balances that were originally $12,000 or lower after 120 payments, among other improvements. Also, please note that once you refinance federal student loans you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as SAVE, or extended repayment plans.

Auto Loan RefinanceAutomobile refinancing loan information presented on this Lantern website is from Caribou, AUTOPAY, Engine by MoneyLion, and each of Engine’s partners (along with their affiliated companies). Caribou, AUTOPAY, and Engine by MoneyLion pay SoFi compensation for marketing their products and services on the Lantern site.

Auto loan refinance information presented on this Lantern site is indicative and subject to you fulfilling the lender’s requirements, including but not limited to: credit standards, loan size, vehicle condition, and odometer reading. Loan rates and terms as presented on this Lantern site are subject to change when you reach the lender and may depend on your creditworthiness, consult with the lender for more details. Additional terms and conditions may apply and all terms may vary by your state of residence.

Secured Lending DisclosureTerms, conditions, state restrictions, and minimum loan amounts apply. Before you apply for a secured loan, we encourage you to carefully consider whether this loan type is the right choice for you. If you can’t make your payments on a secured personal loan, you could end up losing the assets you provided for collateral. Not all applicants will qualify for larger loan amounts or most favorable loan terms. Loan approval and actual loan terms depend on the ability to meet underwriting requirements (including, but not limited to, a responsible credit history, sufficient income after monthly expenses, and availability of collateral) that will vary by lender.

BankingSoFi Lending Corp. (“SoFi”) operates this website in cooperation with Engine by MoneyLion presenting promotions for products and services offered by other banks, lenders, and financial institutions. If you select a promotion above, you will be connected to the website of the company offering the product. The promotions presented on this site are from companies that pay SoFi and Engine by MoneyLion compensation for marketing their products and services. This may affect whether a provider is featured on this site and could affect the order of presentation. Lantern and Engine by MoneyLion do not include all providers in the market or all of their available offerings. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

More from MediaFeed:

Yikes: These electric car costs may be much higher than they are for gas cars

At first, electric vehicles (EVs) were marketed as luxury cars with price tags that put them out of reach for most people. However, as interest in eco-friendly cars rises, more automakers are releasing electric cars aimed at the masses. S&P Global Mobility forecasts there will be more than 28 million electric cars in operation by 2030.

These cars promise to be environmentally friendly and save you money at the gas pump. However, the price of gas isn’t the only cost to consider. Read on to learn the factors that can affect the cost of an electric car, as well as look at whether electric cars are more cost-effective.

(Learn more atPersonal Loan Calculator)

martin-dm/istockphoto

Electric cars, also known as electric vehicles or EVs, are expected to surge in popularity as tax incentives make electric car costs more affordable.

Consumers who buy a new electric car in the years 2023 through 2032 may be eligible for a $7,500 clean vehicle tax credit. The Inflation Reduction Act of 2022 also offers federal tax credits of up to $4,000 for eligible consumers who buy a used electric car.

Electric cars are typically more expensive than your average auto, but the ongoing cost of maintaining an electric car can be cheaper. One of the reasons for this is that electric cars have fewer moving parts than traditional cars and don’t require oil changes.

Sofi

As of August 2023, the average price of an electric car stood at $53,376, down 18.7% from the year before, according to Kelley Blue Book® data. Across the auto industry, the average transaction price of new cars stood at $48,451.

Although the average transaction price of electric cars has declined in 2023, electric cars still remain more expensive than conventional cars on average.

Here are some of the average car transaction prices by category as of August 2023, according to KBB data:

wellphoto/istockphoto

In addition to the price you’ll pay to drive an electric car off the lot, there will be other costs you’ll have to account for over the life of the vehicle, from charging to maintenance to insurance. We examine some of those added costs below.

Electric Car Maintenance Costs

Electric cars have fewer moving parts than their gas-powered counterparts. As a result, there are fewer parts subject to wear and tear and therefore in need of regular maintenance. You’ll never have to worry about getting an oil change with an electric car.

Any vehicle can have ongoing maintenance costs, such as the costs of rotating tires or replacing windshield wipers. But the average cost of maintaining an electric car over a five-year period is about $300 less than the cost of maintaining a gas-powered vehicle, according to the National Automobile Dealers Association (NADA).

Over the course of a vehicle’s lifecycle, some metrics suggest that electric car maintenance costs are 60% to 70% less than the average cost of maintaining a traditional car. The average internal combustion engine (ICE) car has nearly 10,000 parts, whereas an electric car has about 700, according to Cox Automotive.

Electric cars generally have an expected battery lifetime of 12 to 15 years. If your battery dies, one of the most expensive car repairs is replacing your electric car battery. EV battery replacements can cost $5,000 to $15,000, but the battery may have a manufacturer’s warranty covering eight years or 100,000 miles.

jozzeppe/istockphoto

When you charge your electric vehicle, you’ll pay per kilowatt-hour (kWh). The price typically ranges from 10 cents to 35 cents per kWh, whereas regular gasoline typically costs between $3 and $4 per gallon in 2023.

If you charge your electric car at home, it could inflate your electric bill by $48 to $72 each month. By comparison, pumping 25 to 40 gallons of gasoline into a gas-powered vehicle at a price of $3.50 per gallon each month could cost between $87.50 to $140.

Charging your electric vehicle at home is typically the slowest but most cost-effective method of charging. You can also go to public charging stations, which are typically faster but more expensive than charging at home.

Some charging stations may offer free charging, although the fastest charging stations with direct current (DC) fast charging may cost up to 40 cents per kWh. Overall, the cost of recharging your electric car is typically lower than the cost of fueling up a gas-powered car.

saruservice/istockphoto

In general, owners of electric vehicles can face higher insurance premiums compared with those of gas-only vehicles. This is due in part to the fact that vehicles that are more expensive tend to cost more to insure. Additionally, repairs for electric vehicles may be more costly due to the price of their parts as well as the more limited options in technicians who know how to repair electric vehicles.

Of course, as electric vehicles grow more popular, their sticker price and the cost of repairs will likely go down, which will likely also push down insurance rates for EVs.

As of 2023, the average five-year cost of collision and liability insurance for electric cars is $6,824 vs. $5,707 to insure the average gas-powered vehicle, according to Kelley Blue Book data cited by NADA.

boschettophotography/istockphoto

Electric cars have a higher rate of depreciation than conventional cars, according to new research. An empirical analysis of the depreciation of electric cars vs. gasoline vehicles found electric cars can lose 13.9% of their value each year compared with 10.4% for gas-powered cars.

Cars typically depreciate in value over time, and car depreciation diminishes the resale value of your vehicle.

deepblue4you/istockphoto

Here are some of the environmental benefits of electric cars:

- Electric cars are powered by electric motors fueled by rechargeable batteries, not internal combustion engines

- Electric cars produce zero tailpipe emissions

- Electric cars typically have a smaller carbon footprint than conventional cars

- Electric cars don’t leak motor oil and don’t require any oil changes by design

Electric cars don’t emit carbon dioxide or smog when operating on the roadways. This can help improve air quality over time, although manufacturing electric cars and recharging their batteries can create carbon pollution.

When comparing the carbon footprint of electric cars vs. conventional cars, the U.S. Environmental Protection Agency says electric cars typically have a smaller carbon footprint than gas-powered vehicles.

In the future, electric cars can become greener over their lifecycle if and when power plants and energy grids transition to zero-emission electricity. The United States has set a goal of 100% carbon pollution-free electricity by 2035, according to a May 2023 report prepared by the U.S. Department of Energy’s Office of Policy.

SimonSkafar/istockphoto

If you’re choosing between an electric vehicle and a traditional gas-powered option, it’s important to weigh out the pros and cons of electric cars.

Sofi

While the average upfront cost of purchasing a new electric vehicle may be more than the average gas-powered car, they are cheaper to operate and maintain, and you could ultimately save thousands of dollars over the life of the car. What’s more, government incentive programs may reduce your out-of-pocket costs by a significant amount, making an electric car a more feasible option for those with smaller budgets.

Still, there is some give and take with the costs of owning an electric vehicle to keep in mind. For one, insurance premiums tend to be higher. And while there is less maintenance needed overall, some repairs like battery replacement can be costly.

You’ll also want to keep in mind the cost of charging, including if you want to install an at-home charger, the most cost-effective option. All told, however, the annual cost of charging electric cars is typically cheaper than the annual cost of fueling up a gas-powered car.

Pollyana Ventura/istockphoto

When it comes to purchasing an electric vehicle, your options are the same as buying a traditional car. Here’s a look at the ways you can pay for an electric car:

Cash

If you have enough savings on hand, you can buy a vehicle in cash. Doing so may give you some leverage as you negotiate a purchase price. It will also mean you don’t have to pay any extra costs in the form of loan fees and interest. You’ll own the car outright with 100% equity and no lienholders listed on your car title.

Financing

You may also choose to finance your car purchase, taking out a loan through a bank or other financial institution. Or, you may consider dealership financing. These are among the different types of car loans you can explore.

When you take out an auto loan, you usually make a down payment and then pay off the rest of the cost of the vehicle, also known as your car loan principal, over a series of monthly payments. In return for allowing you to borrow the funds, your lender will typically charge interest, adding to the cost of your loan. Some lenders offer 0% annual percentage rate (APR) car loans.

The amount of interest a lender charges will depend on a number of factors, including your credit score, income, and whether you’re using a co-borrower. Lenders typically offer their best rate to borrowers with excellent credit.

Leasing

Another option you have when it comes to getting an electric car is leasing. There are a number of benefits to leasing an electric car as opposed to buying it outright, including being able to avoid the steep depreciation that comes with electric vehicles, steering clear of dealing with eventual battery degradation, and getting access to newer, evolving technology when you trade in your car at regular intervals.

However, you’ll lose out on potential federal and state tax credits when you lease instead of buy — though sometimes the leasing company may pass on their savings to the consumer. Plus, with leasing, you won’t actually own the vehicle.

Tramino/istockphoto

In the future, you may consider refinancing your auto loan. When you refinance car loan debt, you take out a new loan with better terms or interest rates and pay off your old loan.

You may be wondering, when should you consider refinancing a car? If your financial situation improves, interest rates drop, or your electric car payments become unmanageable, looking into refinancing may be worthwhile.

It’s important to consider the benefits and disadvantages of refinancing, though. On the plus side, you may be able to settle on more manageable monthly payments, save money on interest, and free up cash to put toward other financial goals. On the other hand, you may also find yourself dealing with prepayment penalties and fees to originate a new loan.

Olivier Le Moal/istockphoto

While you’ll skip costs at the gas station with an electric vehicle, there are still costs of an electric car to keep in mind if you’re considering getting one. Added costs can include charging — both at public stations and at home — as well as maintenance and insurance. Still, overall, the average cost of an electric car does tend to be cheaper in terms of operation and maintenance than its gas-powered counterparts, even if their sticker price is currently higher.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Lantern By

SoFiSoFi receives compensation in the event you obtain a loan, financial product, or service through the Lantern marketplace. This Lantern website is owned by SoFi Lending Corp., a lender licensed by the Department of Financial Protection and Innovation under the California Financing Law, license number 6054612; NMLS number 1121636. (www.nmlsconsumeraccess.org). This site is NOT owned and operated by SoFi Bank. Loans, financial products, and services may not be available in all states.

All rates, fees, and terms are presented without guarantee and are subject to change pursuant to each provider’s discretion. There is no guarantee you will be approved or qualify for the advertised rates, fees, or terms presented. The actual terms you may receive depends on the things like benefits requested, your credit score, usage, history and other factors.

*Check your rate: To check the rates and terms you may qualify for, Lantern and/or its network lenders conducts a soft credit pull that will not affect your credit score. However, if you choose a product and continue your application, the lender(s) you choose will request your full credit report from one or more consumer reporting agencies, which is considered a hard credit pull and may affect your credit.

All loan terms, including interest rate, and Annual Percentage Rate (APR), and monthly payments shown on this website are from lenders and are estimates based upon the limited information you provided and are for information purposes only. Estimated APR includes all applicable fees as required under the Truth in Lending Act. The actual loan terms you receive, including APR, will depend on the lender you select, their underwriting criteria, and your personal financial factors. The loan terms and rates presented are provided by the lenders and not by SoFi Lending Corp. or Lantern. Please review each lender’s Terms and Conditions for additional details.

Many factors affect your credit scores and the interest rates you may receive. SoFi is not a Credit Repair Organization as defined under federal or state law, including the Credit Repair Organizations Act. SoFi does not provide “credit repair” services or advice or assistance regarding “rebuilding” or “improving” your credit record, credit history, or credit rating. For details, see the FTC’s website on credit (consumer.ftc.gov)

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.¹

SoFi’s Insights tool offers users the ability to connect both SoFi accounts and external accounts using Plaid, Inc.’s service. When you use the service to connect an account, you authorize SoFi to obtain account information from any external accounts as set forth in SoFi’s Terms of Use. SoFi assumes no responsibility for the timeliness, accuracy, deletion, non-delivery or failure to store any user data, loss of user data, communications, or personalization settings. You shall confirm the accuracy of Plaid data through sources independent of SoFi. The credit score provided to you is a VantageScore® based on TransUnion® (the “Processing Agent”) data.

Personal Loan

SoFi Lending Corp. (“SoFi”) operates this Personal Loan product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders/partners receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.Personal loan offers provided to customers on Lantern do not exceed 35.99% APR. An example of total amount paid on a personal loan of $10,000 for a term of 36 months at a rate of 10% would be equivalent to $11,616.12 over the 36 month life of the loan.

Student Loan RefinanceSoFi Lending Corp. (“SoFi”) operates this Student Loan Refinance product in cooperation with Engine by MoneyLion. If you submit a loan inquiry, SoFi will deliver your information to Engine by MoneyLion, and Engine by MoneyLion will deliver to its network of lenders/partners to review to determine if you are eligible for pre-qualified or pre-approved offers. The lenders receiving your information will also obtain your credit information from a credit reporting agency. If you meet one or more lender’s and/or partner’s conditions for eligibility, pre-qualified and pre-approved offers from one or more lenders/partners will be presented to you here on the Lantern website. More information about Engine by MoneyLion, the process, and its lenders/partners is described on the loan inquiry form you will reach by visiting our Personal Loans page as well as our Student Loan Refinance page. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

NOTICE: The debt ceiling legislation passed on June 2, 2023, codifies into law that federal student loan borrowers will be reentering repayment. The US Department of Education or your student loan servicer, or lender if you have FFEL loans, will notify you directly when your payments will resume For more information, please go to https://docs.house.gov/billsthisweek/20230529/BILLS-118hrPIH-fiscalresponsibility.pdf https://studentaid.gov/announcements-events/covid-19

If you are a federal student loan borrower considering refinancing, you should take into account the new income-driven payment plan, SAVE, which replaces REPAYE, seeks to make monthly payments more affordable, and offers forgiveness of balances that were originally $12,000 or lower after 120 payments, among other improvements. Also, please note that once you refinance federal student loans you will no longer be eligible for current or future flexible payment options available to federal loan borrowers, including but not limited to income-based repayment plans, such as SAVE, or extended repayment plans.

Auto Loan RefinanceAutomobile refinancing loan information presented on this Lantern website is from Caribou, AUTOPAY, Engine by MoneyLion, and each of Engine’s partners (along with their affiliated companies). Caribou, AUTOPAY, and Engine by MoneyLion pay SoFi compensation for marketing their products and services on the Lantern site.

Auto loan refinance information presented on this Lantern site is indicative and subject to you fulfilling the lender’s requirements, including but not limited to: credit standards, loan size, vehicle condition, and odometer reading. Loan rates and terms as presented on this Lantern site are subject to change when you reach the lender and may depend on your creditworthiness, consult with the lender for more details. Additional terms and conditions may apply and all terms may vary by your state of residence.

Secured Lending DisclosureTerms, conditions, state restrictions, and minimum loan amounts apply. Before you apply for a secured loan, we encourage you to carefully consider whether this loan type is the right choice for you. If you can’t make your payments on a secured personal loan, you could end up losing the assets you provided for collateral. Not all applicants will qualify for larger loan amounts or most favorable loan terms. Loan approval and actual loan terms depend on the ability to meet underwriting requirements (including, but not limited to, a responsible credit history, sufficient income after monthly expenses, and availability of collateral) that will vary by lender.

BankingSoFi Lending Corp. (“SoFi”) operates this website in cooperation with Engine by MoneyLion presenting promotions for products and services offered by other banks, lenders, and financial institutions. If you select a promotion above, you will be connected to the website of the company offering the product. The promotions presented on this site are from companies that pay SoFi and Engine by MoneyLion compensation for marketing their products and services. This may affect whether a provider is featured on this site and could affect the order of presentation. Lantern and Engine by MoneyLion do not include all providers in the market or all of their available offerings. Click to learn more about Engine’s Licenses and Disclosures, Terms of Service, and Privacy Policy.

Basilico Studio Stock/istockphoto

kate_sept2004/istockphoto

Featured Image Credit: Zbynek Pospisil / iStock.

AlertMe