It’s Not Over Till It’s Over

The good news is that when this rough patch is over, we can look back on it as another history lesson and use it as a guide for cycles to come. The bad news is I don’t think it’s over yet. But we’re getting closer.

As is always true, the market looks forward while economic data looks backward. The size of the time-gap between the two varies but is measured in months — not days or weeks.

At this point, with a drawdown of almost 30% in the Nasdaq and almost 20% in the S&P, we can agree that the market started “forecasting” rough waters months ago. The reason I don’t think it’s quite over yet is because the economic data hasn’t entirely caught up.

Related: What is wealth management?

It’s Always Darkest Before the Dawn

Last week I wrote that the temptation to call peak inflation has become almost as contagious as the temptation to call a market bottom. As has been proven many times, calling bottoms with any consistent accuracy is nearly impossible.

What we can do, however, is shift our focus to some of the economic indicators that haven’t cracked yet. If the market cracks first, the economic data should crack later, and we can start to feel more confident that the darkest hours are behind us.

What am I watching? The stuff that everyone keeps saying is so strong — the last few items in the “pros” column after so many moved to “cons.”

The most important of these is the consumer. Let me be clear that I’m not hoping for the consumer to fall apart. I’m simply saying that there likely needs to be some cooling in a few more metrics in order for inflation to fall, for the Fed to retract its claws, and for us to confirm that the market can stop forecasting dreadful days ahead.

Spending With a Vengeance

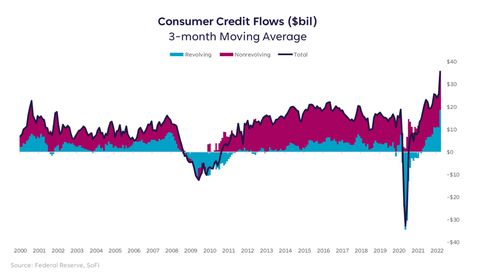

Despite inflation scaring the heck out of markets, it hasn’t yet scared the heck out of consumer spending. Which means demand hasn’t cooled much, and higher prices haven’t stopped the post-Covid revenge spending spree.

But something that says the spending is getting a little harder to stomach is the recent growth in revolving consumer debt.

Yes, consumers built up their savings during the pandemic to $2.5 trillion, and that number still sits around $2.4 trillion. And yes, personal income levels have risen. But the personal savings rate has fallen to 6.2% — below the pre-pandemic level of 7.3%. Which means the level of spending increased faster than the level of income.

At some point, people have to make tough choices and demand should cool. The data that will reflect the cooling is personal consumption expenditures, retail sales, and revenues of consumer-dependent companies. In turn, inflation should reflect a more balanced supply/demand relationship.

Dropping Shoes

While we wait for some of the last shoes to drop, and for the darkest days to be behind us, stay focused on diversification and investing, not trading. This type of bumpy environment is when short-term trades can turn into long-term mistakes. Instead, work on building a portfolio that has allocations to high quality growth opportunities, while diversifying it with defensive positions for those rough periods. And wait for the gap to close between market action and economic data.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

Investment Risk: Diversification can help reduce some investment risk. It cannot guarantee profit, or fully protect in a down market.

More from MediaFeed:

What happens to your debt when you die?

Do you know what will happen to your debt when you die? Some debts are forgiven while others may be passed down to heirs. Read on for the answers to some of the most frequently asked questions related to death and debt.

SPONSORED: Get MORE out of your credit cards

Know which of your credit cards is best for each purchase. Maximize your rewards, cash back, points and more with Uthrive, a truly free credit card rewards app. Get it here.

panida wijitpanya / istockphoto

In order to accurately answer this question, we need to examine the most common types of debt people accumulate. In other words: Not all debt is equal. The type of debt you have and when you accumulated the debt will determine how and if your debt is passed on to others when you die.

The Most Common Types Of Debt

DepositPhotos.com

If you die with credit card debt, there are two things that may happen:

- Your debt may be forgiven and written off by the credit card company

- The debt will be passed on and the responsibility of a survivor

DepositPhotos.com

If you are the sole owner of the debt when you die, (not married or a cosigner) the credit card companies will be involved in the probate process. The money left in your estate, any retirement accounts, or other items worth money will be sold and the outstanding debts will be paid.

If there is not enough money in your estate to pay off the remaining credit card balance, your children or beneficiaries will not be required to pay the remaining balance. The outstanding debt will be “forgiven” by the credit card company.

Farknot_Architect / istockphoto

If the credit card is a joint account with a living spouse or a cosigner, the other account holder will be responsible for the debt. If you have authorized users on the account but they are not the account owner, the users will not be responsible for the debt.

bernardbodo / istockphoto

This is one of those myths that continues to live on. Credit card debt does not go away after seven years. The confusion with the seven-year time frame comes from the credit report time requirement.

After seven years, old debts begin to fall off of your credit report. Your debt, however, is still very much alive and owed. Lenders can and will continue to pursue the amount owed until it is paid, settled, or charged off. Do not be fooled into thinking your credit card debt will go away after seven years.

Farknot_Architect / istockphoto

The quick answer? It depends. There are several factors that determine if a deceased spouse’s credit card debt will be passed along to the surviving spouse. If the credit card debt was incurred before marriage and the deceased spouse was the sole owner of the account, in most cases, the debt will not be the responsibility of the surviving spouse.

If the credit card debt was incurred after marriage and the deceased spouse was the sole owner of the account, the state you live in determines the surviving spouse’s responsibility. If you live in one of these community property states and the debt was incurred after marriage, the surviving spouse is responsible for the credit card debt of their spouse regardless of the account ownership:

- Arizona

- California

- Idaho

- Louisiana

- Nevada

- New Mexico

- Texas

- Washington

- Wisconsin

If you do not live in one of these states, generally the surviving spouse will not be responsible for the credit card debt if they were not a joint owner of the account. If you are a joint owner on the account, you are now solely responsible for the debt.

DepositPhotos.com

Again, where you live determines what can happen to your medical bills when you die. Generally speaking, children and heirs will not be required to pay back the outstanding medical bills of their parents. With that being said, there are a couple of instances where a child could be responsible for the medical debt of their parents.

DepositPhotos.com

When a child cosigns admission paperwork acknowledging financial responsibility if the adult is unable to pay their bills, this debt may be passed down to the child.

gorodenkoff / istockphoto

There are 26 states that have filial responsibility laws that state a child may be responsible for a deceased parent’s medical debt in certain situations. The states that have filial responsibility laws are:

- Alaska

- Kentucky

- New Jersey

- Tennessee

- Arkansas

- Louisiana

- North Carolina

- Utah

- Indiana

- Nevada

- California

- Maryland

- North Dakota

- Vermont

- Connecticut

- Massachusetts

- Ohio

- Virginia

- Iowa

- New Hampshire

- Delaware

- Mississippi

- Oregon

- West Virginia

- Georgia

- Montana

- Pennsylvania

- South Dakota

- Rhode Island

Now, before you become overly concerned about living in one of these states, understand that the enforcement of filial responsibility laws is extremely rare. If you have significant medical debt, consult with an attorney in your state to see exactly what responsibility your adult children may be required to pay back.

Rawpixel / istockphoto

Student loan debt may or may not be passed on to survivors when the borrower dies. What happens to the loan depends on what type of loan was taken out and when it was established.

Ta Nu/ istockphoto

If you have federal student loans, they will be forgiven upon death. Federal student loans do not pass on to others as long as a death certificate is presented to the lender. Federal student loans that fall into this category are:

- Direct Subsidized Loans

- Direct Consolidation Loans

- Direct Unsubsidized Loans

- Federal Perkins Loans

zimmytws / istockphoto

On Nov. 20, 2018, the Economic Growth, Regulatory Relief, and Consumer Protection Act was amended. The added section releases cosigners of a private student loan from financial responsibility if the primary borrower dies. Due to this, all new private student loans with cosigners are not required to repay the loan upon the student’s death.

However, student loans with cosigners taken out before Nov. 20, 2018, may still require the cosigner to be held responsible for the debt.

istockphoto

Federal Direct PLUS Loans are also forgiven upon the student’s death. In the past, the parent who signed for the PLUS loan was required to bear the burden of the tax responsibility and file the forgiveness as “income” after a child’s death.

Currently, The Tax Cuts and Jobs Act of 2017, is in effect and releases parents from this tax responsibility. This tax stipulation remains in effect until the year 2025.

designer491 / istockphoto

There is several different scenarios involving vehicle loan debt upon the borrower’s death. If the auto loan has a cosigner or the vehicle was purchased in a community property state after a couple was married, the cosigner or spouse is responsible to repay the auto loan.

If the loan was obtained before marriage and is only in the deceased spouse’s name, generally the surviving spouse is not held responsible for the debt. The bank will take possession of the vehicle to settle the outstanding debt or the surviving spouse can pay off the vehicle loan.

If the borrower is not married, the survivors can either pay off the vehicle loan and keep the vehicle, sell the vehicle and pay off the loan or return the vehicle to the bank. Heirs do not inherit vehicle loan debt.

DepositPhotos.com

Payday loan debt is very similar to credit card debt when you die. If there was not a cosigner or someone else listed as jointly responsible for the loan, then the company writes off the debt as a loss. Payday loan debt is not transferred to heirs but may be the responsibility of a surviving spouse if the debt was incurred after marriage in a community property state.

relif / istockphoto

In probate, the home must be paid off with the funds from the estate or the mortgage company must agree to let someone else inherit the loan. If you still owe money on your home, your spouse or heirs usually have three separate options:

Option 1: Sell the home to pay off the outstanding mortgage. The executor of the will can initiate a home sale to fulfill the outstanding debt obligations. If the home is not worth what is owed, additional money from the estate will be used to pay off the mortgage. If additional money is still required, the bank can take possession of the property.

Option 2: If there is enough money in your estate, your heirs can use that money to pay off the mortgage. Or the beneficiaries can use their own money to pay off the loan in full.

Option 3: If there is not enough money in the estate to pay off the loan, an heir may elect to contact the lender in an attempt to take over the loan. The loan would need to be transferred into the new borrower’s name which would require the heir to meet the credit obligations for a loan.

PRImageFactory / istockphoto

Lenders can force the sale of a property to fulfill the outstanding equity loan balance if the estate does not have enough capital to pay it off. This is another scenario where the heir may be able to apply with the lender to take over the payments.

Depositphotos

If you have federal tax debt when you die, the IRS gets the first chance at your estate. Legally, the executor of the state is unable to pay any other debt or obligation until the federal tax debt is settled.

If a substantial amount is owed, the IRS will quickly put a lien on any property owned by the deceased in an attempt to satisfy the debt. The federal government will get their money one way or another – but the heirs will not personally be liable for the outstanding tax debt.

supawat bursuk / istockphoto

There is not an automatic notification process when a person dies. The next of kin or executor of the state is required to contact the bank and provide a copy of the descendant’s death certificate.

When the death certificate is presented, the financial institution will freeze all of the associated accounts until the probate process is completed. If money is not owed to other lenders, the beneficiaries will be given access to any monies left in the deceased person’s accounts.

marchmeena29 / istockphoto

Even though most debts will not be passed on to your heirs when you die, you may not want them to deal with the hassle of paying off all your debt with your estate – only to be left with nothing.

If you have struggled with debt your entire life, a cheap term life insurance policy may be an option to leave a small inheritance to your heirs. Most life insurance policies are dispersed tax-free and are not accessible to creditors.

sturti

Leaving debt behind is a fear many seniors face. On the bright side, your heirs will usually not be personally responsible for paying off your outstanding debts. However, the sooner you can clean up your own financial mess, the better.

Do your best to start paying off your debt so your executor is not faced with a long probate process. If you need help getting started, check out this related post The Debt Payoff Playbook.

This article originally appeared on Arrest Your Debt and was syndicated by MediaFeed.org.

Deposit Photos

tumsasedgars/istock

Featured Image Credit: RossHelen/ iStock.

AlertMe