If you’re overwhelmed by credit card debt, you might consider credit card debt forgiveness, which can involve paying less than you owe. This type of credit forgiveness is rare, however, and it usually comes with some financial consequences.

Still, if you’re unable to repay your credit card balance, it may be an option worth exploring. Read on to learn how to get credit card debt forgiven and what options there are to credit card forgiveness.

What Is Credit Card Debt Forgiveness?

Credit card debt forgiveness occurs when a portion of your credit card debt is effectively erased. However, this rarely happens. And when it does, it usually comes at a high cost.

As part of the terms and conditions you agreed to when signing up for a credit card, you likely committed to repaying your credit card debt accrued from swiping your card to make purchases. For this reason, it’s unlikely the credit card company will forgive your debt unless you have a compelling reason for why you don’t have to repay it.

(If your identity was stolen and a fraudster ran up your credit card bill, for instance, you’re probably not responsible for repaying the outstanding balance. In this case, you may consider disputing a credit card charge.)

When you don’t pay your credit card bill for an extended time, the credit card company may sell your debt to a debt collector. At this point, the debt collector will reach out to try to get you to repay all or a portion of the debt you owe. However, if you agree to repay a portion of your debt, they may forgive the rest, resulting in credit debt forgiveness.

How Does Debt Forgiveness Work for Credit Cards?

If a debt collector forgives your debt, you’ll generally still have to pay off a portion of the amount you racked up. Here’s a look at how credit card debt forgiveness works:

- Say that you owe $10,000 in outstanding credit card debt. If you haven’t paid your bill for the last six months — not even your credit card minimum payment — your credit card company may have sold the debt to a debt collector.

- At this point, you’ll no longer communicate with your credit card company about debt negotiations since the debt collector is now responsible for recouping the loss.

- If you agree to repay $5,000 of the debt, your debt collector may require you to make a lump sum payment or installment payments over a set period of time.

- This means that the other $5,000 of your outstanding credit card balance is now forgiven, meaning you don’t have to pay it.

While this may seem like a relief, here’s one important point to note: You’re still responsible for paying taxes on the amount of credit card forgiveness you receive in most cases. Essentially, you will claim the forgiven debt as taxable income and report it on your tax return.

When Does Credit Card Debt Forgiveness Work Best?

When you’ve fallen behind on your credit card payments and your creditor sells your debt to a debt collector for a fraction of the total balance, this is usually the best time to request credit forgiveness. Typically, debt collectors are more willing to settle some of your debt since they purchased your debt for a portion of what you owe. In other words, any debt you agree to pay back will help the debt collector make a profit from the transaction.

However, if your debt has not yet gone to a debt collector and the creditor is about to charge-off your account, you could still consider credit card forgiveness. A charge-off means that the creditor is accepting your debt as a loss. Therefore, they can recoup the funds by selling your debt to a debt collector. So, before they sell the debt, they might be willing to negotiate credit card debt forgiveness with you.

How Credit Card Debt Forgiveness May Affect Your Credit

The most significant financial implication of credit card debt forgiveness is the negative impact it can have on your credit. When you don’t pay your credit card bill for an extended amount of time, the creditor may report this as a charge-off to the three major credit bureaus (TransUnion, Equifax, and Experian). A charge-off indicates that you didn’t follow through with your financial commitments to a lender, and it can stay on your credit report for up to seven years.

Because credit bureaus use this information to calculate your credit score, a charge-off could lower your score for a while. A lower credit score may make it challenging to qualify for future loans or credit cards. And if you do qualify, you may have to pay a higher than average credit card interest rate, which can make borrowing more expensive.

To avoid this situation, it’s best to contact your credit card issuer as soon as you get behind on payments. Credit card companies may be willing to help you if you’ve fallen on hard times. They may offer a hardship plan, which can lower your monthly payments or reduce your interest for a set amount of time and ultimately help you get back on your feet. This is only a temporary solution though, so if your financial issues are more significant, you may need to explore another solution.

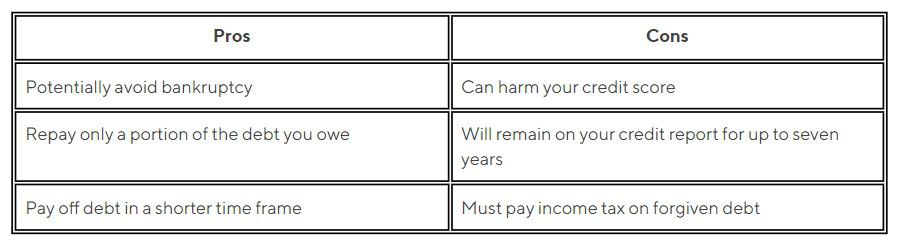

Pros and Cons of Credit Card Debt Forgiveness

If you can’t make your credit card payments, credit card forgiveness might be a viable option. But, while getting your debt forgiven can help alleviate the financial burden, it also can harm your credit and cost you financially.

Here’s a breakdown of the pros and cons of pursuing credit card debt forgiveness.

Alternatives to Credit Card Debt Forgiveness

An alternative to credit card debt forgiveness may make more sense for your financial situation. Exploring all of your options in advance can help ensure that you make the best decision for your needs.

Debt Management

Third-party credit counseling agencies offer debt management plans that help you establish a plan for debt repayment. Working with one of these agencies may help you lower the fees you owe as well as your interest rate. However, you usually must agree to repay the total amount of outstanding debt before moving forward.

With a debt management plan, you’ll make one monthly payment to the credit counselor, who will then distribute the funds among the creditors you owe. Most plans help you repay your debt within three to five years. During this time, your account will still accrue interest, though your creditor might be willing to offer a lower rate.

To use one of these plans, you usually have to close your credit card account. This can negatively impact your credit score since it lowers your total credit card limit, thus increasing your credit utilization rate. Your credit utilization ratio is one of the most significant factors credit bureaus use when calculating your credit score.

Also, you will likely have to pay a monthly fee to your credit counselor. If considering this option, carefully vet the counselors you are considering and make sure the one you are working with has a good reputation.

Debt Settlement

Working with a debt settlement company can help you to lower the amount of debt you owe. For example, if you owe $10,000 as your credit card balance, the credit debt settlement company may try to help you settle your debt for $5,000 instead. But, of course, this strategy will only work if the creditor would rather have some of your debt repaid instead of having you default on the account.

Debt settlement also can harm your credit. Usually, debt settlement companies require you to stop making credit card payments while they negotiate with your creditor. At this time, your payments will go toward the debt settlement company so they can offer your creditor a lump sum payment as an incentive to settle your debt. However, pausing payments can negatively impact your debt since payment history is another factor used to calculate your credit score.

While debt settlement may sound good in theory, you should use it as a last resort option before filing bankruptcy. This solution is risky since it doesn’t guarantee that you’ll settle your debt. Your creditor could reject the offer.

Debt Consolidation

If your credit isn’t damaged too much, you might be able to qualify for a debt consolidation loan. While this isn’t technically a debt relief option, it can help you to consolidate your debt and potentially lower your interest rate, allowing you to save money.

To consolidate your debt, you’ll apply for another loan, ideally one with better terms than your existing debt. You’d use the loan to pay off your outstanding credit card debts. Then, you will make installment payments to the lender instead of paying the creditors.

Before you apply for a debt consolidation loan, compare your options to identify the loans with the most competitive terms and interest rates.

Declaring a Chapter 7 or Chapter 13 Bankruptcy

Depending on your situation, declaring Chapter 7 or Chapter 13 bankruptcy may make the most sense. For instance, if you can’t make the payments with a debt management or debt settlement plan, bankruptcy could be an option to avoid going deeper into debt. But before you declare bankruptcy, consider speaking with a bankruptcy attorney to weigh out the pros and cons of this solution.

Bankruptcy should be one of your last resorts since it can drastically harm your credit. Also, it will stay on your credit report for up to 10 years after the filing date. To settle your debts with bankruptcy, you may also be forced to sell some of your assets.

The Takeaway

Credit card debt forgiveness involves paying less than the full amount you owe. While this prospect may sound great in theory, in reality it can harm your credit and end up costing you financially. If you find yourself starting to struggle with debt repayment, contact your credit card company to see if they will offer a hardship plan. If they’re unwilling to help or your financial troubles require a more long-term solution, you can explore credit debt forgiveness and other alternatives.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Financial Tips & Strategies: The tips provided on this website are of a general nature and do not take into account your specific objectives, financial situation, and needs. You should always consider their appropriateness given your own circumstances.

Non affiliation: SoFi isn’t affiliated with any of the companies highlighted in this article.

Third-Party Brand Mentions: No brands, products, or companies mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third-party trademarks referenced herein are property of their respective owners.

Tax Information: This article provides general background information only and is not intended to serve as legal or tax advice or as a substitute for legal counsel. You should consult your own attorney and/or tax advisor if you have a question requiring legal or tax advice.

More from MediaFeed:

My bank made an error. Do I really have to tell them if it benefits me?

A bank error is an erroneous transaction affecting a customer’s deposit account. Here are some examples of a bank error:

- A bank erroneously deposits $50K into your checking account

- Your bank mishandles a deposit and miscalculates your account balance

- A bank charges your top savings account in error

- A bank deposits funds into the wrong account of a customer who has several types of bank accounts

Bank errors may occur from time to time, and they may not always be in your favor. You may submit a complaint to the Consumer Financial Protection Bureau (CFPB) whenever you’ve been wronged by a financial institution. You may file a CFPB complaint online.

izusek/istockphoto

A bank error happens whenever a financial institution causes a faulty transaction that affects a customer’s deposit account. Such mistakes can happen at any time and on any given day. Banks may acknowledge the possibility of such errors in their deposit account agreements.

Your deposit account agreement may provide guidance on how you can contact the bank if you discover an error on your statement. Banks are generally permitted to make adjustments to correct any errors. For example, a bank that mistakenly gives you $50K may reverse the transaction and may give you notice of the clawback action.

Pheelings Media/istockphoto

There may not be a specific bank error in your favor law, but you generally must return the funds if a bank accidentally gives you money. That’s because you have no right to spend, use, or withdraw any money you may receive from your bank in error. As mentioned above, banks are generally permitted to make adjustments to correct any errors.

What happens if a bank accidentally gives you money is it may discover the mistake and attempt a reversal of the transaction. This can result in an overdraft or negative balance if you withdraw or spend the accidental funds before the bank discovers the error. The bank may attempt to recover the money through other means, such as contacting law enforcement and filing a police report.

You don’t have a right to spend money that doesn’t belong to you. If the bank gives you money by accident, the bank under existing laws may pursue and demand full reimbursement of the accidental transaction as a matter of unjust enrichment (Learn more atPersonal Loan Calculator).

Koh Sze Kiat/istockphoto

If you receive a bank error in your favor:

Do Not Spend the Money

Spending money that doesn’t belong to you is never a good idea. You’re not responsible for a bank’s mistakes, but you could be held responsible if you receive bank funds in error and fail to return the liquid assets. Such a bank error is not your typical direct deposit transaction.Banks are typically required to report deposits over $10,000 to the IRS, but this may not apply if a bank gives you more than $10K by accident.

Contacting Your Bank

In addition to not spending the money, you may want to contact your bank if you discover a bank error in your favor. You can call your bank’s customer service phone number to report the mistake.

You may find your bank account number in your personal checkbook or mobile banking app if the bank asks you to provide your account number for verification purposes.

Monitoring Your Bank Account

Whether you have a traditional bank account or an online savings account, monitoring your bank account is always a good idea. If a bank accidentally gives you money, you can monitor your account to see if and when the bank reverses the erroneous transaction.

You can transfer money from bank to bank at any time, but you may want to minimize your bank account activity until resolving any bank errors affecting your account.

damircudic/istockphoto

A bank error that gives you money by mistake is not really in your favor. That’s because you don’t have a right to keep that money, so allowing your bank to recover the funds may be your best course of action.

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at here. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at here.

FreshSplash/istockphoto

bernie_photo/istockphoto

Featured Image Credit: stefanamer/istockphoto.

AlertMe