Lenders will consider a number of factors — not just your credit score — when determining if you’ll be approved for a mortgage. Your debt-to-income ratio and proof of income represent a couple of things you need to buy a house.

Figuring out how to buy a house with a so-called bad credit score can vary on a case-by-case basis. These eight tips will help you assess your financial situation and plan accordingly to buy a house with bad credit.

Image Credit: Depositphotos.

1. Get Your Credit Reports

As the saying goes, knowledge is power. Assessing your credit is a valuable first step to understand where you stand in qualifying for a mortgage.

A credit report can provide a detailed overview of your creditworthiness, including your total debt, payment history, and age of your credit accounts. You can request free credit reports from this site or once a year directly from each of the three major credit reporting companies: Equifax, Experian, and TransUnion.

Upon receipt of your credit reports, it’s important to review any derogatory marks (e.g., late payments) and check for errors. Addressing mistakes could give a quick boost to your credit score.

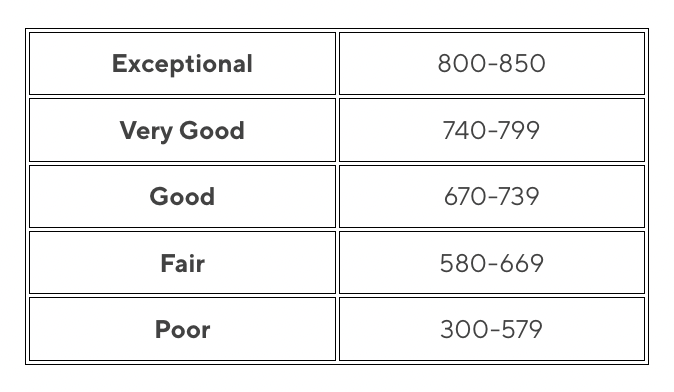

Many lenders use the FICO® score model to calculate credit scores, from 300 to 850, and categorize them like this.

It’s not uncommon for your FICO score to differ slightly among the three credit reporting companies, so mortgage lenders take the average or use the middle score.

According to the June 2021 Origination Insight Report by Ellie Mae, the average FICO score ranged from 743 to 753 for mortgages that closed in the first half of 2021. Borrowers with credit scores in this range or higher generally receive the most competitive mortgage rates.

Meanwhile, borrowers with credit scores below 650 represented only 6.2% of mortgages in June 2021.

An estimated 30% of U.S. consumers had credit scores in the subprime range, or less than 670, in Q1 of 2021, Experian found. (There is no universal definition of “subprime.” And Experian sometimes uses the term “nonprime,” for the category of borrowers with scores between 601 and 660.)

Image Credit: alexsl/istockphoto.

2. Plan to Pay a Higher Mortgage Interest Rate

Lenders may consider borrowers with poor credit more likely to default on a mortgage loan. To account for this risk, borrowers with lower credit scores usually face higher interest rates.

A modest increase in the mortgage interest rate can bump up your monthly payment and translate to much more interest paid over the life of the loan. For example, a borrower with a 30-year fixed-rate loan of $250,000 at 5% interest would pay $53,468 more in interest than a borrower with a 4% interest rate.

Paying a higher interest rate may be an unavoidable part of buying a house with bad credit. An option is to refinance your mortgage later to secure a lower rate and save on interest, especially if you make timely payments and improve your credit over time.

Image Credit: AlbertPego/istockphoto.

3. Pay Your Other Debts

How much debt you have and your ability to pay it is another factor lenders weigh when approving mortgage loans. This is captured through your debt-to-income ratio. Your DTI ratio is your monthly debt obligations divided by your gross monthly income and multiplied by 100.

Higher DTI ratios suggest that borrowers have less ability to make monthly payments. A 43% DTI ratio is usually the highest a borrower can have to obtain a qualified mortgage.

Paying off other debts, like credit cards and student loans, can improve your DTI ratio and signal to lenders that you can afford mortgage payments. Reducing your debt can boost your credit score too by lowering your credit utilization ratio, which is a measure of the amount of available revolving credit you use.

Image Credit: bernie_photo/istockphoto.

4. Draw Up a Budget

Buying a home is exciting, and it’s easy to lose sight of the true cost of homeownership when shopping for your dream home. But this puts you at risk of becoming “house poor,” meaning you have to spend a disproportionately high share of your monthly income on housing.

Although buying a home is a way to build wealth, having little left over from your paycheck makes it hard to save for retirement and realize other financial goals.

The dreaded B-word, budgeting, is a useful way to ensure that you can afford a home before you walk away with the keys.

An effective budget accounts for both the upfront costs of buying a home (down payment and closing costs) and the long-term expenditures. Besides the loan principal and interest, it’s important to consider property taxes, homeowners insurance, and maintenance, as well as private mortgage insurance (PMI) if you plan to put less than 20% down on a conventional loan, or mortgage insurance premiums (MIP) for an FHA loan, no matter the down payment. They add up, but PMI and MIP allow many people to buy homes who otherwise wouldn’t be able to.

Image Credit: megaflopp/istockphoto.

5. Save Up a Down Payment

If you’re a buyer with subpar credit, putting more money down on a home can be advantageous. A larger down payment means borrowing less money, making the loan less risky to lenders and improving the chances of qualifying with bad credit. A smaller loan amount also accrues less interest.

But of course, saving up for a down payment can be challenging. If you meet first-time homebuyer qualifications, you may be eligible to receive down payment assistance.

Image Credit: Ridofranz/istockphoto.

6. Opt for an FHA Loan

Buyers with lower credit scores or less money tucked away for a down payment could benefit from an FHA loan. FHA loans are issued by private lenders but are insured and regulated by the Federal Housing Administration.

Borrowers with credit scores of at least 580 may put just 3.5% down. If your credit score is 500 to 579, you might still qualify, but need to make a 10% down payment. Borrowers who have declared bankruptcy in the past may still qualify for an FHA loan.

Keep in mind that borrowers with higher credit scores who qualify for a conventional (nongovernment) mortgage may put just 3% down.

Image Credit: designer491/istockphoto.

7. See if You Are Eligible for a VA or USDA Loan

The federal government backs other loan types that can help buyers with fair credit.

Active-duty service members, veterans, or certain surviving spouses may use a VA loan to purchase a primary residence. VA loans usually don’t require a down payment, and the U.S. Department of Veterans Affairs does not set a minimum credit score for eligibility. Lenders have their own requirements, though, so it’s important to compare options.

The U.S. Department of Agriculture guarantees mortgages issued to low- and moderate-income homebuyers in eligible rural areas. No down payment is needed, and the USDA does not specify a credit score requirement. But lenders will still evaluate a borrower’s credit history and ability to pay back the loan.

VA loans typically come with a one-time funding fee that varies; USDA loans, an upfront and annual guarantee fee.

Image Credit: designer491/istockphoto.

8. Build Up Your Credit Scores

Raising your credit scores can increase your chances of qualifying and securing better loan terms, but it takes time. Negative marks usually stay on your credit reports for seven years.

Paying bills on time, every time, can gradually build up your credit scores. And if possible, it’s a good idea to stay below your credit limits and avoid applying for several credit cards within a short amount of time.

Soft credit inquiries do not affect credit scores, no matter how often they take place. Multiple hard inquiries if you’re rate shopping for an auto loan, mortgage, or private student loan within a short period of time are typically treated as a single inquiry.

But outside of rate shopping, many hard pulls for new credit can lower your credit scores and indicate distress in a lender’s eyes.

Image Credit: NicoElNino/istockphoto.

The Takeaway

Can you buy a house with bad credit? Yes, but you may have to put more money down or accept a higher interest rate to qualify. If taking steps to improve your credit aren’t enough, you might consider using a cosigner or exploring federal loan programs. Knowing how to buy a house with bad credit is a good first step to making it happen.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

Image Credit: marchmeena29/istockphoto.

More from MediaFeed

I’m in a tight bidding war for my dream house. How can I make sure I win?

Image Credit: dragana991/istockphoto.

AlertMe