Tick, Tick, Boom

These are historic times. We got another piece of data yesterday, but the puzzle is still not solved.

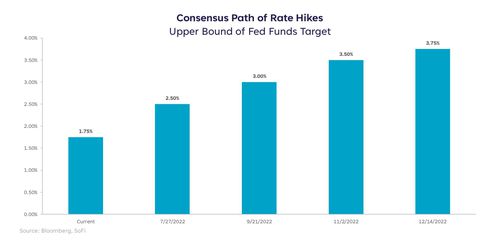

The Federal Reserve raised its benchmark policy rate by 75 basis points to an upper bound of 1.75%. We haven’t seen a hike of this size since 1994. Just one week ago, markets were still expecting only a 50-basis point move, but that was quickly abandoned for more aggressive action after a hotter-than-expected inflation print last Friday.

Additionally, Fed officials raised their forecast for the Fed Funds Rate at the end of 2022 from 1.9% to 3.4% and for 2023 from 2.8% to 3.8%. Adjustments that large in just three months’ time reinforce the growing sentiment that the Fed was far behind the curve. We’ve now seen three hikes in this cycle, each one bigger than the last…tick, tick, boom.

Related: How rising inflation affects insurance rates

Dynamite or Kryptonite?

Sometimes you have to break it down in order to build it back up. That’s a phrase used often by business leaders who are trying to “fix” a problem in their company. In a perfect world, we can light the dynamite carefully enough to blow up the problem spots without taking the whole thing down.

If we ask the market, it’s still sending a message that averting a deep recession is possible (judging by the S&P’s max drawdown of 22% so far this cycle). Earlier this week, however, the S&P officially entered bear market territory for the first time since 2020 and the 2s/10s yield curve inverted more than once. Those indicators would say the market is still hanging on to some “no recession” optimism, but the likelihood of averting one has fallen. Typically, drawdowns coupled with recessions are deeper than 30%, which would suggest the market has not yet priced in a recessionary environment.

And here’s where rate hike expectations fall for the remainder of the year. Expectations are for another 75 bps hike in July, and roughly 125 bps more before the end of the year. That would bring the Fed Funds Rate to an upper bound around 3.75%.

The market has predicted hikes with surprising accuracy so far, and the acceleration of hikes has given the market comfort for now. That said, inflation is kryptonite for markets and rate hikes are the best tool we have to work with. There really is no choice but to be aggressive about attacking the problem…regardless of recession risk.

Trimming the Wick

The Fed’s previous projections for growth, unemployment, the Fed Funds Rate, and inflation were pretty far off base, in my opinion. This meeting brought those projections to a more appropriate place – 2022 growth expectations came down from 2.8% to 1.7% and inflation expectations moved up from 4.3% to 5.2%.

Despite volatility immediately after the Fed announcement, markets reacted positively. I think the two biggest positives from the meeting were, 1) the Fed showed they were willing to be nimble and react quickly to the data, 2) they also proved that they were watching more “real world” indicators to make policy decisions. In particular, headline inflation instead of core, and consumer sentiment and consumer activity.

The best we can do as investors is wait for some of the immediate uncertainty to abate and stay ready to re-evaluate our allocations in the case of any unexpectedly good or bad news. I continue to believe volatility stays elevated through June and likely July. It’s more important as investors to prevent full participation in drawdowns than to ensure full participation in upside. As such, I’m comfortable keeping a larger-than-normal cash position until later in summer.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

More from MediaFeed:

US recession history: Reviewing past market contractions

From time to time, media outlets that cover financial news will report rumblings of a coming recession. And that can be a little nerve-jangling.

The potential problems are not unknown, because the country has been there before —most notably for the Great Recession from 2008 to 2009, the worst financial crisis in the U.S. since the Great Depression.

A recession can make jobs disappear or cause employers to cut hours, wages, or bonuses. That can affect consumer confidence and spending. A recession also can lead to, or be preceded by, a significant stock market downturn and less spending by businesses as they change their focus from growing to merely surviving.

So, yes, it can be scary, but it’s also a natural part of a business or economic cycle. After expansion, there is, inevitably, a contraction. A boom and then a bust.

Lazy_Bear / istockphoto

It’s a little like predicting the weather: There may be signs of a storm on the horizon, but it’s tough to tell exactly when, or if, it will actually hit. Or how bad it could be.

Some folks point to an inverted yield curve as a sort of economic barometer. An inverted yield curve has preceded all nine of the U.S. recessions that have occurred since 1955, so it’s a worthy warning sign.

But it’s only one indicator, and unlike your weather app, it doesn’t provide a tight timeline to help you avoid the storm. It just means there could be trouble in the next year, or two, or three.

A recession is loosely defined as two straight quarters of declines in real gross domestic product (GDP), the broadest gauge of U.S. growth.

But the official designation comes from the National Bureau of Economic Research (NBER), a private, nonprofit organization of economists who determine when a recession starts and ends.

That group looks for a “significant decline in economic activity” lasting “more than a few months” based on a number of indicators including real GDP, real income, employment, industrial production and wholesale-retail sales.

How long do recessions last? Recovery may seem to take forever, but since the end of World War II, US recessions have averaged about 11 months, according to NBER data. The Great Recession of 2008 was an outlier at 18 months, and the Great Depression was 45 months long.

wpd911

The thought of going through another recession — whenever it might come — can be daunting.

Constant reports about market fluctuations and what they might mean can make investing difficult. But there are a few things savers can consider doing to better protect their hard-earned money:

• They can try to have an emergency fund of three to six months’ worth of living expenses saved in an easy-to-access account, so they won’t be tempted to dip into their investment savings if they lose their job or experience a pay cut.

• They can look at rebalancing regularly to be sure their portfolio mix matches their financial planning goals and their risk tolerance.

• They can seek out professional help from a fiduciary adviser who has their best interests in mind (and doesn’t make commissions based on recommendations). Investors who have questions about what’s happening in the market and how it affects their portfolio can talk to a financial planning professional.

Here is our list of recessions throughout U.S. history.

designer491 / istockphoto

Uncannily familiar with the Great Recession of 2008 to 2009, the recession of 1797 is believed to have been caused by a credit expansion and an investment bubble that included real estate, manufacturing and infrastructure projects.

Problems ensued, bringing about a recession that affected nearly everyone from investors to shopkeepers to laborers.

Robert Linsdell from St. Andrews, Canada / WikiMedia Commons

The Panic of 1857 wasn’t the first financial crisis in the United States, but thanks to the invention of the telegraph, news about the crisis spread quickly across the country.

Most historians attribute the panic to a confidence crisis that involved the failure of the Ohio Life Insurance and Trust Company, but other events have also been cited, including the end of the Crimean War (which affected grain prices), excessive speculation in various markets and questions about the overall stability of the U.S. economy.

Beyond My Ken / WikiMedia Commons

Often referred to as the “Long Depression,” the Depression of 1873–1879 started with a stock market crash in Europe. Investors there began selling their investments in American projects, including bonds that funded railroads.

Without that funding, the banking firm Jay Cooke and Company, which was heavily invested in railroad construction, realized it was overextended and closed its doors.

Other banks and businesses followed; and from 1873 to 1879, 18,000 U.S. businesses went bankrupt, including 89 railroads and at least 100 banks.

At the same time, the Coinage Act of 1873 demonetized silver as the legal tender of the United States, in favor of fully adopting the gold standard. The withdrawal of silver coins further contributed to the recession, as miners, farmers and others in the working class had no way to pay their debts.

Frank Leslie’s Illustrated Newspaper / WikiMedia Commons

Like many other financial downturns, this depression was preceded by a series of events that undermined public confidence and weakened the economy, including disputes over monetary policy (particularly gold vs. silver), underconsumption that led to a cutback in production and government overspending.

Two of the country’s largest employers, the Philadelphia and Reading Railroad and the National Cordage Company, collapsed, and the stock market panic that followed turned into a larger financial crisis.

Banks and other financial firms began calling in loans, causing hundreds of businesses to go bankrupt. More than 16,000 businesses failed, and unemployment rates and homelessness soared.

Frank Leslie’s Illustrated Newspaper / WikiMedia Commons

This recession (May 1907 to June 1908) was preceded by the San Francisco Earthquake, which took a toll on the insurance industry. The recession was also influenced by the Bankers Panic of 1907 along with a dramatic 50% drop in the stock market.

Those events spread fear and a lack of confidence across the country in the financial industry, causing more banking failures. As a result, the banking industry experienced major changes, including the creation of the Federal Reserve System in 1913, which was designed to provide a more stable monetary and financial system.

New York Public Library / WikiMedia Commons

Most recessions last for months. The Great Depression lasted years and is generally regarded as the most devastating economic crisis in U.S. history. It had many causes. Reckless speculation and overvaluation ended in a stock market crash in 1929.

Consumer confidence crashed as well, and a downturn in spending and investment led businesses to slow down production and lay off workers.

And by early 1933, after a series of panics caused investors to demand the return of their funds, thousands of banks had closed their doors. Immediately upon taking office, President Franklin Roosevelt began implementing a recovery plan, including reforms known as the New Deal.

He also moved to protect depositors’ accounts with the new Federal Deposit Insurance Corporation (FDIC). And he created the Securities and Exchange Commission (SEC) to regulate the stock market. America’s entry into World War II further solidified the recovery, as production expanded and unemployment continued to drop from a high of 24.9% in 1933 to 4.7% by 1942.

searagen / istockphoto

The result of demobilization and a shift to a peacetime economy after World War II ended, this eight-month recession (February to October 1945) is mostly known for a precipitous 12.7% drop in the GDP. The unemployment rate stood at 5.2%.

US government photographer / WikiMedia Commons

Economists blame this 11-month downturn (November 1948 to October 1949) on the “Fair Deal” social reforms of President Harry Truman, as well as a period of monetary tightening by the Federal Reserve in response to rampant inflation.

Although it is generally considered a minor downturn, the unemployment rate did reach a 7.9% peak in October 1949.

Harry S. Truman Library & Museum / WikiMedia Commons

A combination of events led to this 10-month recession (July 1953 to May 1954), including a post-Korean War contraction as well as the tightening of monetary policy due to inflation and the separation of the Federal Reserve from the U.S. Treasury in 1951.

Unemployment peaked at 6.1% in September 1954, four months after the recession was officially over.

Divided Families Foundation

The U.S. Federal Reserve’s contractionary monetary policy — restricting the supply of money in an overheated economy — is often cited as the cause of this economic downturn.

The GDP fell 4.1% in the last quarter of 1957, then dropped another 10% at the start of 1958. Unemployment peaked at 7.5% in July 1958.

AgnosticPreachersKid / WikiMedia Commons

This recession lasted 10 months (from April 1960 to February 1961) and spanned two presidencies. When it began, Dwight D. Eisenhower was in office, but John F. Kennedy inherited the problem (after using the downturn to defeat Vice President Richard Nixon in the 1960 presidential election).

Although the recession caused serious problems for many sectors of the economy (a drop in manufacturer’s sales — and, therefore, manufacturing employment — was one of the first signs of trouble), its overall effects were mostly mild.

Personal income continued to rise through much of 1960, and declined less than 1% from October 1960 to February 1961. Unemployment was high, however, peaking at 7.1% in May 1961.

The Ledger-Enquirer / WikiMedia Commons

Though it lasted almost a year (from December 1969 to November 1970), this recession is considered to have been relatively mild, because it brought about only a 0.6% decline in the GDP. However, the unemployment rate was high, reaching a peak of 6.1% in December 1970.

The downturn’s causes include a rising inflation rate resulting from increased deficits, heavy spending on the Vietnam War and the Federal Reserve’s policy of increasing interest rates.

S.Sgt. Albert R. Simpson. Department of Defense. Department of the Army. Office of the Deputy Chief of Staff for Operations. U.S. Army Audiovisual Center / WikiMedia Commons

This recession, which lasted from November 1973 to March 1975, is usually blamed on rocketing gas prices caused by OPEC (the Organization of Petroleum Exporting Countries), which raised oil prices and embargoed oil exports to the United States.

Other major factors in this 1970s recession included a stock market crash that caused a bear market from 1973 to 1974, and several monetary moves made by President Richard Nixon , including implementing wage-price controls and ending the gold standard in the U.S. The result was “stagflation,” a slowing economy with high unemployment and high inflation.

David Falconer / WikiMedia Commons

There were actually two recessions during this period, according to the NBER. A brief recession occurred during the first six months of 1980, and then, after a short period of growth, a second, more sustained recession lasted from July 1981 to November 1982.

That second recession is largely blamed on monetary policy, as high-interest rates — in place to fight inflation — put pressure on sectors of the economy that depended on borrowing, such as manufacturing and construction.

Unemployment grew from 7.4% at the start of the recession to a peak of 10.8% in December 1982, the highest level of any modern recession.

White House photo, courtesy Reagan Library, in PD as official government record / WikiMedia Commons

The “Reagan Boom” of the early- and mid-1980s came to an ugly end at the end of the decade, as stock markets around the world crashed and the U.S. savings and loan industry collapsed. When Iraq invaded Kuwait in 1990, driving up the price of oil, consumer confidence took another hit.

The recession lasted from July 1990 to March 1991, according to the NBER, but it took the economy a while longer to fully rebound. Unemployment peaked at 7.8% in June 1992, and candidate Bill Clinton’s focus on the struggling economy helped him unseat President George H.W. Bush later that year.

Christopher Michel from San Francisco, USA / WikiMedia Commons

The 2001 recession lasted just eight months, from March to November, according to the NBER. And yet, the story behind the dot-com bubble trouble that triggered it remains a cautionary tale.

As investors looking for the next big thing overlooked fundamentals that are important to a business’ stability, a frenzy grew over tech companies in the late 1990s. Many became overvalued and the Y2K scare at the start of 2000 took things up another notch.

When the tech bubble bursted in 2001, equities crashed, and the 9/11 terrorist attacks only made matters worse. The Nasdaq index tumbled from a peak of 5,048.62 on March 10, 2000, to 1,139.90 on Oct 4, 2002, a 76.81% fall.

On June 7, 2001, President George W. Bush signed the Economic Growth and Tax Relief Reconciliation Act of 2001 (EGTRRA), which used tax rebates and tax cuts to help stimulate the economy. And by 2003, the Federal Reserve had lowered its federal funds rate to a range of between 0.75% and 1.0% to further tamp down the recession.

DepositPhotos.com

The Great Recession is as notable for its severity as for its length. According to Federal Reserve history, the nation’s GDP fell 4.3% from its highest level at the end of 2007 to its lowest point in mid-2009. Meanwhile, the unemployment rate kept rising, from 5% at the end of 2007 to 10% in October 2009.

Home prices fell about 30%, on average, from their mid-2006 peak to their low in mid-2009. The S&P 500 fell 57% from October 2007 to March 2009. And the net worth of U.S. households and nonprofit organizations also took a hit, dropping from approximately $69 trillion in 2007 to $55 trillion in 2009.

Though the recession was especially devastating in the U.S., where it was triggered by the subprime mortgage crisis, this wasn’t the only country affected. A global economic downturn resulted in an unprecedented number of stimulus packages being introduced around the world.

In the U.S., the Federal Reserve reduced the federal funds rate from 5.25% in September 2007 to a range of zero to 0.25% by December 2008. It also introduced a $787-billion stimulus package, the American Recovery and Reinvestment Act of 2009, including tax breaks and spending projects credited with helping revive the sagging economy.

Learn more:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

External Websites: The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. Links are provided for informational purposes and should not be viewed as an endorsement.

Third Party Brand Mentions: No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this article. Third party trademarks referenced herein are property of their respective owners.

SoFi Invest

The information provided is not meant to provide investment or financial advice. Investment decisions should be based on an individual’s specific financial needs, goals and risk profile. SoFi can’t guarantee future financial performance. Advisory services offered through SoFi Wealth, LLC. SoFi Securities, LLC, member FINRA/SIPC. The umbrella term “SoFi Invest” refers to the three investment and trading platforms operated by Social Finance, Inc. and its affiliates (described below). Individual customer accounts may be subject to the terms applicable to one or more of the platforms below.

Getty

Featured Image Credit: Photodjo / iStock.

AlertMe