In 2021, the Average Down Payment On a House was $70,600 or 13% down

The average down payment nationwide was $70,600 in 2021, according to Optimal Blue, a division of Black Knight. The median for all buyers was 87% of the home price financed, or 13% down.

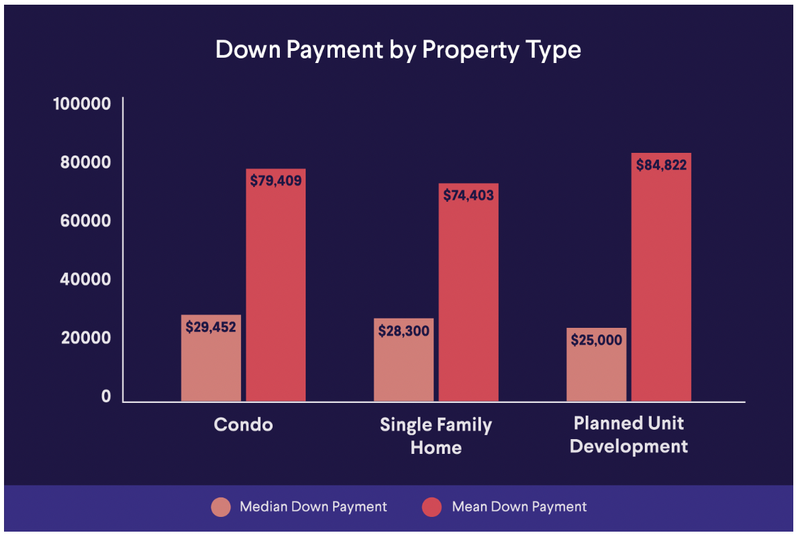

Because extremes can skew an average, the median is more informative. Of course, timing and location influence any mention of an average down payment, but here is the median and average by property type at that time:

Image Credit: kwanchaichaiudom / iStock.

Average Down Payment by Age

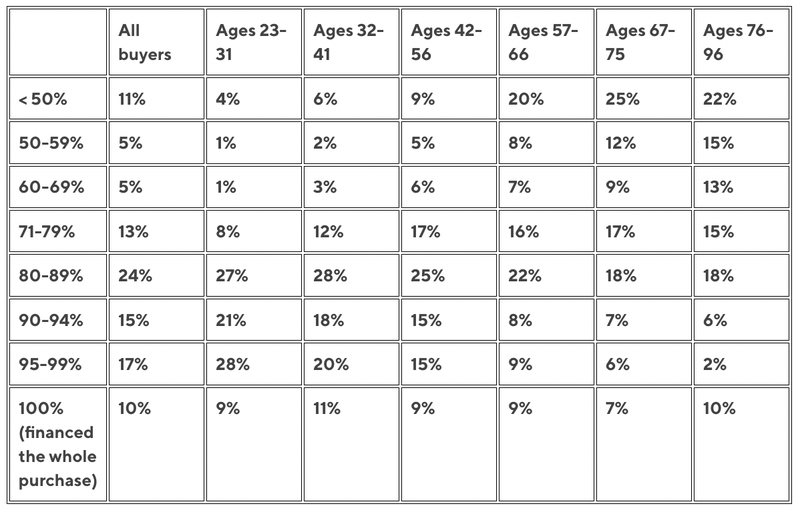

The latest NAR Home Buyers and Sellers Generational Trends Report breaks down by age the percentage of a home that was financed by homebuyers in the 12-month period ending in July 2021.

Older buyers tend to use proceeds from the sale of a previous residence to help fund the new home. Buyers 57 to 66 years old, for instance, put a median of 21% down, the NAR report shows.

Most younger buyers depend on savings for their down payment. Buyers ages 23 to 31 put down a median of 8%, and those ages 32 to 41, 10%.

A fortunate 29% of younger millennial homebuyers received down payment help from a friend or relative.

Percentage of Home Financed

Image Credit: urbazon/istockphoto.

Average Down Payment by State

Down payments are tied to home prices in any state.

You can look into the cost of living by state for an overview and then find the median home value in a particular state at a given point in time and estimate your down payment.

Redfin, for example, shows a median sales price of $763,300 in California in late 2022. A 3% down payment would be $22,900; 10% down, $76,330; and 20% down, $152,660.

California is joined by Hawaii, Oregon, Washington, and Colorado on many lists of the most expensive states in which to buy a house.

Redfin put the median sales price of a home in the Aloha State at nearly $700,000 in late 2022. Three percent down would be $21,000; 10% down, $70,000; and 20%, $140,000.

Mortgages under conforming loan limits are often the most attractive for homeowners because they are backed by Fannie Mae and Freddie Mac. The limit is $647,200 for a one-unit property in most counties and $970,800 in high-cost counties (which includes all Alaska counties).

A jumbo loan may be used to finance a property exceeding those limits.

The least expensive states in which to buy a home? West Virginia, Arkansas, Iowa, Indiana, Ohio, Nebraska, Kansas, and Oklahoma are among them.

You might want to check out housing market trends by city.

Image Credit: ake1150sb/istockphoto.

Down Payment Requirements by Mortgage Loan Types

A first-time homebuyer can often put as little as 3% down on a home purchase.

That is the minimum down required for a conventional home loan, a nongovernment loan and the kind favored by most buyers.

FHA Loans:

An FHA loan, acquired through private lenders but guaranteed by the Federal Housing Administration, allows for a 3.5% down payment if the borrower’s credit score is at least 580. Someone with a credit score of 500 to 579 is required to put 10% down.

VA or USDA Loans:

A VA loan or USDA loan usually requires no down payment.

A VA loan backed by the Department of Veterans Affairs is for eligible veterans, service members, Reservists, National Guard members, and some surviving spouses. The VA also issues direct loans to Native American veterans or non-Native American veterans married to Native Americans.

A USDA loan backed by the U.S. Department of Agriculture is for households with low to moderate incomes buying homes in eligible rural areas. The USDA also offers direct subsidized loans for households with low and very low incomes.

For all of the above loan types, the home being purchased must be a primary residence, but a homebuyer can use a conventional or VA loan to purchase a multifamily property with up to four units if one unit will be owner-occupied.

Image Credit: inewsistock/istockphoto.

Should You Aim for 20% Down?

Should buyers try to put 20% down to get a mortgage loan? Here are some things to consider:

If Your Down Payment Is at Least 20%

Putting down at least 20% has benefits:

You won’t have to pay for mortgage insurance: If you put down 20% or more with a conventional loan, you won’t be required to pay for private mortgage insurance (PMI), which protects the lender if you were to stop making payments.

Your loan terms may be better: Lenders look at an applicant’s credit history, employment stability, income, debt to income ratio, and savings.

They’ll calculate the loan-to-value ratio, or what percentage of the home’s purchase price will be covered by the mortgage. Lenders often provide a better rate to borrowers who have an LTV ratio of 80% or lower — in other words, at least a 20% down payment — because they consider them a better risk.

You have instant equity in the property: You borrowed less than you could have, which translates to a lower mortgage payment, less interest paid over the life of the loan, and the potential later to take out a home equity loan.

If Your Down Payment Is Less Than 20%

If you have a down payment that’s less than 20%, you have plenty of company. Things to chew on:

A government loan could be the answer: FHA loans are popular with some first-time buyers because of the lenient credit requirements. Just know that up-front and monthly mortgage insurance premiums (MIP) always accompany FHA loans, and for the life of the loan if the down payment is under 10%. If you put 10% or more down, you’ll pay MIP for 11 years.

You may be able to improve your loan terms: If you can’t pull together 20% for a down payment, you can still help yourself by showing lenders that you’re a good risk. You’ll likely need a FICO® score of at least 620 for a conventional loan. If you have that and other positive factors, you may qualify for a manageable interest rate or better terms.

You can eventually cancel PMI: Lenders are required to automatically cancel PMI when the loan balance gets to 78% LTV of the original value of the home. You also can ask your lender to cancel PMI on the date when the principal balance of your mortgage falls to 80% of the original home value.

You may be able to find down payment assistance: City, county, and state down payment assistance programs are out there. They may take the form of grants or second mortgages, some with deferred payments or a forgivable balance.

Image Credit: courtneyk/istockphoto.

The Takeaway

What is the average down payment on a house? The median is less than 20%, which usually means mortgage insurance and higher payments. But buyers who put less than 20% down on a house unlock the door to homeownership every day.

Learn More:

This article originally appeared on SoFi.com and was syndicated by MediaFeed.org.

Please understand that this information provided is general in nature and shouldn’t be construed as a recommendation or solicitation of any products offered by SoFi’s affiliates and subsidiaries. In addition, this information is by no means meant to provide investment or financial advice, nor is it intended to serve as the basis for any investment decision or recommendation to buy or sell any asset. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi. These links are provided for informational purposes and should not be viewed as an endorsement. No brands or products mentioned are affiliated with SoFi, nor do they endorse or sponsor this content.

Communication of SoFi Wealth LLC an SEC Registered Investment Advisor

SoFi isn’t recommending and is not affiliated with the brands or companies displayed. Brands displayed neither endorse or sponsor this article. Third party trademarks and service marks referenced are property of their respective owners.

Communication of SoFi Wealth LLC an SEC Registered Investment Adviser. Information about SoFi Wealth’s advisory operations, services, and fees is set forth in SoFi Wealth’s current Form ADV Part 2 (Brochure), a copy of which is available upon request and at www.adviserinfo.sec.gov. Liz Young is a Registered Representative of SoFi Securities and Investment Advisor Representative of SoFi Wealth. Her ADV 2B is available at www.sofi.com/legal/adv.

Image Credit: Drazen_/istockphoto.

More from MediaFeed

The big mistakes people make when buying a starter home

Image Credit: svetikd/istockphoto.

AlertMe