The COVID-19 pandemic altered the landscape of the U.S. economy. Significant government relief and rock-bottom interest rates helped households build wealth, even as an inflation spike eroded their money’s real value. In the first quarter of 2020, U.S. households’ total wealth equaled $103.99 trillion, but that figure spiked to $141.10 trillion in the first quarter of 2022.

As a generation, millennials born between 1981 and 1996 (ages 26 to 41 in 2022) have benefited financially since the start of the pandemic, more than doubling their net worth. While they still lag behind older generations — particularly baby boomers and Gen Xers — millennials are starting to build long-term wealth, particularly through real estate ownership.

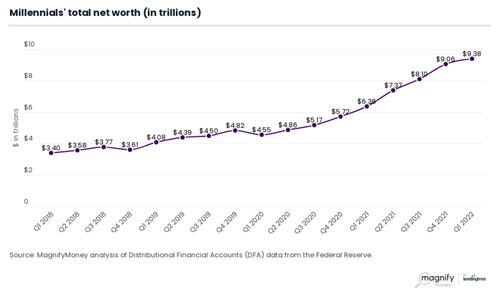

Millennial net worth has doubled since start of COVID-19 pandemic

In the first quarter of 2020, just as the coronavirus pandemic started to upend American life, millennials collectively held $4.55 trillion in net worth. Two years later, millennials have more than doubled their net worth to $9.38 trillion.

“The COVID-19 pandemic has changed the way people spend money, and savings rates have skyrocketed,” according to MagnifyMoney executive director Ismat Mangla. “Millennials are no exception. They’re also savvy when it comes to investing and compounding their earnings.”

Millennials are starting to build wealth as they become more established in the workplace, Mangla says.

Average millennial net worth has also doubled

Between increased earnings and support from pandemic-era government policies like expanded unemployment insurance and a pause on student loan payments, millennials have built a lot of wealth over the past two years.

Based on 2020 population figures from the U.S. Census Bureau, MagnifyMoney estimates millennials’ average net worth was $62,758 in the first quarter of that year. Using 2022 population estimates, that figure grew to $127,793 in the first quarter of 2022 — more than double the average from the first quarter of 2020.

That millennial net worth average is still much lower than the average net worth among older generations. Gen Xers (ages 42 to 57 in 2022) own $647,619 on average, and baby boomers (ages 58 to 76) own $1,021,264 on average. While millennials have doubled their net worth over the past two years, their wealth is still a fraction of what their older counterparts have.

Most of millennial wealth — and debt — is in real estate

Homeownership has been a successful strategy for building long-term wealth for generations, and millennials are no exception. Most of their wealth is held in real estate — homes and other properties — but they also hold wealth in consumer durables, which include cars, furniture and other household goods that have a longer lifespan.

Real estate can help explain why millennial net worth has risen during the pandemic.

“Millennials who were lucky enough to secure mortgages when interest rates were at historic lows have a significant leg up,” Mangla says. “As they pay down their mortgages, they build their net worth by accumulating equity in their homes.”

However, millennials who recently bought homes tend to have significant debt. Most of the debt owed by millennials (62.6%) is tied up in home mortgages, according to the Fed. Among other categories it tracks, consumer credit is also a big source of millennial debt (35.6%). Other liabilities totaled just 1.7%. Perhaps that debt burden is a big reason why 28% of millennials still receive financial support from their parents.

Even though Gen Xers have more debt across all categories than millennials, millennials hold the most consumer credit debt ($1.85 trillion) of any generation. No other generation has more than 22.0% of their overall debt in consumer credit. Some examples of consumer credit include car loans, credit cards and personal loans.

Older generations own most of the country’s wealth

Even though millennials have doubled their wealth during the pandemic, older generations still own most of America’s wealth. Baby boomers have more than half of the country’s wealth (50.4%), Gen Xers have 29.9% and the silent generation and those born earlier — which include those 77 and older in 2022 — have 13.1%. Millennials have just 6.6%.

To explain the massive wealth disparity between older and younger generations, Mangla calls it a “perfect storm for building incredible generational wealth.”

For baby boomers, they benefited from low housing costs, reductions in tax rates for high-income earners, a booming stock market, affordable education and low interest rates. Then they saw the values of their homes rise due to housing inflation.

Of course, baby boomers and other older generations also have had more time to build their wealth. While millennials have experienced economic headwinds, the bump in their collective net worth over the past two years is a positive sign.

Millennials hold just 6.6% of the country’s total net worth

Millennials have made up some ground recently, as their net worth grew the most relative to other generations from the first quarter of 2021 to the first quarter of 2022 (47.5%). But they still have a long way to go to catch up with older generations. Mangla says there’s no secret to wealth-building.

“The best ways to build wealth are to keep expenses low, find ways to increase your income — whether it’s through higher-paying jobs or side hustles — and invest that delta smartly for the long term.”

One smart investment may be real estate, though home prices have hit record highs and interest rates are rising quickly. Beyond that, millennials can contribute to tax-advantaged retirement savings accounts to help build wealth over the next few decades.

Methodology

MagnifyMoney researchers analyzed Distributional Financial Accounts (DFA) data from the Federal Reserve, focusing on millennials. The DFA measures wealth as assets minus liabilities. That’s the same calculation for net worth, so the terms are used interchangeably here.

Analysts then used the DFA and U.S. Census Bureau population data to estimate the average net worth of millennials.

We defined generations as the following:

- Millennials: Born between 1981 and 1996 (ages 26 to 41 in 2022)

- Generation Xers: Born between 1965 and 1980 (ages 42 to 56 in 2022)

- Baby boomers: Born between 1946 and 1965 (ages 57 to 76 in 2022)

Researchers also estimated average net worths among Gen Xers and baby boomers.

Related:

- Planning for retirement: How to get started

- Financial planner vs retirement planner: What’s the difference?

- How to find a financial planner

This article originally appeared on MagnifyMoney.com and was syndicated by MediaFeed.org.

More from MediaFeed:

25 things about adulting your parents really should’ve told you

Wouldn’t it be easier to have an instruction manual for adulthood? A book covering all the things parents should have taught their kids about personal finance, a career, happiness and the main things that matter in life?

Sadly, no manual or playbook exists to help you make all these new adult decisions. But if it did, it would include these 25 things your parents didn’t tell you about being an adult that you wished they did.

SPONSORED: Find a Qualified Financial Advisor

1. Finding a qualified financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to 3 fiduciary financial advisors in your area in 5 minutes.

2. Each advisor has been vetted by SmartAsset and is held to a fiduciary standard to act in your best interests. If you’re ready to be matched with local advisors that can help you achieve your financial goals, get started now.

Rattankun Thongbun / iStocl

When two-thirds of parents don’t discuss money with their kids, it’s not surprising that it becomes the main source of stress for 44 percent of people. From working and balancing money for your monthly expenses, to paying off college loans and saving money for your retirement, there are many personal finance matters to manage once you enter adulthood.

So while most people don’t keep track of all their finances (and a majority of Americans don’t know how much money they spent last month), you can start adulthood on the right foot with these 14 personal finance tips.

DepositPhotos.com

When you were still living with your parents, did you ever think about how they managed to pay for the house, car, groceries, clothes and everything else? You might have heard your parents discussing bills, but, of course, it is different when you’re the one behind the wheel. Now that you are an adult, you’re facing the reality that you have to pay many bills: credit cards, utilities, cable subscriptions, groceries and more.

That is why creating a budget is the first step in actively managing your finances. Tracking and monitoring your expenses allows you to see how you can afford both the essentials and things you value. For example, you can do things with no money on the weekends. Then you’ll have more money for a new car or vacation with friends.

DepositPhotos.com

If you don’t have a budget yet and don’t know how to get started, the 50/30/20 budget rule is a good starting point. This rule says that you should allocate your take-home pay using the following math: 50% for your needs, 30% for your wants and 20% for your savings.

These numbers may not be possible for new graduates, but it’s a great goal to work toward. What is important is that you regularly save money from what you earn, even if that means starting with $5 a paycheck and working your way up.

AndreyPopov/istockphoto

The very first thing you should do with your savings is build an emergency fund. Putting aside money for emergencies is critical because unforeseen expenses will happen. For example, a flat tire, a large medical bill or even losing your job are all things to plan for.

As a rule of thumb, an emergency fund should cover 3 to 6 months of living expenses so you’ll have a cushion until you find a new job. Of course, it will take time to reach this goal, but the important part is to get started.

DepositPhotos.com

After you’ve built up your emergency fund, it’s time to start saving for retirement. When you first become an adult, retirement seems like a lifetime away. But a fundamental yet overlooked idea is that the sooner you start building your retirement accounts, the better. Your older self will thank you for saving for retirement as soon as possible.

While you are young, you often have lighter financial responsibilities before the days of mortgages and kids. While it might seem lame to save money for retirement instead of spending it, remember the earlier and more you save, the earlier you can stop working.

DepositPhotos.com

Since many parents don’t talk about money matters with their kids, they don’t know that your money can work for you instead of you working for money once they become adults. If you knew from the start that investing could help you reach your financial goals, you might make different moves with your hard-earned money. Investments can provide an additional income stream that can help your overall financial plans and help build your wealth gradually.

nortonrsx

There are both good and bad debts, and understanding the difference will save you a lot of money and stress in the long run. Mortgages and student loans are often considered good debt. However, credit cards, personal loans and payday loans are bad debts. While it is almost impossible to live without credit cards, using them to fund a lifestyle you can’t afford is not a way to enter adulthood.

fizkes / istockphoto

If you’re having problems sticking to a budget and find yourself impulse shopping, paying with cash can help. It’s pretty quick and easy to use a credit card, so the act of counting out your hard-earned money can bring more mindfulness to your spending and help create better money habits.

DjelicS/ iStock

You should pay the total credit card balance every month to prevent costly interest charges on your purchases. Plus, it will improve your credit score. When you don’t pay your credit cards in full, the interest will start building up, and it gets harder to pay it back at all.

That can be a large hole to dig yourself out of. If you find yourself with credit card debt, it’s important to pay off the outstanding debt as soon as possible so the compounding interest charges are minimized.

kitzcorner // istockphoto

If you have a strong credit score but find yourself with a credit card balance, you may be able to transfer the balance to a 0% credit card. If you qualify, you’ll have 3-12 months to pay off your debt with no interest charges. If you ever find yourself in this situation, leveraging a 0% credit card offer can help you get out of debt faster.

SPONSORED: Find a Qualified Financial Advisor

1. Finding a qualified financial advisor doesn’t have to be hard. SmartAsset’s free tool matches you with up to 3 fiduciary financial advisors in your area in 5 minutes.

2. Each advisor has been vetted by SmartAsset and is held to a fiduciary standard to act in your best interests. If you’re ready to be matched with local advisors that can help you achieve your financial goals, get started now.

Farknot_Architect / istockphoto

If you don’t qualify for a 0% credit card transfer, you can negotiate for a lower interest rate. Did you know that you can call your creditors and just ask? If you have a good payment history and an acceptable credit score, creditors can lower your rate.

Depositphotos

Late payments can knock points off your credit score, a figure that shows your creditworthiness. Your credit score is between 300-850, and the higher the score, the better. It’s determined by factors like total debt, repayment history, number of open accounts and more.

Companies also use it to determine how likely you’re going to pay them back. This number will be referenced every time you want to rent an apartment, apply for a mortgage, purchase a car, open a bank account or apply for a credit card. So make on-time payments a priority.

Doucefleur / istockphoto

Your parents grew up and lived a part of their life in an era of traditional banking, so they may not have explained the benefits of online bill paying. It’s an easy way to pay your bills on time as it all happens without you once you’d set it up. However, be careful that you’re not spending more money than you have, as your bank will charge you costly overdraft fees if you dip below your balance.

gustavofrazao/ istockphoto

When you’re shopping online, credit cards offer better security features than debit cards. In addition, in a case of fraud, a credit card will provide better protection. If you shop online regularly with one site, like Amazon, think about opening a credit card that will give you points or a certain percentage of cashback when you shop.

DepositPhotos.com

If you don’t know the rules, how can you play the game? Suppose you’ve applied for a credit card for travel hacking to earn free flights or hotel stays. In that case, it is crucial to read the fine print to prevent fees and penalties and make sure you actually receive the large sign-up bonuses.

DepositPhotos.com

While money matters are an essential part of adulthood, there’s so much more to life and finding your place in the world.

Chainarong Prasertthai / istockphoto

While it’s often taboo to talk about money in America, if you’re struggling with money matters, don’t hide it. Whether you speak with your parents, friends or financial institutions, the sooner you work through the challenges, the faster you can make a plan to resolve them.

DepositPhotos.com

Your parents may provide suggestions for your college major and as well as your career. Odds are, they are coming from a place of love. But what they might not tell you is that it will take time to find a job that you enjoy. And that it might mean trying out different roles and using a process of elimination. You may not learn that you like ( or dislike) something until you give it a try. Then, over time, you’ll know which direction you want to go in to land a job you enjoy.

GaudiLab / istockphoto

During this process of elimination, you may discover that your childhood dreams have changed. Parents and teachers ask kids what they want to be when they grow up. Whether you want to be a doctor, a lawyer or a police officer, our childhood dreams provide some direction early in life. As you grow up, things may change. Try asking your parents what their childhood dreams were and how they shaped their careers.

DepositPhotos.com

The last thing most young adults who are striving for independence want to do is ask for help. Our brains are wired to push us toward doing things on our own. But life is complicated. If you’re having a bad day, a tough time navigating work or feeling down, it’s OK to ask your family, friends and professionals for help.

roman dragunov / istockphoto

If you grew up in a house where uncomfortable feelings weren’t welcomed, you might have formed a habit of hiding your feelings. Now that you’re an adult, you’ll need to work on your communication skills. The last thing you want to do at work is push feelings down so long that you blow up at a meeting and get fired.

g-stockstudio/istockphoto

While you’ve already navigated the complicated relationships that come with middle school, high school, and college, the dynamics of interpersonal relationships in the workplace take it to a whole other level.

You thought group projects in college were challenging? Unfortunately, the workplace is one long group project that never ends. If you find yourself struggling in this area, seek out a Career Coach who can help build your soft skills so that you’ll succeed no matter what role you’re in.

DepositPhotos.com

While protective parents may not preach about risks, it’s one of the best things you can do as a young adult. You’ll have less to lose. You learn something from it, gain experience and build confidence in your abilities and resilience.

William_Potter / istockphoto

You might have been raised to avoid mistakes at all costs. But if you play it so safe that you never push yourself, you’re missing out on growth, experience and learnings. No one’s perfect. If you have a good relationship with your parents, ask them what they learned from some of their biggest mistakes to give you to courage to push yourself into some new areas as an adult.

DepositPhotos.com

The odds are probably pretty high that you didn’t learn how to practice gratitude from your parents. However, at an age when you’re constantly comparing yourself to your friends and their accomplishments, gratitude is one key to happiness. According to Harvard Medical School, consistent gratitude can help you feel more positive emotions, enjoy your experiences, improve your health and build strong relationships.

DepositPhotos.com

Another route to happiness as an adult is letting go of the things you can’t control. If your parents didn’t model this behavior, it could be hard to make the switch as an adult. While you can do everything in your power to be a strong candidate for a job or an apartment, at the end of the day, the decision on who gets pick is out of your hands.

Prostock-Studio/istockphoto

At this age, what your friends think of you carries so much weight, but what others say is another thing you can’t control in life. To feel accepted and liked is something that everyone wants, but maturing into a new mindset is part of becoming an adult. You could apply author Brene Brown’s approach by training yourself to react by asking yourself, “How can I improve?” instead of, “What will they think?”

This article

originally appeared on Savoteur.comand was

syndicated by MediaFeed.org.

pixelfit

DepositPhotos.com

Featured Image Credit: Depositphotos.

AlertMe